Photo by rawpixel.com on Pexels.com

Thinking about borrowing money from your 401(k), 403(b), or 457 account?

Think twice about that because these loans are not only risky, but injurious, to your retirement planning.

A loan of this kind damages your retirement savings prospects.

A 401(k), 403(b), or 457 should never be viewed like a savings or checking account. When you withdraw from a bank account, you pull out cash. When you take a loan from your workplace retirement plan, you sell shares of your investments to generate cash. You buy back investment shares as you repay the loan. (1)

In borrowing from a 401(k), 403(b), or 457, you siphon down invested retirement assets, leaving a smaller account balance that experiences a smaller degree of compounding. In repaying the loan, you will likely repurchase investment shares at higher prices than in the past – in other words, you will be buying high. None of this makes financial sense.(1)

Most plan providers charge an origination fee for a loan (it can be in the neighborhood of $100), and of course, they charge interest. While you will repay interest and the principal as you repay the loan, that interest still represents money that could have remained in the account and remained invested.1,2

As you strive to repay the loan amount, there may be a financial side effect. You may end up reducing or suspending your regular per-paycheck contributions to the plan. Some plans may even bar you from making plan contributions for several months after the loan is taken. (3,4)

Your take-home pay may be docked.

Most loans from 401(k), 403(b), and 457 plans are repaid incrementally – the plan subtracts X dollars from your paycheck, month after month, until the amount borrowed is fully restored. (1)

If you leave your job, you will have to pay 100% of your 401(k) loan back.

This applies if you quit; it applies if you are laid off or fired. Formerly, you had a maximum of 60 days to repay a workplace retirement plan loan. The Tax Cuts & Jobs Act of 2017 changed that for loans originated in 2018 and years forward. You now have until October of the year following the year you leave your job to repay the loan (the deadline is the due date of your federal taxes plus a 6-month extension, which usually means October 15). You also have a choice: you can either restore the funds to your workplace retirement plan or transfer them to either an IRA or a workplace retirement plan elsewhere.(2)

If you are younger than age 59½ and fail to pay the full amount of the loan back, the I.R.S. will characterize any amount not repaid as a premature distribution from a retirement plan – taxable income that is also subject to an early withdrawal penalty. (3)

Even if you have great job security, the loan will probably have to be repaid in full within five years.

Most workplace retirement plans set such terms. If the terms are not met, then the unpaid balance becomes a taxable distribution with possible penalties (assuming you are younger than 59½.(1)

Would you like to be taxed twice?

When you borrow from an employee retirement plan, you invite that prospect. You will be repaying your loan with after-tax dollars, and those dollars will be taxed again when you make a qualified withdrawal of them in the future (unless your plan offers you a Roth option). (3,4)

Why go into debt to pay off debt?

If you borrow from your retirement plan, you will be assuming one debt to pay off another. It is better to go to a reputable lender for a personal loan; borrowing cash has fewer potential drawbacks.

You should never confuse your retirement plan with a bank account.

Some employees seem to do just that. Fidelity Investments says that 20.8% of its 401(k) plan participants have outstanding loans in 2018. In taking their loans, they are opening the door to the possibility of having less money saved when they retire. (4)

Why risk that? Look elsewhere for money in a crisis. Borrow from your employer-sponsored retirement plan only as a last resort.

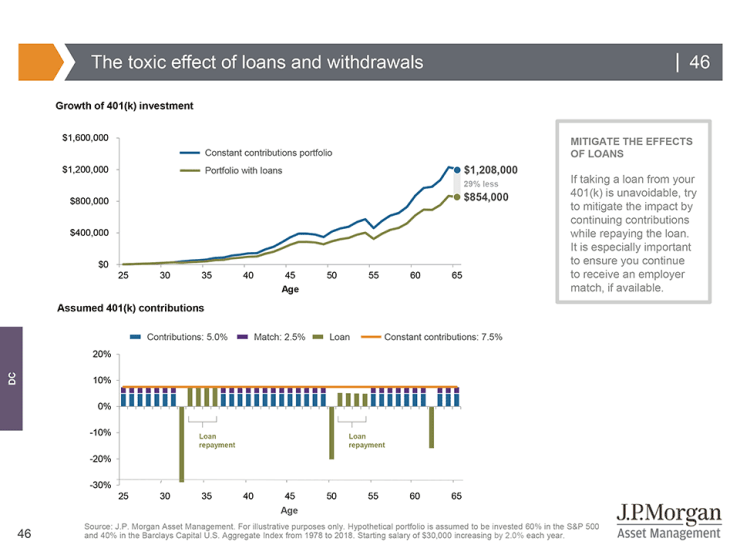

▲The toxic effect of loans and withdrawals

The top chart shows that employees who took loans and a withdrawal from their account may end up with significantly lower balances in the end. The bottom chart shows that the employee did not get the benefit of contributions and company match when paying back their loans. To avoid this scenario, stress the importance of an emergency reserve and savings for other goals outside of the retirement account. If the employee must borrow, if they keep contributing while paying back the loan that may mitigate the negative impact of the loan.

Sources

- gobankingrates.com/retirement/401k/borrowing-401k/

- forbes.com/sites/ashleaebeling/2018/01/16/new-tax-law-liberalizes-401k-loan-repayment-rules/

- cbsnews.com/news/when-is-it-ok-to-withdraw-or-borrow-from-your-retirement-savings/

- cnbc.com/2018/06/26/the-lure-of-a-401k-loan-could-mask-its-risks.html

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.