Photo by rawpixel.com on Pexels.com

Whether your 65th birthday is on the horizon or decades away, you should understand the parts of Medicare – what they cover and where they come from.

Parts A & B: Original Medicare

There are two components. Part A is hospital insurance. It provides coverage for inpatient stays at medical facilities. It can also help cover the costs of hospice care, home health care, and nursing home care – but not for long and only under certain parameters. (1,2)

Seniors are frequently warned that Medicare will only pay for a maximum of 100 days of nursing home care (provided certain conditions are met). Part A is the part that does so. Under current rules, you pay $0 for days 1-20 of skilled nursing facility (SNF) care under Part A. During days 21-100, a $170.50 daily coinsurance payment may be required of you. (2)

Part B is medical insurance and can help pick up some of the tab for physical therapy, physician services, expenses for durable medical equipment (hospital beds, wheelchairs), and other medical services, such as lab tests and a variety of health screenings. (1)

Part B isn’t free. You pay monthly premiums to get it and a yearly deductible (plus 20% of costs). The premiums vary according to the Medicare recipient’s income level. The standard monthly premium amount is $135.50 this year. The current yearly deductible is $185. (Some people automatically receive Part B coverage, but others must sign up for it.) (3)

Part C: Medicare Advantage plans.

Insurance companies offer these Medicare-approved plans. To keep up your Part C coverage, you must keep up your payment of Part B premiums as well as your Part C premiums. To say not all Part C plans are alike is an understatement. Provider networks, premiums, copays, coinsurance, and out-of-pocket spending limits can all vary widely, so shopping around is wise. During Medicare’s annual Open Enrollment Period (October 15 – December 7), seniors can choose to switch out of Original Medicare to a Medicare Advantage plan or vice versa; although, any such move is much wiser with a Medigap policy already in place. (4,5)

How does a Medigap plan differ from a Part C plan? Medigap plans (also called Medicare Supplement plans) emerged to address the gaps in Part A and Part B coverage. If you have Part A and Part B already in place, a Medigap policy can pick up some copayments, coinsurance, and deductibles for you. You pay Part B premiums in addition to Medigap plan premiums to keep a Medigap policy in effect. These plans no longer offer prescription drug coverage. (6)

Part D: prescription drug plans.

While Part C plans commonly offer prescription drug coverage, insurers also sell Part D plans as a standalone product to those with Original Medicare. As per Medigap and Part C coverage, you need to keep paying Part B premiums in addition to premiums for the drug plan to keep Part D coverage going. (7)

Every Part D plan has a formulary, a list of medications covered under the plan. Most Part D plans rank approved drugs into tiers by cost. The good news is that Medicare’s website will determine the best Part D plan for you. Go to medicare.gov/find-a-plan to start your search; enter your medications and the website will do the legwork for you. (8)

▲ What is Medicare?

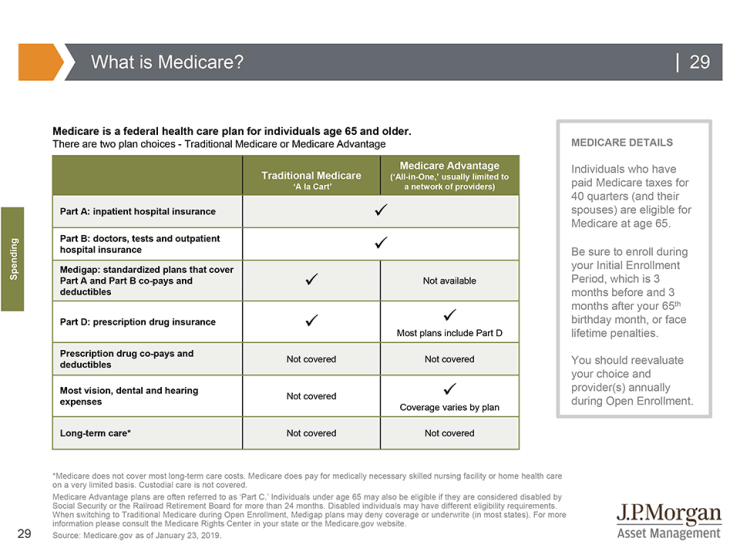

The left side of this table shows all the parts of Medicare. The next column to the right has a check mark for all the parts of Medicare that are included in traditional Medicare. Individuals sign up for the different parts, and Part A is usually free for most people. The column to the far right shows what is typically included in Medicare Advantage, which are local plans sold by private companies. Usually Medicare Advantage beneficiaries are limited to a local network of providers. During the annual enrollment period, beneficiaries may switch from traditional Medicare to Medicare Advantage and vice versa. However, Medigap, which covers the gaps in Parts A and B, is only available with traditional Medicare, and must be signed up for when first eligible or the individual may be denied coverage, face underwriting or incur higher premiums. Whichever plan an individual chooses, they should consider future coverage needs including drug coverage to avoid lifetime penalties when signing up later. (9)

Sources

- mymedicarematters.org/coverage/parts-a-b/whats-covered/

- medicare.gov/coverage/skilled-nursing-facility-snf-care

- medicare.gov/your-medicare-costs/part-b-costs

- medicareinteractive.org/get-answers/medicare-basics/medicare-coverage-overview/original-medicare

- medicare.gov/sign-up-change-plans/joining-a-health-or-drug-plan

- medicare.gov/supplements-other-insurance/whats-medicare-supplement-insurance-medigap

- ehealthinsurance.com/medicare/part-d-all/medicare-part-d-prescription-drug-coverage-costs

- https://www.medicare.gov/drug-coverage-part-d/what-drug-plans-cover

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.