Photo by rawpixel.com on Pexels.com

How global returns and proper diversification are affecting overall returns.

Your Portfolio vs. the S&P 500

“Why is my portfolio underperforming the market?” This question may be on your mind. It is a question that investors sometimes ask after stocks shatter records or return exceptionally well in a quarter.

The short answer is that while the U.S. equities market has realized significant gains in 2018, international markets and intermediate and long-term bonds have underperformed and exerted a drag on overall portfolio performance. A little elaboration will help explain things further.

A diversified portfolio necessarily includes a range of asset classes.

This will always be the case, and while investors may wish for an all-equities portfolio when stocks are surging, a 100% stock allocation is obviously fraught with risk.

Because of this long bull market, some investors now have larger positions in equities than they originally planned. A portfolio once evenly held in equities and fixed income may now have a majority of its assets held in stocks, with the performance of stock markets influencing its return more than in the past.(1)

Yes, stock markets – as in stock markets worldwide.

Today, investors have more global exposure than they once did. In the 1990s, international holdings represented about 5% of an individual investor’s typical portfolio. Today, that has risen to about 15%. When overseas markets struggle, it does impact the return for many U.S. investors – and struggle they have. A strong dollar, the appearance of tariffs – these are considerable headwinds. (2,3)

In addition, a sudden change in sector performance can have an impact.

At one point in 2018, tech stocks accounted for 25% of the weight of the S&P 500. While the recent restructuring of S&P sectors lowered that by a few percentage points, portfolios can still be greatly affected when tech shares slide, as investors witnessed in fall 2018. (4)

How about the fixed-income market?

Well, this has been a weak year for bonds, and bonds are not known for generating huge annual returns to start with. (3)

This year, U.S. stocks have been out in front.

A portfolio 100% invested in the U.S. stock market would have a 2018 return like that of the S&P 500. But who invests entirely in stocks, let alone without any exposure to international and emerging markets? (3)

Just as an illustration, assume there is a hypothetical investor this year who is actually 100% invested in equities, as follows: 50% domestic, 35% international, 15% emerging markets. In the first two-thirds of 2018, that hypothetical portfolio would have advanced just 3.6%. (3)

Your portfolio is not the market – and vice versa.

Your investments might be returning 3% or less so far this year. Yes – this year. Will the financial markets behave in this exact fashion next year? Will the sector returns or emerging market returns of 2018 be replicated year after year for the next 10 or 15 years? The chances are remote.

The investment markets are ever-changing.

In some years, you may get a double-digit return. In other years, your return is much smaller. When your portfolio is diversified across asset classes, the highs may not be so high – but the lows may not be so low, either. When things turn volatile, diversification may help insulate you from some of the ups and downs you go through as an investor.

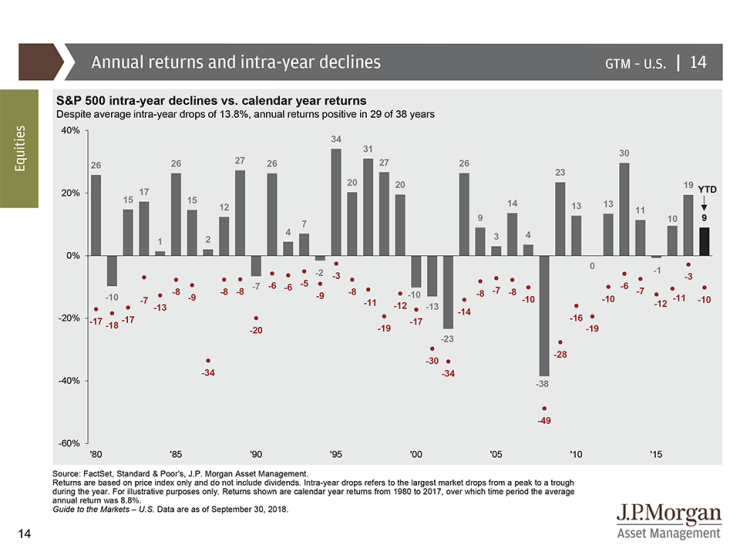

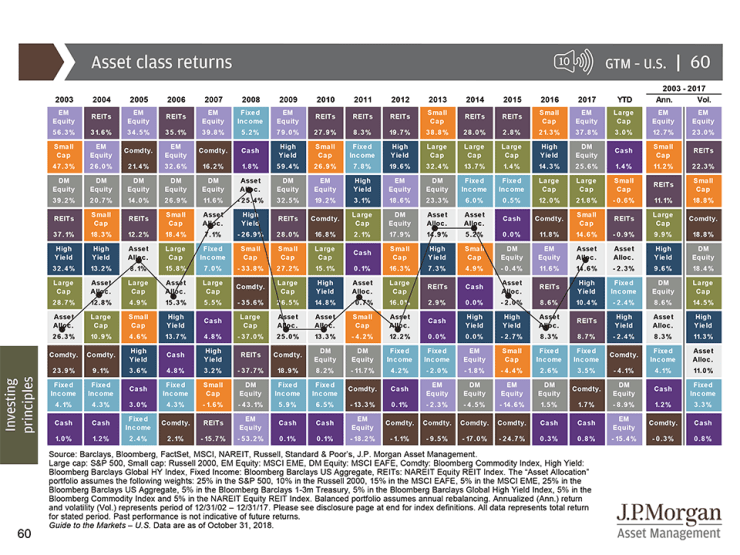

Asset class returns

This chart shows the historical performance and volatility of different asset classes, as well as an annually rebalanced asset allocation portfolio. The asset allocation portfolio incorporates the various asset classes shown in the chart and highlights that balance and diversification can help reduce volatility and enhance returns. (5)

Sources:

- seattletimes.com/business/5-steps-to-take-if-the-bull-market-run-has-you-thinking-of-unloading-stocks/

- forbes.com/sites/simonmoore/2018/08/05/how-most-investors-get-their-international-stock-exposure-wrong/

- thestreet.com/investing/stocks/dear-financial-advisor-why-is-my-portfolio-performing-so-14712955

- cnbc.com/2018/04/20/tech-dominates-the-sp-500-but-thats-not-always-a-bad-omen.html

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-the-markets/viewer

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.