Retirement Planning is Not Entirely Financial

Your degree of happiness in your “second act” may depend on some factors that don’t come with an obvious price tag. Here are some non-monetary factors to consider as you plan your retirement.

What Will You Do With Your Time?

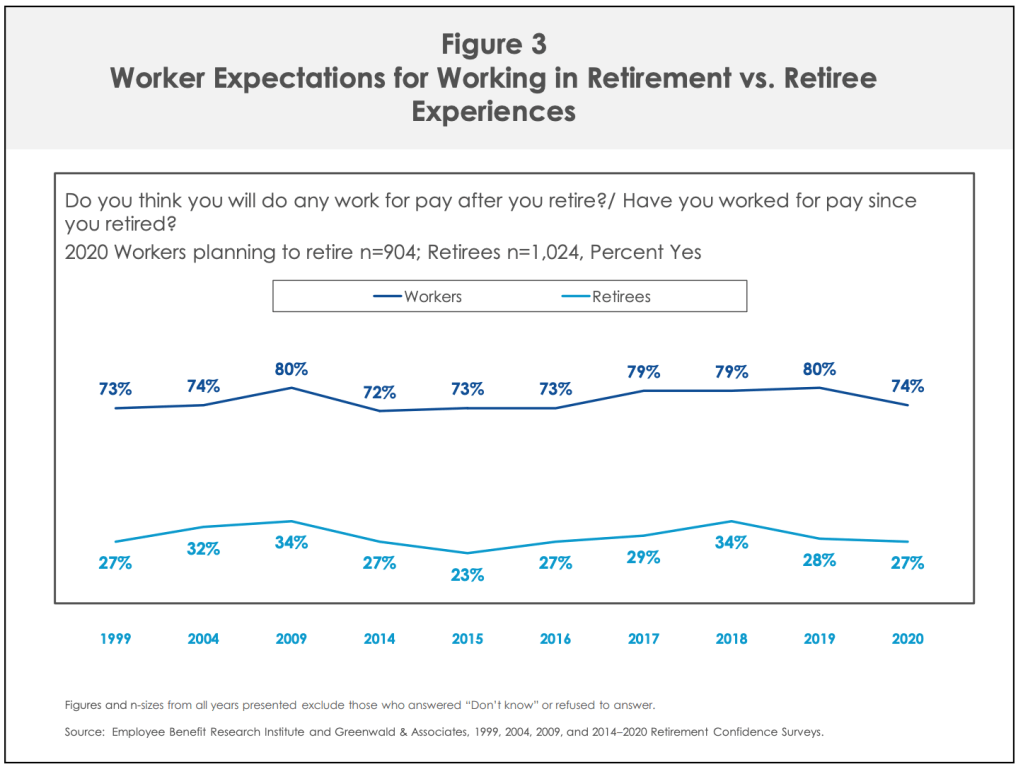

Too many people retire without any idea of what their retirement will look like. They leave work, and they cannot figure out what to do with themselves, so they grow restless. It’s important to identify what you want your retirement to look like and what you see yourself doing. Maybe you love your career, and can’t imagine not working during your retirement. There’s no hard and fast rule to your dream retirement, so it’s important to be honest with yourself. An EBRI retirement confidence survey shows that almost 74% of retirees plan to work for pay, whereas just 27% of retirees report that they’ve actually worked for pay. (1)

While this concept doesn’t have a monetary value, having a clear vision for your retirement may help you align your financial goals. It’s important to remember that your vision for retirement may change—like deciding you don’t want to continue working after all.

Where Will You Live?

This is another factor in retirement happiness. If you can surround yourself with family members and friends whose company you enjoy, in a community where you can maintain old friendships and meet new people with similar interests or life experience, that is a definite plus. If all this can occur in a walkable community with good mass transit and senior services, all the better. Moving away from the life you know to a spread-out, car-dependent suburb where anonymity seems more prevalent than community may not be the best decision for you.

How Are You Preparing to Get Around in Your Eighties and Nineties?

The actuaries at Social Security project that the average life expectancy for men is 84 years old, and the life expectancy for women is 86.5 years. Some will live longer. Say you find yourself in that group. What kind of car would you want to drive at 85 or 90? At what age would you cease driving? Lastly, if you do stop driving, who would you count on to help you go where you want to go and get out in the world? (2)

How Will You Keep Up Your Home?

At 45, you can tackle that bathroom remodel or backyard upgrade yourself. At 75, you will probably outsource projects of that sort, whether or not you stay in your current home. You may want to move out of a single-family home and into a townhome or condo for retirement. Regardless of the size of your retirement residence, you will probably need to fund minor or major repairs, and you may need to find reliable and affordable sources for gardening or landscaping.

These are the non-financial retirement questions that no pre-retiree should dismiss. Think about them as you prepare and invest for the future.

▲Working for Pay in Retirement

“Nearly 3 in 4 workers (74 percent) plan to work for pay in retirement, compared with just 27 percent of retirees who report they have actually worked for pay in retirement. In fact, the RCS has consistently found that workers are far more likely to plan to work for pay in retirement than retirees are to have actually worked (Figure 3). In the 2019 RCS, among retirees who worked for pay in retirement reported why they worked for pay in retirement and almost all gave a positive reason for doing so, saying they continued to work because they wanted to stay active and involved (91 percent), they enjoyed working (89 percent), or a job opportunity came along (58 percent). a Retirees could have retired for more than one reason. However, they reported that financial reasons also played a role in that decision, such as wanting money to buy extras (75 percent), needing money to make ends meet (37 percent), a decrease in the value of their savings or investments (28 percent), or keeping health insurance or other benefits (16 percent). *Retirees could have worked for pay in retirement for more than one reason.” (1)

Sources

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.