Getting ready to retire or have you just started your retirement? Here are 7 important ages you should to be ready for:

AGE 55

Can Make Withdrawals Without 10% Penalty if Retired

At age 55 you can withdraw from your 401(k) or 403(b) plan without the 10% penalty if you retire or get fired. Also, if your employer offers a pension you may be eligible for full retirement benefits, if you meet the plan requirements.

AGE 59 1/2

Can Make Withdrawals Without 10% Penalty

This is an important age to remember. Once you turn 59 ½ you can withdraw money from IRA’s and deferred annuities without paying the 10% penalty for early withdrawal.

AGE 62

Can Start Reduced Social Security Benefits

This is another big year. At age 62 you can start receiving Social Security benefits. However, keep in mind your benefits will be reduced since you will not have reached full retirement age. The other thing is that at age 62 you may be eligible for full pension benefits if applicable to your situation.

AGE 65

Qualify for Medicare Benefits

This is when you qualify for medicare benefits. Also, with most pension plans you become eligible for your full benefits.

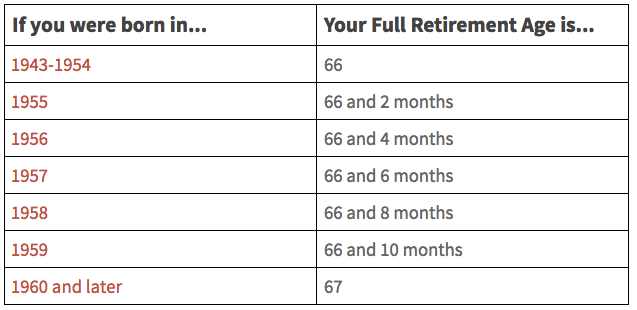

AGES 66 & 67

Eligible for Full Social Security Benefits

Ok, I have two ages here. But, they are pretty much for the same thing so I lumped them together. At age 66 you become eligible for full social security benefits, if you were born between 1943-1954. Everyone born after 1954 follows this table:

AGE 70

Your Social Security Benefits Max Out

Once you hit 70 you should start collecting your social security benefits if you haven’t already done so because your benefits will be maxed out. Waiting to collect benefits until age 70 can actually be a great strategy if you are trying to max out social security benefits or are concerned about longevity.

AGE 70 1/2

Must Start Your Required Minimum Distributions (RMD’s)

Finally, age 70 ½ . When you turn 70 ½ you will be required to start withdrawing specified amounts from your 401(k)’s and IRAs. This is called your Required Minimum Distribution or RMD for short. You must begin these withdrawals once your turn 70 ½ but you actually have until April 1st of the year following the year you actually turn age 70 1/2 . I know, confusing right? Let me give you an example. Let’s say you turn 70 ½ in January 2016, you will need to take your RMD by April 1st, of 2017. Now, you can take it in 2016 but you don’t have to. Going forward, every year after your first RMD you will be required to take the distribution buy December 31st.

Source: