Photo by Public Domain Pictures on Pexels.com

Everyone is told to save for retirement early. Everyone is told to save consistently. You may wonder: just what kind of difference might an early start and ongoing account contributions make?

Let’s take a look some eye-opening numbers

(You can verify these numbers simply by using the compound interest calculator at investor.gov, the Securities and Exchange Commission’s website).

Scenario #1

If you are 30 years old and contribute $200 a month to a tax-deferred retirement account (initial investment of $200, then $200 per month thereafter), you will have $333,903.82 by age 65, if that account consistently returns 7% a year. (This is with annual compounding.)

Scenario #2

If you change one variable in the above scenario – you start saving and investing at 25 years old instead of 30 – you will have $482,119.16 by age 65.

Scenario #3

Start at 20 years old and you will have $689,998.84 by age 65.

An early start really matters.

It gives you a few more years of compounding – and the larger the account balance, the greater difference compounding makes.

These are simple scenarios, but the impact of consistent saving and investing is undeniable. Over time, it may help you build a retirement account that could become a significant part of your retirement savings.

▲Benefit of saving and investing early

Investors should make saving for retirement a priority by investing early and often. This graph illustrates the savings and investing behavior of four people who start saving the same annual amount at different times in their lives, for different durations and with different investment choices. Consistent Chloe saves and invests consistently over time and reaches 65 with more than double the amount of the other investors. Quitter Quincy starts early but stops after 10 years, just as Late Lyla starts saving. Despite saving one-third as much as Lyla, the power of long-term compounding on money invested early helps Quincy end up with almost the same wealth at retirement. Nervous Noah saves as much and as often as Chloe, but chooses not to invest his money so he accumulates less than half of Chloe’s final amount.

Are you saving enough?

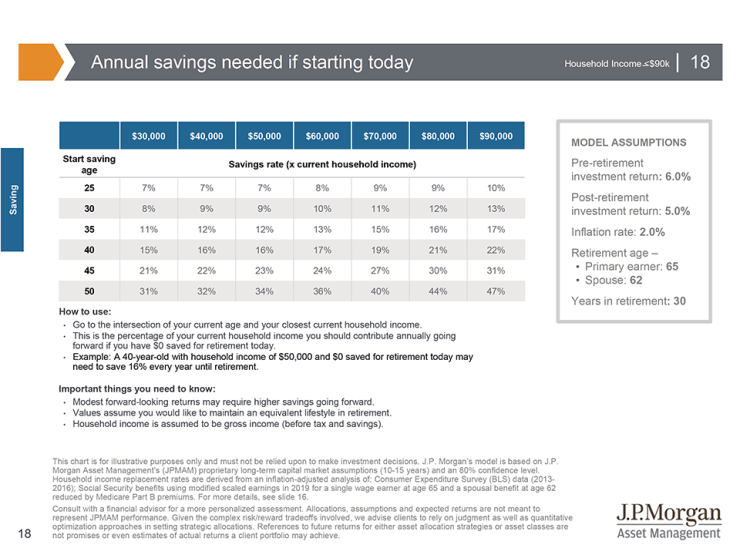

▲ Annual savings needed if starting today

What is the rule of thumb for the percentage of your income you need to save for retirement? Some say 10%, some say higher or lower. The real answer is that it depends—on what you earn, the “lifestyle you become accustomed to” and when you start saving. This chart shows the percentage of gross income someone would need to start saving at the ages in the left column to be able to afford the typical lifestyle associated with the household income amounts in the top row. Starting at age 25, the annual savings required ranges from 7% to 10%: achievable, but well above what most Americans save. By contrast, someone thinking about waiting until age 50 to focus on retirement should see how unrealistic that may be, with required savings of between 31% and 47% of their gross income. The sooner investors start, the better chance they may have of steadily winning the retirement savings race.

Sources

- https://www.investor.gov/additional-resources/free-financial-planning-tools/compound-interest-calculator

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

One Comment

Good post. Thanks for sharing.

Compound interest, in long run, does make a huge difference and can work wonders for us. Yet, very few of us realize this and end up taking debt … and make compound interest work against us!

LikeLike