Photo by Oleksandr Pidvalnyi on Pexels.com

Future financial needs may be underestimated.

If you were born during 1965-80, you belong to “Generation X.”

Ten or twenty years ago, you may have thought of retirement as an event in the lives of your parents or grandparents; within the next 10-15 years, you will probably be thinking about how your own retirement will unfold. (1)

According to the most recent annual retirement survey from the Transamerica Center for Retirement Studies, the average Gen Xer has saved only about $72,000 for retirement. Hypothetically, how much would that $72,000 grow in a tax-deferred account returning 6% over 15 years, assuming ongoing monthly contributions of $500? According to the compound interest calculator at Investor.gov, the answer is $312,208. Across 20 years, the projection is $451,627. (2,3)

Should any Gen Xer retire with less than $500,000?

Today, people are urged to save $1 million (or more) for retirement; $1 million is being widely promoted as the new benchmark, especially for those retiring in an area with high costs of living. While a saver aged 38-53 may or may not be able to reach that goal by age 65, striving for it has definite merit. (4)

Many Gen Xers are staring at two retirement planning shortfalls.

Our hypothetical Gen Xer directs $500 a month into a retirement account. This might be optimistic: Gen Xers contribute an average of 8% of their pay to retirement plans. For someone earning $60,000, that means just $400 a month. A typical Gen X worker would do well to either put 10% or 15% of his or her salary toward retirement savings or simply contribute the maximum to retirement accounts, if income or good fortune allows. (2)

How many Gen Xers have Health Savings Accounts (HSAs)?

These accounts set aside a distinct pool of money for medical needs. Unlike Flexible Spending Accounts (FSAs), HSAs do not have to be drawn down each year. Assets in an HSA grow with taxes deferred, and if a distribution from the HSA is used to pay qualified health care expenses, that money comes out of the account, tax free. HSAs go hand-in-hand with high-deductible health plans (HDHPs), which have lower premiums than typical health plans. A taxpayer with a family can contribute up to $7,000 to an HSA in 2019. (The limit is $8,000 if that taxpayer will be 55 or older at any time next year.) HSA contributions also reduce taxable income. (2,5)

Fidelity Investments projects that the average couple will pay $280,000 in health care expenses after age 65. A particular retiree household may pay more or less, but no one can deny that the costs of health care late in life can be significant. An HSA provides a dedicated, tax-advantaged way to address those expenses early. (6)

Retirement is less than 25 years away for most of the members of Generation X.

For some, it is less than a decade away. Is this generation prepared for the financial realities of life after work? Traditional pensions are largely gone, and Social Security could change in the decades to come. At midlife, Gen Xers must dedicate themselves to sufficiently funding their retirements and squarely facing the financial challenges ahead.

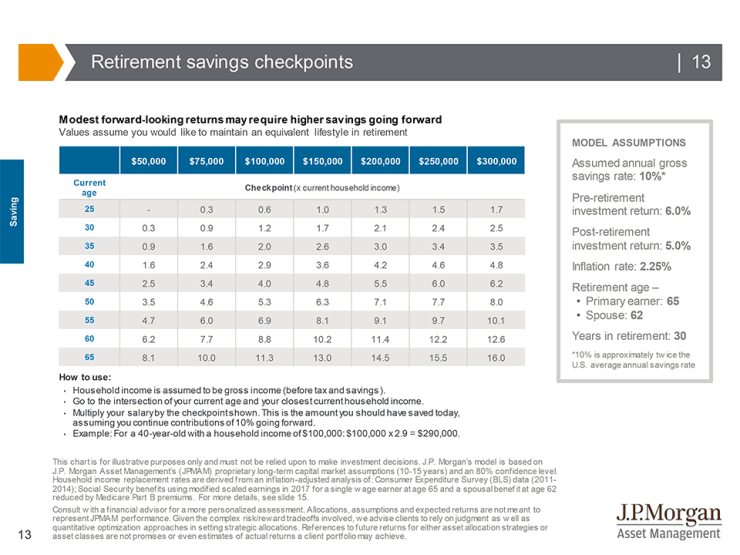

▲Retirement savings checkpoints

Achieving a financially successful retirement requires consistent savings, disciplined investing and a plan, yet too few Americans have calculated what it will take to be able to retire at their current lifestyle. This chart helps investors to quickly gauge whether they are “on track” to afford their current lifestyle for 30 years in retirement based on their current age and annual household income. This analysis uses an appropriate income replacement rate, an estimate of how much Social Security is likely to cover and the rate of return and inflation rate assumptions detailed on the right to determine the amount of investable wealth needed today, assuming a 10% gross annual savings rate until retirement. It is important to note that this analysis assumes a household with the primary earner who plans to retire at age 65 when the spouse is assumed to be 62. If an investor’s current retirement savings falls short of the amount for their age and income, developing a written retirement plan tailored to their unique situation with the help of an experienced financial advisor is a recommended next step. (6)

Sources:

- businessinsider.com/generation-you-are-in-by-birth-year-millennial-gen-x-baby-boomer-2018-3

- forbes.com/sites/megangorman/2018/05/27/generation-x-our-top-2-retirement-planning-priorities/

- investor.gov/additional-resources/free-financial-planning-tools/compound-interest-calculator

- washingtonpost.com/news/get-there/wp/2018/04/26/is-1-million-enough-to-retire-why-this-benchmark-is-both-real-and-unrealistic

- kiplinger.com/article/insurance/T027-C001-S003-health-savings-account-limits-for-2019.html

- fool.com/retirement/2018/11/05/3-reasons-its-not-always-a-good-idea-to-retire-ear.aspx

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.