Whether you want to leave work at 62, 67, or 72, claiming the retirement benefits you are entitled to by federal law is no casual decision. You will want to consider a few key factors first.

How long do you think you will live?

If you have a feeling you will live into your nineties, for example, it may be better to claim later. If you start receiving Social Security benefits at or after Full Retirement Age (which varies from age 66 to 67 for those born in 1943 or later), your monthly benefit will be larger than if you had claimed at 62. If you file for benefits at FRA or later, chances are you probably a) worked into your mid-sixties, b) are in fairly good health, and c) have sizable retirement savings. (1)

If you really need retirement income, then claiming at or close to 62 might make more sense. If you have an average lifespan, you will, theoretically, receive the average amount of lifetime benefits regardless of when you claim them. Essentially, the choice comes down to more lifetime payments that are smaller versus fewer lifetime payments that are larger. For the record, Social Security’s actuaries project that the average 65-year-old man to live 84.0 years, and the average 65-year-old woman, 86.5 years. (2)

Will you keep working?

You might not want to work too much, since earning too much income may result in your Social Security being withheld or taxed.

Prior to Full Retirement Age, your benefits may be lessened if your income tops certain limits. In 2018, if you are aged 62 to 65, receive Social Security, and have an income over $17,040, $1 of your benefits will be withheld for every $2. If you receive Social Security and turn 66 later this year, then $1 of your benefits will be withheld for every $3 that you earn above $45,360. (3)

Social Security income may also be taxed above the program’s “combined income” threshold. (“Combined income” = adjusted gross income + nontaxable interest + 50% of Social Security benefits.) Single filers who have combined incomes from $25,000 to $34,000 may have to pay federal income tax on up to 50% of their Social Security benefits, and that also applies to joint filers with combined incomes of $32,000 to $44,000. Single filers with combined incomes above $34,000 and joint filers whose combined incomes surpass $44,000 may have to pay federal income taxes on up to 85% of their Social Security benefits. (3)

When does your spouse want to file?

Timing does matter, especially for two-income couples. If the lower-earning spouse collects Social Security benefits first, and then the higher-earning spouse collects them later, that may result in greater lifetime benefits for the household. (4)

Finally, how much in benefits might be coming your way?

Visit SSA.gov to find out, and keep in mind that Social Security calculates your monthly benefit using a formula based on your 35 highest-earning years. If you have worked for less than 35 years, Social Security fills in the “blank years” with zeros. If you have, say, just 33 years of work experience, working another couple years might translate to a slightly higher Social Security income. (1)

A claiming decision may be one of the most significant financial decisions of your life. Your choices should be evaluated years in advance – with insight from the financial professional who has helped you plan for retirement.

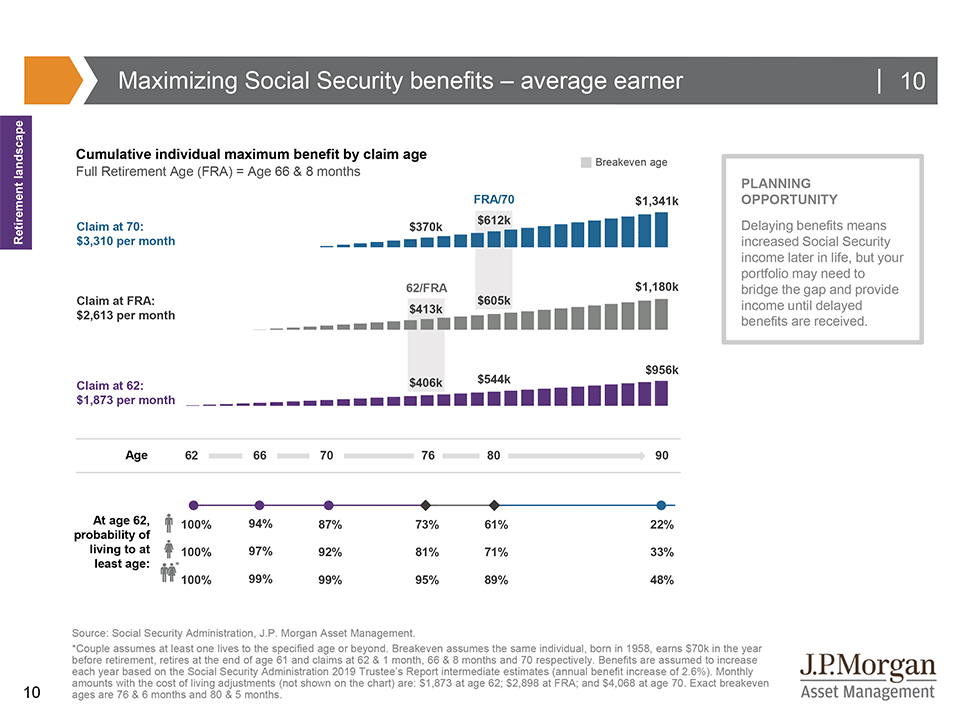

Maximizing Social Security benefits (average earner)

The age at which one claims Social Security greatly affects the amount of benefit received. Key claiming ages are 62, Full Retirement Age (FRA is currently 66 and 8 months for individuals turning 62 in 2020) and 70, as shown in the row of ages in the middle of the slide. The top three graphs show the three most common ages an individual is likely to claim and the monthly benefit he or she would receive at those ages, assuming average earnings at retirement of $70,000 (based on JPMorgan research). Claiming at the latest age (70) provides the highest monthly amount but delays receipt of the benefit for 8 years. Claiming at Full Retirement Age, 66 and 8 months, or at 62 years old provides lesser amounts at earlier ages. The bars represent the cumulative value of benefits received by the specified age. The gray shading between the bar charts represents the ages at which waiting until a later claim age results in greater cumulative benefits than claiming at the earlier age. This is called the “breakeven age.” The breakeven age between taking benefits at age 62 and FRA is age 76 and between FRA and 70 is 80. Along the bottom of the page, the percentages shown are the probability that a man, woman or one member of a married couple currently age 62 will live to the specified ages or beyond. Comparing these percentages against the breakeven ages will help a beneficiary make an informed decision about when to claim Social Security if maximizing the cumulative benefit received is a primary goal.

Note that while the benefits shown are for an average earner, the breakeven ages would be the same for those with other earnings histories.

Sources

- MarketWatch.com

- SSA.gov

- BlackRock.com

- MarketWatch.com

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.