No doubt the market gyrations of the last several weeks have rattled the nerves of many investors.

Sharp market declines and volatility are built around uncertainty, whether it be in the financial system (e.g. 2008), terrorist events (2001), commodity price shocks (1970s), wars, or other surprises. It’s easy for investors to forget in hindsight that the very nature of these historical events did not lend themselves to certain interpretation or resolution while they were happening. This is why the ‘price discovery’ mechanism of markets can get off-track, divergent from the more predictable modeling of earnings, dividends, and interest rates. (1)

“In the short run, stock returns are very volatile, driven by changes in earnings, interest rates, risk, and uncertainty, as well as psychological factors, such as optimism and pessimism as well as fear and greed.”

– Jeremy Segal “Stocks for the Long Run 5/E: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies”

In times like this, though, when information is fluid, estimates are difficult. The severity of the downturn and market reaction will likely depend on a variety of factors. These include government action and fiscal stimulus to assist those out of work in the service and entertainment industries, and, most importantly, the progression of COVID-19 cases, and any signs of these peaking or decelerating. When financial markets move beyond rational pricing, non-financial indicators take on greater importance than they normally would. (1)

“It took just over 15 years to recover the money invested at the 1929 peak… And since World War II, the recovery period for stocks has been even better. Even including the recent financial crisis (2008), which saw the worst bear market since the 1930s, the longest it has ever taken an investor to recover an original investment in the stock market (including reinvested dividends) was the five-year, eight-month period from August 2000 through April 2006.”

– Jeremy Segal “Stocks for the Long Run 5/E: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies”

So, what should we as rational investors do to maintain a cool head amongst all this volatility and uncertainty?

5 Investing Principles for This Tumultuous Market

Dr. David Kelly, chief global strategist of J.P. Morgan Asset Management, recently suggested (2):

- Recognize that stocks are long-term investments – Historically stocks tend to overreact on both the upside and the downside and eventually recover.

- Recognize that the market has already de-risked investors – You may now have less equity exposure.

- Look at valuation gaps – Not every investment is equally priced.

- Think about income – The S&P 500 yield is greater than current Treasury yields.

- Active managers should do well during this period – Mutual Fund managers can help us navigate these choppy waters and help separate the potential winners from the losers.

The Markets Will Adapt

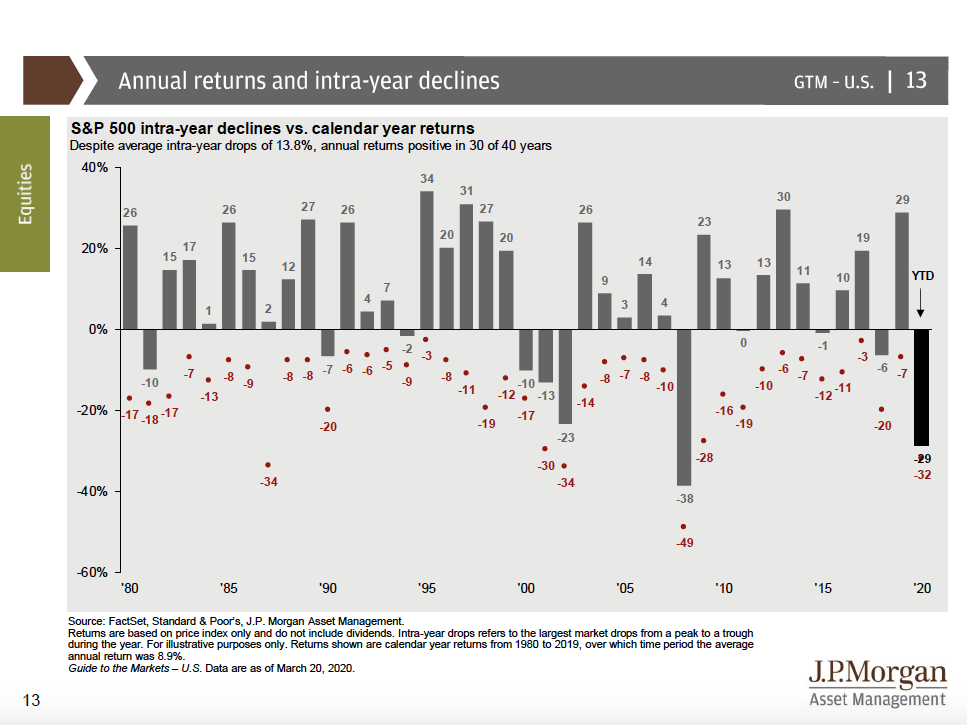

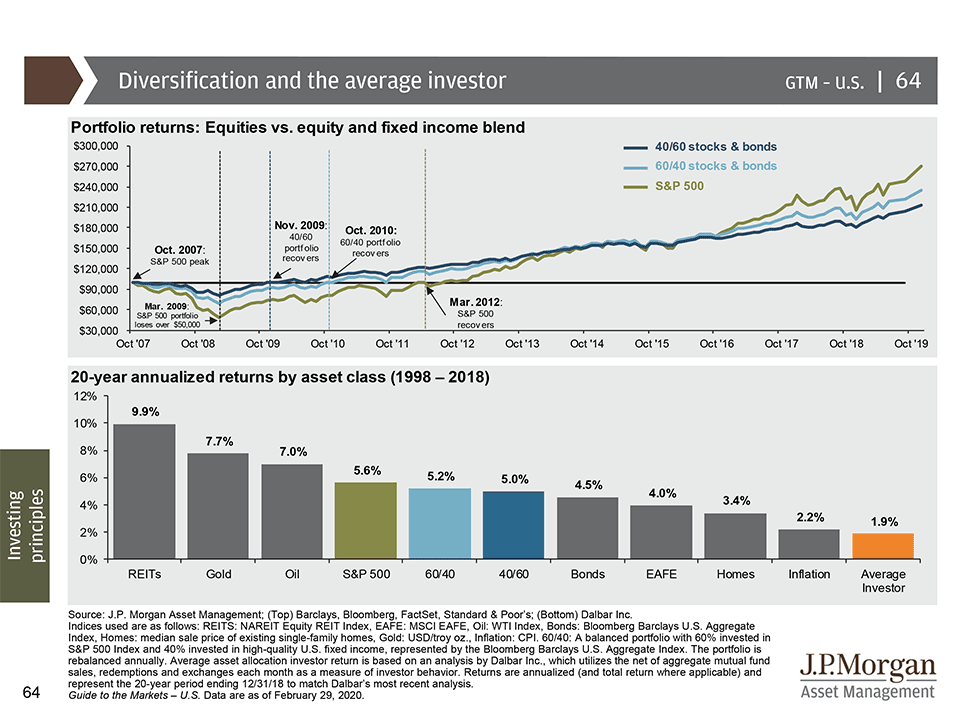

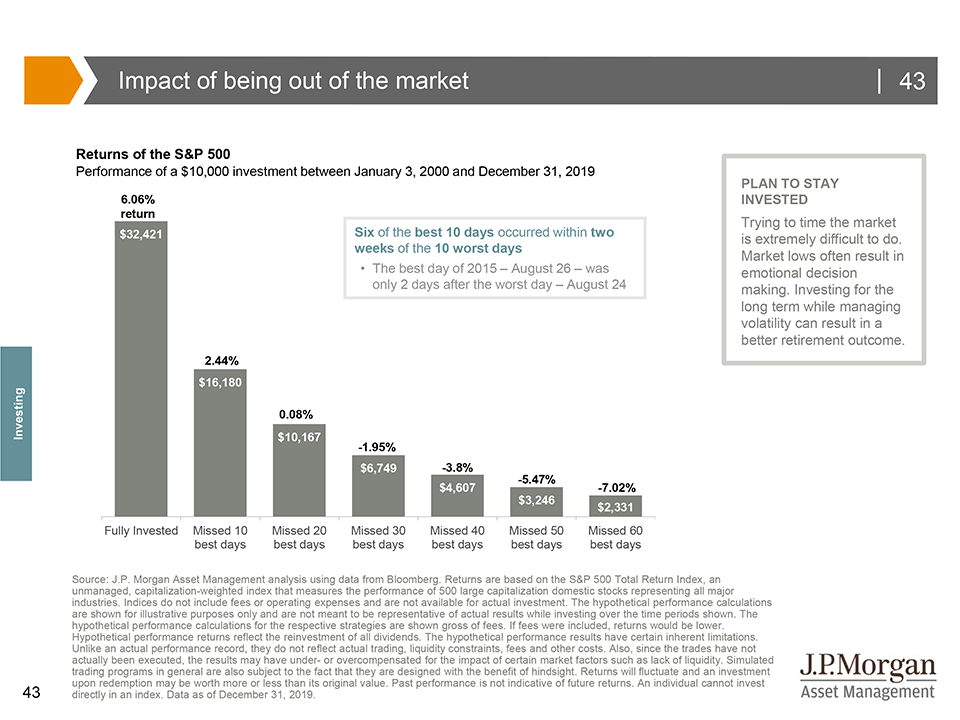

If you believe, like I do, that we will eventually recover from this crisis then we’ll need to lean into what we do know from past market (and investor) behavior. Here are four charts that help provide a better understanding (click charts for expanded view):

The bottom chart shows 20-year annualized returns by asset class, as well as how an “average investor” would have fared. The average investor asset allocation return is based on an analysis by Dalbar, which utilizes the net of aggregate mutual fund sales, redemptions and exchanges each month as a measure of investor behavior. (3) Carl Richards coined this the “Behavior Gap” in his book “The Behavior Gap: Simple Ways to Stop Doing Dumb Things with Money”

Sources:

- LSA Portfolio Analytics

- https://www.thinkadvisor.com/2020/03/20/jpmorgans-kelly-5-investing-principles-for-this-tumultuous-market/

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-the-markets

- https://www.amazon.com/Behavior-Gap-Simple-Doing-Things/dp/1591844649/ref=sr_1_1?dchild=1&keywords=the+behavior+gap&qid=1584981929&sr=8-1

- https://www.amazon.com/dp/0071800514/?coliid=I2TQ2AX89NOD8Q&colid=2ECH1J1LBJRKC&psc=1&ref_=lv_ov_lig_dp_it_im