Photo by rawpixel.com on Pexels.com

You can prepare for your retirement transition years before it occurs.

In doing so, you can do your best to avoid the kind of financial surprises that tend to upset an unsuspecting new retiree.

1. How much monthly income will you need?

Look at your monthly expenses and add them up. (Consider also the trips, adventures and pursuits you have in mind in the near term.) You may end up living on less; that may be acceptable, as your monthly expenses may decline. If your retirement income strategy was conceived a few years ago, revisit it to see if it needs adjusting. As a test, you can even try living on your projected monthly income for 2-3 months prior to retiring.

2. Should you downsize or relocate?

Moving into a smaller home may reduce your monthly expenses. If you will still be paying off your home loan in retirement, realize that your monthly income might be lower as you do so.

3. How should your portfolio be constructed?

In planning for retirement, the top priority is to build investments; within retirement, the top priority is generating consistent, sufficient income. With that in mind, portfolio assets may be adjusted or reallocated with respect to time, risk tolerance, and goals: it may be wise to have some risk-averse investments that can provide income in the next few years as well as growth investments geared to income or savings objectives on the long-term horizon.

4. How will you live?

There are people who wrap up their careers without much idea of what their day-to-day life will be like once they retire. Some picture an endless Saturday. Others wonder if they will lose their sense of purpose (and self) away from work. Remember that retirement is a beginning. Ask yourself what you would like to begin doing. Think about how to structure your days to do it, and how your day-to-day life could change for the better with the gift of more free time.

5. How will you take care of yourself?

What kind of health insurance do you have right now? If you retire prior to age 65, Medicare will not be there for you. Check and see if your group health plan will extend certain benefits to you when you retire; it may or may not. If you can stay enrolled in it, great; if not, you may have to find new coverage at presumably higher premiums.

Even if you retire at 65 or later, Medicare is no panacea. Your out-of-pocket health care expenses could still be substantial with Medicare in place. Extended care is another consideration – if you think you (or your spouse) will need it, should it be funded through existing assets or some form of LTC insurance?

Give your retirement strategy a second look as the transition approaches.

Review it in the company of the financial professional who helped you create and refine it. An adjustment or two before retirement may be necessary due to life or financial events.

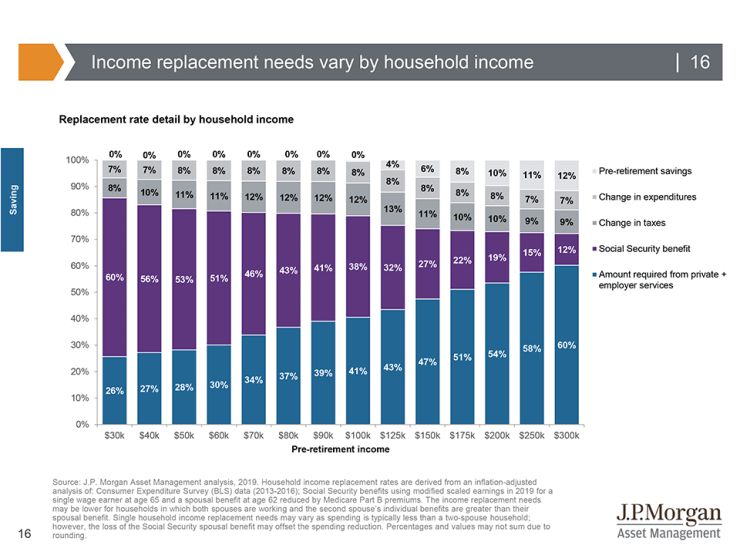

▲ Income replacement needs vary by household income

Income replacement needs in retirement vary by household income due to different levels of pre-retirement savings and changes in sp¹ending and income taxes. Based on J.P. Morgan research, this chart shows the percentage of pre-retirement income that may be needed to provide a comparable lifestyle through retirement. It also shows what percentage of that total income amount is estimated to come from Social Security to determine what amount will need to be covered by private sources, which include employer-provided retirement plans, IRAs, mutual funds, annuities and other investments.¹

Sources

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment. Investments seeking to achieve higher rate of return also involve a higher degree of risk.