Photo by Pixabay on Pexels.com

When you reach age 70½, the Internal Revenue Service instructs you to start making withdrawals from your traditional IRA(s). These withdrawals are also called Required Minimum Distributions (RMDs). You will make them, annually, from now on. (1)

If you fail to take your annual RMD or take out less than the required amount, the I.R.S. will notice. You will not only owe income taxes on the amount not withdrawn, you will owe 50% more. (The 50% penalty can be waived if you can show the I.R.S. that the shortfall resulted from a “reasonable error” instead of negligence.) (1)

Many IRA owners have questions about the rules related to their initial RMDs, so let’s answer a few.

How does the I.R.S. define age 70½?

Its definition is pretty straightforward. If your 70th birthday occurs in the first half of a year, you turn 70½ within that calendar year. If your 70th birthday occurs in the second half of a year, you turn 70½ during the subsequent calendar year. (2)

Your initial RMD has to be taken by April 1 of the year after you turn 70½. All the RMDs you take in subsequent years must be taken by December 31 of each year. (1)

So, if you turned 70 during the first six months of 2020, then you will be 70½ by the end of 2020, and you must take your first RMD by April 1, 2021. If you turn 70 in the second half of 2020, then you will be 70½ in 2021, and you won’t need to take that initial RMD until April 1, 2022. (1)

Is waiting until April 1 of the following year to take my first RMD a bad idea?

The I.R.S. allows you three extra months to take your first RMD, but it isn’t necessarily doing you a favor. Your initial RMD is taxable in the year that it is taken. If you postpone it into the following year, then the taxable portions of both your first RMD and your second RMD must be reported as income on your federal tax return for that following year. (2)

An example: James and his wife Stephanie file jointly, and they earn $78,950 in 2019 (the upper limit of the 22% federal tax bracket). James turns 70½ in 2019, but he decides to put off his first RMD until April 1, 2020. Bad idea: this means that he will have to take two RMDs before 2020 ends. So, his taxable income jumps in 2020 as a result of the dual RMDs, and it pushes the pair into a higher tax bracket for 2020 as well. The lesson: if you will be 70½ by the time 2019 ends, take your initial RMD by the end of 2019 – it might save you thousands in taxes to do so. (3)

How do I calculate my first RMD?

I.R.S. Publication 590 is your resource. You calculate it using I.R.S. life expectancy tables and your IRA balance on December 31 of the previous year. For that matter, if you Google “how to calculate your RMD,” you will see links to RMD worksheets at irs.gov and a host of other free online RMD calculators. (1,4)

If your spouse is more than 10 years younger than you and happens to be designated as the sole beneficiary for one or more of the traditional IRAs that you own, you should use the I.R.S. IRA Minimum Distribution Worksheet (downloadable as a PDF online) to help calculate your RMD. (5)

If your IRA is held at one of the big investment firms, that firm may calculate your RMD for you and offer to route the amount into another account of your choice. It will give you and the I.R.S. a 1099-R form recording the income distribution and the amount of the distribution that is taxable. (6)

When I take my RMD, do I have to withdraw the whole amount?

No. You can also take it in smaller, successive withdrawals. Your IRA custodian may be able to schedule them for you. (7)

What if I have more than one traditional IRA?

You then figure out your total RMD by calculating the RMD for each traditional IRA you own, using the IRA balances on the prior December 31. This total is the basis for the RMD calculation. You can take your RMD from a single traditional IRA or multiple traditional IRAs. (1)

What if I have a Roth IRA?

If you are the original owner of that Roth IRA, you don’t have to take any RMDs. Only inherited Roth IRAs require RMDs. (7)

Be proactive when it comes to your first RMD

Putting off the initial RMD until the first quarter of next year could mean higher-than-normal income taxes for the year ahead. (2)

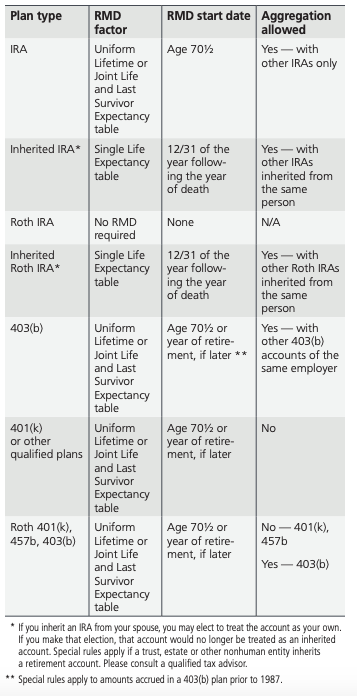

▼RMDs at a Glance for All Account Types

Sources

- irs.gov/Retirement-Plans/Retirement-Plans-FAQs-regarding-Required-Minimum-Distributions

- kiplinger.com/article/retirement/T045-C032-S014-avoid-the-5-biggest-ira-rmd-mistakes.html

- taxfoundation.org/2019-tax-brackets/

- google.com/search?client=firefox-b-1-d&q=how+to+calculate+your+RMD

- irs.gov/pub/irs-tege/jlls_rmd_worksheet.pdf

- finance.zacks.com/everyone-ira-1099r-4710.html

- fidelity.com/viewpoints/retirement/smart-ira-withdrawal-strategies

- https://static.twentyoverten.com/58e639ce21cca2513c90975b/CMPlElT87-y/RMDMFSFlyer.pdf

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.