The impact of a potential new President on stock market returns is always a key question in the weeks prior to a general election. It’s important to keep in mind that, despite frequent worries around this time of year, and that financial markets may react in the shorter-term term to poll results and election outcomes (especially surprises), the longer-term effects of any administration’s policies appear to be disconnected from financial market results. Instead, stocks especially tend to follow earnings, which follow economic growth trends. Nevertheless, there are always policy distinctions that could affect various industries to some extent.

In contrast to election season norms in prior decades, polarization between the two parties has become more pronounced, with more extreme positions on both sides forcing candidates away from traditional ‘centrist’ policy often adopted during general election campaigns. A Biden victory has the potential of moving policy toward a more progressive stance, although this is not as simple of a story as in past years, with the current administration having taken a variety of unconventional stances in its own right.

The potential retaking of the Senate by Democrats, in addition to their already holding power in the House, would heighten the risk of more progressive policies being voted in—with minimal opposition. On the other hand, Republicans successfully retaining the Senate would continue to act as an effective counterbalance against legislation from the House, potentially resulting in a policy log jam for the next four years. (Some see this as a best-case scenario, although doing little to alleviate the high current levels of political disagreement.)

The following represent a few areas that could be most impacted by a new Democratic administration, through either new legislation, reversals of prior policies, or no change:

Taxes

It is assumed that the corporate and personal tax cuts put into place in the current regime could be reversed—partially or fully—towards prior levels. Personal income tax policy rhetoric during the campaign has been aimed at the ultra-wealthy, but with high budget deficits and an unprecedented level of fiscal debt, higher tax rates for even middle-income Americans have been feared. This includes higher capital gains tax rates, seen as benefitting the wealthy the most, as they own the majority of financial assets. ‘Wealth taxes’ based on assets are out there as a wildcard as well (although targeted at billionaires). Even if corporate rates do not return to prior max levels of 35%, they are likely not to remain at 21%, either. Most directly, higher tax rates for companies directly erode multi-year earnings projections, which could result in lower stock valuation assessments.

Environment

This multi-faceted policy area includes not only ‘green’ legislation (likely to be promoted by a Biden administration), but also important carryover effects related to the energy industry broadly. It would likely be unfavorable for traditional petroleum- and coal-based energy production (and emissions), including limitations for drilling, and increased regulation of impacts. Conversely, alternative energy sources would likely be promoted—including wind and solar—as well as the potential taxation of carbon emissions.

U.S.-China Relations and Trade

This is a more challenging policy point, as both parties have adopted a hard line on China—for a variety of different reasons. The current administration has taken a more confrontational approach. This has been unique relative to prior regimes, which, at least at the surface, had attempted to avoid outright hostile language and direct economic sanctions. While the two parties agree in principle for a tougher stance, Republicans have focused this effort on corporate intellectual property, while Democrats have also included human rights concerns; specifically, based on the treatment of several ethnic and religious minority groups within the country. This remains a wildcard to some degree, but the majority of Americans and politicians now favor a tougher stance toward China—a rare point of policy agreement.

Antitrust Legislation

This wouldn’t normally surface as a key policy platform, but the rise of several technology behemoths has raised questions over the competitive environment and growing economic power of these firms. In prior decades, pro-business conservative politicians have been more reluctant to attack oligopolistic entities, while populist/progressive movements had been responsible for breaking up dominant ‘Robber Baron’ firms—such as Rockefeller’s Standard Oil in the early 1900’s. In recent years, though, the more progressively-minded tech giants have been supportive of the Democratic agenda and drawing the ire of Republicans—creating a role reversal. The pressure on these firms may continue to some degree, depending on who’s in charge. Some of this oligopolistic power is due to the structures of the industries. They’ve remained among the most fundamentally solid from a financial standpoint during the pandemic, which has rewarded investors. Of course, many small businesses have not fared nearly as well, fanning the flames of resentment.

Workers

Republican policies over the years have generally been focused on letting ‘laissez faire’ (free market) forces determine market competition and pricing dynamics—favored by many mainstream economists. Biden policies would likely offer more worker-friendly populist concessions, such as a higher minimum wage, better health coverage, paid leave, student loan relief, etc. On one hand, additional benefits and pay cut into company profit margins. On the other hand, more money in the pockets of consumers could be a catalyst for broader personal spending and consumption growth broadly, which benefits the broader economy in its own way.

Healthcare

The formation of the Affordable Care Act (‘Obamacare’) was followed by an immediate battle for repeal by Republicans and expansion by Democrats. This fight is likely to continue, with any enhancements in coverage (like ‘Medicare For All’) or other changes aimed at high prescription drug prices (also favored by the current administration, despite potential impact on corporate profits). Some pharmaceutical firms have acted to pre-emptively curb pricing for some drugs in efforts to stem the criticism and potentially unfavorable legislation. These firms counter that such high prices act as the funding mechanism for continued research and development on new therapeutics, which many politicians have accepted. The convoluted health care system, though, continues to overwhelm attempts at reform, which has led to a lower financial market probability for radical change in the near-term.

Defense

In prior years, a strong defense budget and global projection of power has been a Republican party tenet. Lately, this has taken a bit of an opposite turn with conservatives moving more towards a stance of isolation, and progressives seeking to maintain greater globalism. This may be an area with little net change, absent geopolitical surprises (which can be counted on).

Immigration

This doesn’t seem like a market-related topic at first glance, but movement of people across borders affects demographics, which, in turn, affects the size of the labor force and productivity—and ultimately economic growth. This has been a divisive issue throughout America’s history, and each side currently has a mixed relationship with it. Generally, economists argue that a more lenient immigration policy provides a larger pool of workers, which results in not only higher production but also higher consumption. Companies have often silently been in favor of these less restrictive policies, which brings in a higher supply of workers, which lowers wages and boosts profits. On the other side, and often in conflict with other elements of the party, Democratic politicians have tended to have strong support from unionized U.S. workers, which often oppose globalism and foreign worker competition—in efforts to retain jobs and sustain higher wages domestically. Realistically, on net, there could be few extreme changes due to these continual conflicts.

Fiscal Policy

In decades of old, Republicans were seen as the fiscally spendthrift party, while Democrats were cast in debates as ‘tax-and-spend.’ But even prior to the Covid recession, these traditional labels were less applicable, with higher spending proposed on all sides. Due to economic woes from the pandemic likely carrying over into 2021, and perhaps 2022, as well as increasing acceptance of policies such as Modern Monetary Theory (MMT), it appears the accepted spending may continue regardless of the party in office. However, at the fringes, Democrats have proposed more direct relief to workers, and Republicans to small businesses, in keeping with other distinct policy preferences.

Monetary Policy

This should be unaffected by politics, and largely has been over the years. Of course, there have been notable and theatrical exceptions, such as the Fed Chair being physically bullied at LBJ’s Texas ranch in the 1960’s, and the current President’s urging of low rates via social media. A Biden presidency could likely feature more restraint, and a conventional ‘hands off’ approach. However, the Fed could be increasingly impacted by the large Federal deficit and rising debt load, which affects both interest payment obligations as well as credit rating—which affect rates outside of the Fed’s control.

In short, by looking at individual industries, the outlook may not appear to change that much, aside from policy preferences one way or another. The key differences relate to tax policy, the broader regulatory environment, and fiscal spending policies.

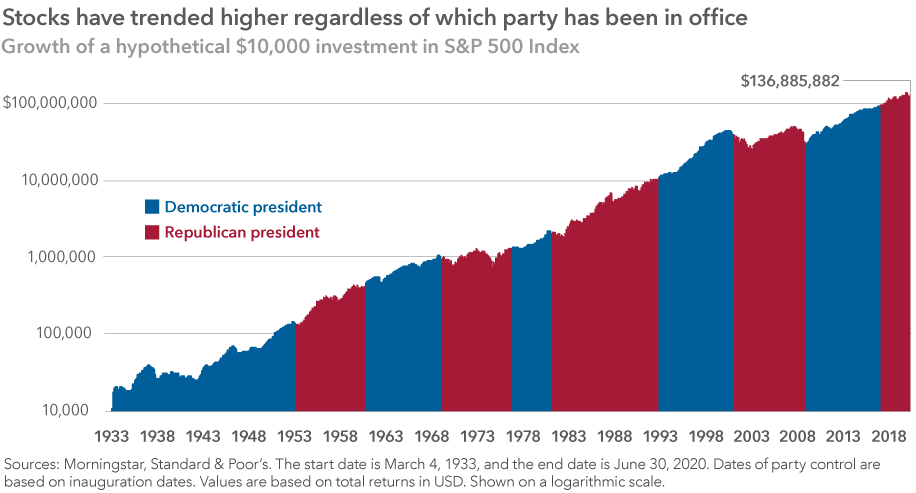

It’s important to remember that an elected President has very little effect on market results, historically. In fact, some of the stronger periods of market performance have been under Democratic administrations, contrary to popular assumption. (1)

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

- Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

- Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

- Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

Sources

Trackbacks and Pingbacks

[…] policies to expect would likely be similar to what’s in place today, and largely opposite of those proposed under a Biden administration. At the same time, Trump’s policies have not followed ‘traditional’ Republican ideologies from […]

LikeLike