On October 13, 2021, the Social Security Administration (SSA) officially announced that Social Security recipients will receive a 5.9 percent cost-of-living adjustment (COLA) for 2022, the largest increase in four decades. This adjustment will begin with benefits payable to more than 64 million Social Security beneficiaries in January 2022. Additionally, increased payments to more than 8 million Supplemental Security Income (SSI) beneficiaries will begin on December 31, 2021. (1)

Biggest COLA Increase in Decades?

While many predicted a bump of as much as 6.1% given recent movement in the Consumer Price Index (CPI), the announced 5.9% increase is still substantial. Some fear that rising consumer prices may dilute the impact of the increase with inflation currently running at more than 5 percent. While this remains to be seen, Social Security beneficiaries will no doubt welcome the largest adjustment in many years.1

How You Will Be Notified

According to the Social Security Administration, Social Security and SSI beneficiaries are usually notified about their new benefit amount by mail starting in early December. However, if you’ve set up your SSA online account, you will also be able to view your COLA notice online through your “My Social Security” account. (1)

Next Steps?

If this increase surprises or concerns you, it’s always a good idea to seek guidance from your financial professional about changes to any of your sources of retirement income. I welcome a chance to talk with you about this.

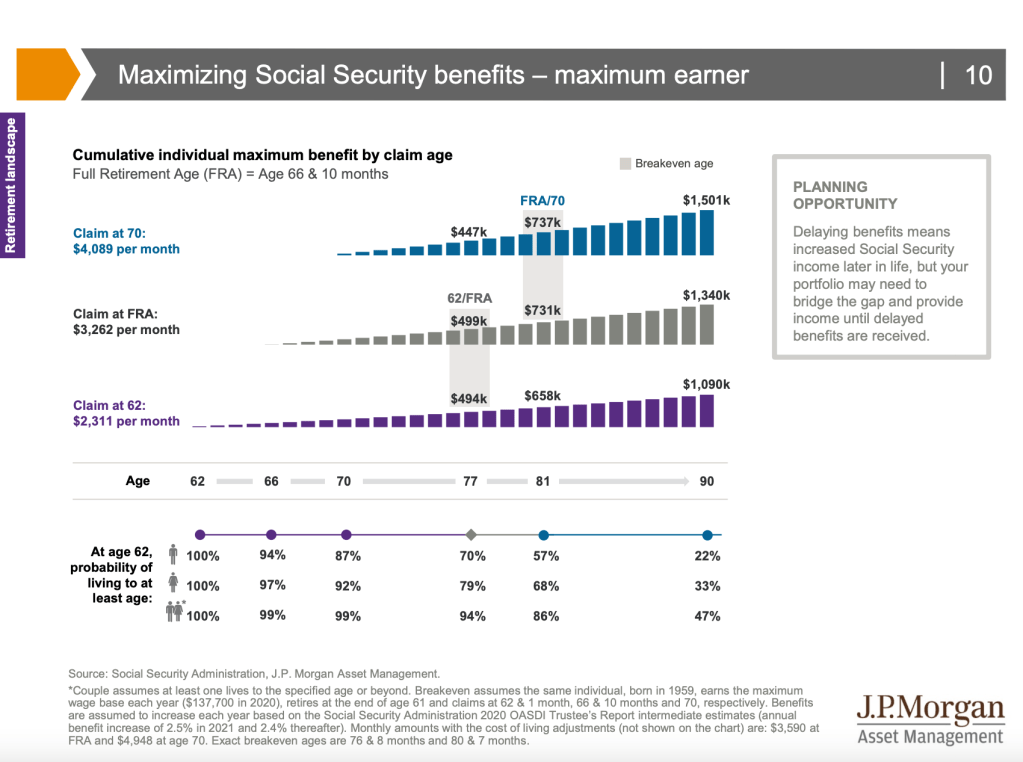

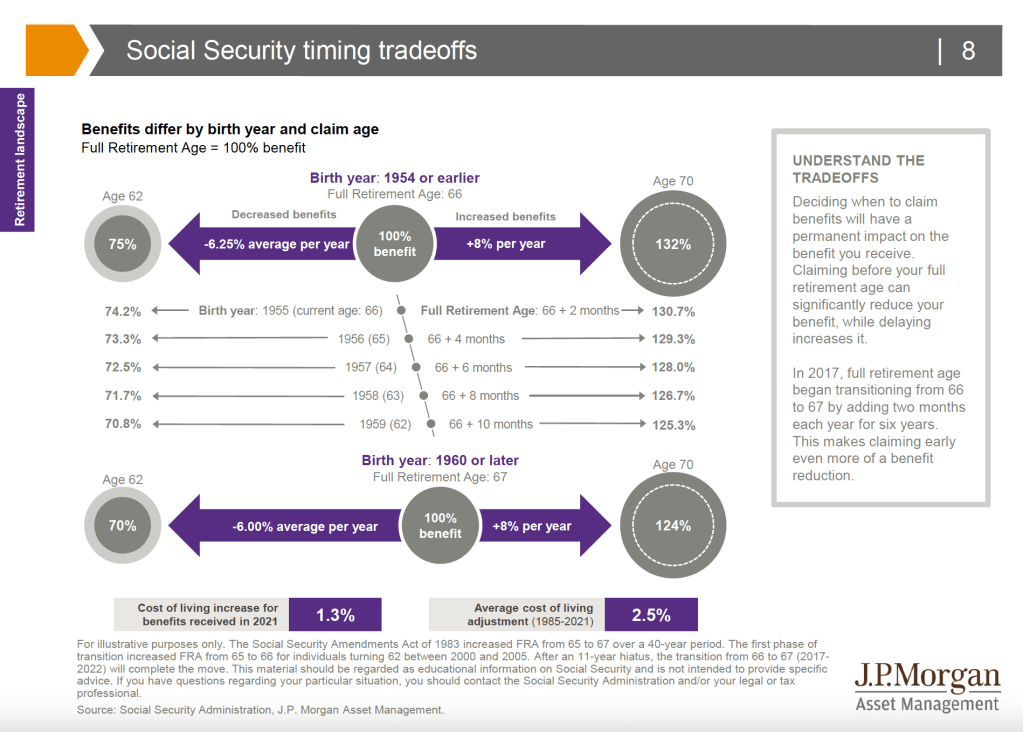

Surprisingly few Americans understand the benefits and trade-offs related to claiming Social Security at various ages. The top graphic illustrates these tradeoffs for people whose Full Retirement Age (FRA) is 66. Delaying benefits results in a much higher benefit amount: Waiting to age 70 results in 32% more in a benefit check than taking benefits at FRA. Likewise, taking benefits early will lower the benefit amount. At age 62, beneficiaries would have received only 75% of what they would get if they waited until age 66. FRA for individuals turning 62 in 2021 is 66 and 10 months, and FRA will continue to move 2 more months in 2022, when it will reach and remain at age 67. The Social Security Amendments Act of 1983 increased FRA from 65 to 67 over a 40-year period. The first phase of transition increased FRA from 65 to 66 for individuals turning 62 between 2000 and 2005. After an 11-year hiatus, the transition from 66 to 67 will complete the move.

The bottom graphic shows the tradeoffs for younger individuals, who will be penalized for early claiming to a greater degree. The percentages shown are “real” amounts – cost-of-living adjustments (COLA) will be added on top, providing an even greater difference between the actual dollar benefits one would receive. The average annual COLA for the past 36 years has been 2.5%.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Most likely, you’ve heard what’s brewing in Washington, D.C., called by one of these names.

The Build Back Better Act.

Or the $3.5 trillion budget reconciliation bill. Or the Jobs and Economic Recovery Plan for Working Families. (1)

Regardless of what name you’ve heard, one fact is clear: It is likely to be months before any action is taken.

When bills are being worked on—especially one that’s this size—it’s a good time to take a quick Civics refresher. Right now, the bill is “in committee” with both the House of Representatives and the Senate. The committees are filling in the policy details and the exact financial figures, which can be a long process. (2)

It will then be up to the House and Senate to vote on an identical version of a final bill—if both can agree to a final version. (2)

Right now, it would be hasty to make any portfolio changes based on what’s being discussed and debated. An ambitious investor would have to guess at what policies will be in the final bill, estimate the financial impact, and determine what portfolio changes should be made. That’s a tall order.

So as difficult as it may be, the best approach is to wait-and-see.

This article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and financial professionals before modifying your tax strategy.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The news keeps getting better for Social Security recipients.

It’s now projected that benefits will increase 6.1% in 2022, up from the 4.7% forecast just two months ago. That would be the most significant increase since 1983. (1,2)

It’s all about inflation. Social Security cost of living adjustments (COLA) are based on the consumer price index, which rose 5.4% in June — its largest 12-month increase since 2008. The official announcement is expected in October and, once it’s confirmed, the revised payment will go into effect in January 2022. (3)

More than 65 million Americans receive Social Security, and the annual cost of living adjustments are designed to help recipients manage higher costs. At the start of 2021, recipients saw a 1.3% increase. (4)

The average monthly benefit is $1,544 for retired workers. So a 6.1% increase amounts to $94 more a month. That might not be quite enough for a car payment, but it’s double the 3% raise being given to U.S. workers in 2021. (4,5)

Social Security can be confusing. One survey found only 6% of Americans know all the factors that determine the maximum benefits someone can receive. If you have any questions, please reach out. We have a number of resources at our fingertips that you may find helpful. (6)

This decision tree is designed to help individuals think through some of the factors related to when to take Social Security benefits. Working, having other sources of income, expected longevity, preserving a portfolio and trying to maximize benefits are important considerations. The possibility of benefits for family is not included; individuals should contact the Social Security Administration if they have questions about their personal situation.

The forecasts for Social Security benefits are based on assumptions, subject to revision without notice, and may not materialize.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

As many workers traded in the office for remote work, data security has been a focus for the public and private sectors. Between robocalls pitching low-cost health insurance, pretending to be the I.R.S., or offering “work from home” opportunities, the pandemic has seen scammers getting more creative than they’ve ever been. (1)

Tax time is prime time for identity thieves.

They would love to get their hands on your 1040 form, and they would also love to claim a phony refund using your personal information. You may realize you’ve been the victim of tax fraud if you can’t e-file your tax return because of a duplicate Social Security number or if you receive a notice from the I.R.S. that talks about owing taxes for a year you haven’t filed. (2)

Just make sure when you e-file that you use a secure Internet connection. When you e-file, you aren’t putting your Social Security number, address, and income information through the mail. You aren’t leaving Form 1040 on your desk at home (or work) while you get up and get some coffee or go out for a walk. If somehow you just can’t bring yourself to e-file, then think about sending your returns via Certified Mail. Those rough drafts of your returns where you ran the numbers and checked your work? Shred them.

The I.R.S. doesn’t use unsolicited emails to request information from taxpayers. If you get an email claiming to be from the I.R.S. asking for your personal or financial information, report it to your email provider as spam. (2)

Use secure Wi-Fi.

Avoid “coffee housing” your personal information away – never risk disclosing financial information over a public Wi-Fi network. (Broadband is susceptible, too.) It takes little sophistication to do this – just a little freeware.

Sure, a public Wi-Fi network at an airport or coffee house is password-protected – but if the password is posted on a wall or readily disclosed, how protected is it? A favorite hacker trick is to sit idly at a coffee house, library, or airport and set up a Wi-Fi hotspot with a name similar to the legitimate one. Inevitably, people will fall for the ruse, log on, and get hacked.

Look for the “https” & the padlock icon when you visit a website.

Not just http, https. When you see that added “s” at the start of the website address, you are looking at a website with active SSL encryption, and you want that. A padlock icon in the address bar confirms an active SSL connection. For really solid security when you browse, you could opt for a VPN (virtual private network) service which encrypts 100% of your browsing traffic. (3)

However, be especially careful when clicking on any links that you receive from an unknown sender. Many criminals have caught up, and use sites that seem valid by using the “https” prefix. Look to see what the email is asking for (for example, demanding payment), and verify this by sending a separate email or calling the supposed contact to verify the validity of the email. Look for any misspelled words or incorrect links in the email. If you’re more technically savvy, you can look at the original version of the email to see if it actually originated from somewhere else. (3)

Check your credit report.

You may have been the victim of identity theft or fraud, and not even realize it, until it shows up on your credit reports. Thanks to the Fair Credit Reporting Act (FCRA) you are entitled to one free credit report per year from each of the big three agencies: Experian, TransUnion, and Equifax. This year, because of the increased issues with identity theft and fraud during COVID-19, these three agencies are also allowing weekly credit checks from now until April 2021. Checking your credit report weekly will not affect your ability to order your free annual credit report.4,5

Don’t talk to strangers.

Broadly speaking, that is very good advice in this era of identity theft. If you get a call or email from someone you don’t recognize – it could tell you that you’ve won a prize; it could claim to be someone from the county clerk’s office, a pension fund, or a public utility – be skeptical. Financially, you could be doing yourself a great favor.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Year after year, certain taxpayers resort to schemes in an effort to put one over on the Internal Revenue Service (I.R.S.). These cons occur year-round, not just during tax season. In response to their frequency, the I.R.S. has listed the 12 biggest offenses – scams that you should recognize, schemes that warrant penalties and/or punishment.

1. Phishing

If you get an unsolicited email claiming to be from the I.R.S., it is a scam. The I.R.S. never reaches out via email, regardless of the situation. If such an email lands in your inbox, forward it to phishing@irs.gov. You should also be careful with sending personal information, including payroll or other financial information, via an email or website. (1,2)

2. Phone scams

Each year, criminals call taxpayers and allege that said taxpayers owe money to the I.R.S. The Treasury Inspector General for Tax Administration says that over the last five years, 12,000 victims have been identified, resulting in a cumulative loss of more than $63 million. Visual tricks can lend authenticity to the ruse: the caller ID may show a toll-free number. The caller may mention a phony I.R.S. employee badge number. New spins are constantly emerging, including threats of arrest, and even deportation. (1,2)

3. Identity theft

The I.R.S. warns that identity theft is a constant concern, but not just online. Thieves can steal your mail or rifle through your trash. While the I.R.S. has made headway in terms of identifying such scams when related to tax returns, and plays an active role in identifying lawbreakers, the best defense that remains is caution when your identity and information are concerned. (1,2)

4. Return preparer fraud

Almost 60% of American taxpayers use a professional tax preparer. Unfortunately, among the many honest professionals, there are also some con artists out there who aim to rip off personal information and grab phantom refunds, so be careful when making a selection. (1,2)

5. Fake charities

Some taxpayers claim that they are gathering funds for hurricane victims, an overseas relief effort, an outreach ministry, and so on. Be on the lookout for organizations that are using phony names to appear as legitimate charities. A specious charity may ask you for cash donations and/or your Social Security Number and banking information before offering a receipt. (1,2)

6. Inflated refund claims

In this scenario, the scammers do prepare and file 1040s, but they charge big fees up front or claim an exorbitant portion of your refund. The I.R.S. specifically warns against signing a blank return as well as preparers who charge based on the amount of your tax refund. (1,2)

7. Excessive claims for business credits

In their findings, the I.R.S. specifically notes abuses of the fuel tax credit and research credit. If you or your tax preparer claim these credits without meeting the correct requirements, you could be in for a nasty penalty. (1,2)

8. Falsely padding deductions on returns

Some taxpayers exaggerate or falsify deductions and expenses in pursuit of the Earned Income Tax Credit, the Child Tax Credit, and other federal tax perks. Resist the temptation to pad the numbers and avoid working with scammers who pressure you to do the same. (1,2)

9. Falsifying income to claim credits

Some credits, like the Earned Income Tax Credit, are reported by scammers claiming false income. You are responsible for what appears on your return, so a boosted income can lead to big penalties, interest, and back taxes. (1,2)

10. Frivolous tax arguments

There are seminar speakers and books claiming that federal taxes are illegal and unconstitutional and that Americans only have an implied obligation to pay them. These and other arguments crop up occasionally when people owe back taxes, and at present, they carry little weight in the courts and before the I.R.S. There’s also a $5,000 penalty for filing a frivolous tax return, so these fantasies are best ignored. (1,2)

11. Abusive tax shelters

If it sounds too good to be true, it usually is, and that’s especially true of complicated tax avoidance schemes, which attempt to hide assets through a web of pass-through companies. The I.R.S. suggests that a second opinion from another financial professional might help you avoid making a big mistake. (1,2)

12. Offshore tax avoidance

Not all taxpayers adequately report offshore income, and if you don’t, you are a lawbreaker, according to the I.R.S. You could be prosecuted or contend with fines and penalties. (1,2)

Watch out for these ploys – ultimately, you are the first defense against a scam that could cause you to run afoul of tax law.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Lafayette, US – December 27, 2016: GameStop Strip Mall Location. GameStop is a Video Game and Electronics Retailer IV

As a long term investors we do not spend too much time on market anomalies, let alone individual stocks that fall outside long-term asset allocation principles, but this seems to have taken over the headlines last week. Rarely do stock market quirks become mainstream news; in this case, it carried over to market sentiment to some extent and definitely raised trading volumes.

What Happened?

GameStop is a video game retailer, and an example of a stock that has been a favorite recent target of short-sellers. This is largely because of skepticism about the company’s long-term business fundamentals (the stock was selling at under $5/share). Like many brick-and-mortar based retailers, Covid has accelerated the movement to online commerce, and has punished these types of companies—putting their future in greater doubt. Taking a step back, selling a stock short is practically the most negative view an investor can take, since it’s the polar opposite of owning it. It involves borrowing the shares from another party, and selling them in advance, so in essence hoping for a sharp downturn to re-buy (‘cover’) the position later at a lower price. So it’s like buy low, sell high, excepted executed in reverse. Investors like hedge funds (often in long/short or market neutral strategies) take short positions in companies for reasons like weak financial prospects, over-optimistic expectations, or even potential fraud. Naturally, this can be risky, especially if extra leverage is used. Such investors may even convey bad news about a company to weaken its stock price, which sounds odd at first thought, but really is not that much different than Warren Buffet talking about his admiration for Coca-Cola—hoping the stock price goes up.

Based on reports, it seems a group of retail investors (presumably video game fans, who may have taken the GameStop assault personally) decided to take a stand against ‘greedy’ hedge funds and punish them for taking advantage of these troubled companies. In that sense, this has been described as a morality play (and/or these folks have given hedge funds too much credit, as fund failures are far more common than successes, but not as publicized). They’ve gathered support on Reddit, an online news aggregator and discussion site, as well as Twitter and other forums. By buying large amounts of the stock in aggregate, as well as that of a few other market short targets, like BlackBerry, AMC, and Bed Bath & Beyond, the group hoped to create a ‘short squeeze’. This happens when demand for owning long positions turns the tables on and overwhelms short position holders, pushing prices sharply higher, and creating huge losses for the shorts. Short squeezes can result in dramatic market movements, but have been a common practice for centuries, and often involving well-known investors. Similar to past cases, the result this time has been a sharp increase in volatility and quick and extreme price jumps for several of these companies. It also creates a feedback loop where the more (unjustifiably) expensive a stock gets, the greater the interest and potential profit in shorting it—if the shorts can hold on long enough, suffering losses in the meantime. Shorting is a risky bet, since a stock can fall to a limit of $0, but losses are theoretically unlimited (the stock price can grow to the sky, and the shorting party has to return the borrowed shares at some point, regardless of price).

In addition, this has been described as the mobilization of a populist effort to ‘re-democratize’ Wall Street. While this sounds dramatic, the backdrop is favorable to something like this happening. With brokerages offering easy-to-use platforms and commission-free trades, and some investors with a lot of free time on their hands due to Covid. This may have turned some trading sites into a ‘gaming’ interface of their own, rather than a vehicle to allocate investments for conventional reasons. It’s been suggested that such activity emerging may be signs of a broader bullishness in equity markets without fundamental basis, but in reality these events have occurred before over the years as one-offs rather than part of larger trends. (It happened with trading in ‘volatility’ strategies a few years ago and famously with silver in 1980.) This type of event is naturally easier with smaller, cheap companies, than large ones with strong mainstream demand. AMC has already taken advantage of the new ‘popularity’ in its stock by issuing more equity.

Will the Fed or SEC Impose Additional Regulations?

There have been calls for the Fed to raise Reg T margin requirements to stem this speculative behavior, at least via leverage, but brokerage firms have put on their own limits in some cases. (Bans on GameStop and other stocks have already been implemented by Robinhood, a favored broker for small investors, resulting in its own backlash from those opposing restrictions. A credit crunch on their part seemed to be partially behind it.) Unless this behavior becomes much more widespread and systematic, affecting overall U.S. financial stability, this is out of the Fed’s mandate. The SEC is investigating under the premise that this could be considered organized stock manipulation (through the online messages), along the same lines as a classic ‘pump and dump’ scheme. Insider trading has also been mentioned, but that seems more of a longshot, unless actual company insider information was shared and used. Time will tell whether a formal criminal case of any kind occurs.

This brings up a variety of potential issues, though, including how to regulate (or not regulate) this type of market activity. Many retail investors seem to see this as an ‘us versus them’ moment. On a deeper level, what is considered a fair market? Should smaller investors be protected from themselves? Or, should they be allowed to take the same risks as institutions? Who gets the blame if this turns out badly? How much leeway to give securities markets has been a long-standing question for much of the past century and prior. More regulation tends to pop up if things end badly, which of course they could here, if small investors end up losing their shirts. There is talk again of regulating the shorting of stocks, but the counterargument is that short sellers play an important economic role in efficient market price discovery and keeping supply/demand conditions in balance. Removing these bearish folks could create even more unpredictable stock price behavior, and infuse a tilt toward perpetual bullishness. Of course, this could have its own set of eventual problems.

The 3 Legs of Successful Long Term Investing

During times of market volatility it is important as long term investors to remember the three legs of successful investing:

Each year naturally brings more surprises than certainties, so outlooks and predictions of any kind quickly become futile. (We’ve already experienced a dramatic and unusual first week of January.) At least at this point in time, noted are a few key issues to monitor as 2021 gets going:

Covid Pandemic

This is the one carryover from 2020 everyone would like to forget. Unfortunately, it remains the single most important issue for both global medical and economic health going into 2021. While acknowledging the loss and hardship for many over the past year, the pandemic has also led to many examples of resiliency. It has resulted in a relatively smooth transition into work-from-home environments for some, but has also caused immeasurable problems for vulnerable cyclical industries forced to close or operate at reduced capacity. The development of several effective vaccines has taken an open-ended economic disaster and turned it into one with a clearer end game, assuming their distribution and effectiveness across populations go as planned. Mid-2021 is the current estimate for higher levels of implementation across the broader population (a goal of near-herd immunity) and some semblance of a ‘back to normal.’ But so far, logistics have been slow for vaccine rollout, so the economic normalization process seem more likely to be pushed back than bumped up, but the situation remains fluid. (Many are watching the rollout process in Israel, which has handled logistics very quickly and already inoculated nearly a quarter of their population, for clues.) The discovery of a new strain of Covid adds additional uncertainty to the mix, with hopes from health professionals that current vaccine technology won’t be derailed by this or further virus mutations.

Presidential Actions

The election of Joe Biden has led to assumed better consistency of behavior in the executive branch, but has also moved policy several ticks toward the left. Relative to others in the Democratic party, though, Biden is considered a ‘centrist’ and finder of common ground. In the best case, this may result in legislation backed by both sides of the aisle. However, the January 6th riot at the U.S. Capitol is an important reminder of how divided the nation remains, which could challenge the effort of national reconciliation. Some tempering of rhetoric and actions could be seen in the areas of tariffs/trade and executive orders, where the President has broader unilateral authority.

Senate

The two U.S. Senate runoff elections in Georgia on Jan. 5 were as closely-watched as any in recent years. While Republicans were expected to retain the seats, pollsters ended up with egg on their faces again, as both Democratic candidates won by narrow margins. This puts the Senate at 50-50, for only the fourth time in history. (Officially, the Democratic 50 includes two independent Senators, one of which is Bernie Sanders, who caucuses with the Democrats.) This equal split puts the deciding vote into the hands of incoming Vice President-Elect Kamala Harris, which is significant. While early descriptions of this result were as a ‘blue wave,’ many pundits have downgraded the impact to more like a ‘blue ripple’ in reality. This Democratic majority, albeit by narrower margins, could well result in further stimulus (early in 2021) and movement on infrastructure (which both parties actually agree on in principle, despite differing details—mostly in the green energy area). This could also include tightening up ACA/Obamacare, as well as procedural changes like altering the filibuster rule. Importantly, the majority gives Biden a smoother road for Senate-required approval of certain Presidential nominations. At the same time, the slim margin, and reduced Democratic majority in the House after the 2020 election, makes more extreme initiatives in health care (as in a full ‘Medicare for All’), the environment, tax law, etc. a bit more difficult to push through.

Economic Growth

The recovery in the economy continues to be almost completely dependent on the course of the pandemic and its abatement, driving estimates in both directions in recent months, along with unpredictable virus case counts. The expected -3% to -5% decline in U.S. GDP growth in 2020 is predicted to reverse to a potential mid-single digit gain in 2021 (give or take a few percent). Despite the initial trepidation about the Georgia race, the expected additional stimulus to be rolled out by a Democratic administration and Congress would be sure to have a positive effect on business and consumer spending in 2021-22, leading to even stronger GDP growth than with the late 2020 stimulus alone. (This is despite concerns of the budget deficit and high debt load down the road.) The recovery growth rate could be roughly double long-term trend growth of 2.0-2.5%, but relies on the mid-year majority vaccination timeline. With the pandemic-led recession marking the end of the last (and historically-long) business cycle, a new cycle is beginning anew. This is expected to lead to recovered corporate earnings growth in coming years—the critical long-term driver of equity returns. While some bearish observers see financial markets as looking too optimistic on 2021, based on higher price multiples, more bullish watchers see the pandemic recovery potentially more akin to the years after World War II, which benefited from a liftoff from stagnant production and pent-up consumer demand. In fact, some have gone as far as to label the coming decade a potential new ‘Roaring Twenties.’ (Interestingly, the original ‘Roaring 1920’s’ came after the 1918 influenza pandemic.)

Interest Rates

As they’ve stated directly, the Federal Reserve is committed to keeping rates low through the pandemic and for a while beyond. Some feared rates might be taken into negative territory, as in Europe, but that appears increasingly less likely due to logistical reasons, and far more pushback against it in the U.S. Long rates are also held lower by Fed purchases of treasuries and mortgages, but if inflation expectations were to rise, pressure could be felt on the long end of the yield curve first. The overall accommodative stance is likely to continue until recovery has taken hold, and until inflation picks up (over 2.0-2.5%) for a period of time. In the the first week of 2021, the 10-year treasury rose over 1.0% again as higher political odds for more stimulus (and a greater debt load) have raised the chances of higher economic growth and accompanying inflation. Overall, though, continued secular trends based on aging demographics and inconsistent productivity growth point to a consensus view that interest rates overall could stay relatively low for some time.

Financial Stability

This is an area not often discussed, due to so much focus on the short-term. What determines stability? For the most part, it’s an absence of excesses—that often include over-speculation in certain asset classes, taking on too much leverage, and higher destabilizing inflation. The 2007 housing market is a recent historical example of such an inflating and bursting bubble, but there are many historical examples. Due to well-known economist Hyman Minsky’s work in this area, the popping of such an unsustainable condition has been referred to as a ‘Minsky Moment.’ This is akin to the single snowflake that triggers a seemingly random avalanche, which is actually not random at all, but a condition that becomes increasingly likely over time as conditions build to more unstable levels. This may not be the case at the moment, being on the back end of a recession. But, over time, red flags such as exuberant sentiment without regard to any fundamentals, continued rising debt levels without regard for consequences, or the ignoring of any bad news that could derail a recovery, could all be signs of growing financial instability.

Investment Markets:

U.S. stocks. Investors have looked at the equity market with amazement, as stock prices moved almost straight back up after a -33% crash. Historically, though, such a result is not so unusual, with stocks often discounting the worst news and looking ahead toward a brighter future (even if a year or more away in reality). Valuations are a bit rich, based on expectations for 2021 revenue and earnings, with multiples appearing to look further into 2022 and even 2023 for fundamentals that justify current pricing. ‘Growth’ stocks, especially in technology and communications feature strong fundamentals, which have resulted in higher valuations, especially with today’s low interest rates. Are signs of the late 2020 rally in cyclical ‘value’ companies here to stay? Or, will a reemergence of challenges cause investors to again seek out the stability of ‘growth’? Uncertainty remains, but the coming year may offer more clues.

Antitrust issues and growth stocks. It’s been wondered whether current conditions are like the 2000 dot-com bubble, based on the extreme differential between ‘growth’ and ‘value’ sector performance. One difference, though, is that fundamentals (like profits) for today’s tech and communications companies are far more robust than at that time (in 2000, profits were often more hope than reality). In fact, high scores for the ‘quality’ factor have been a reason for the strong positive sentiment for that group. The pandemic’s challenges for smaller firms have caused even more consolidation of market share towards the biggest players. This begs the question: are these firms too dominant? There has been some increasing pressure for anti-trust legislation aimed at several mega-cap tech companies, but uncertainty about how that would look. There are some problematic legal issues. Does Congress really want to ‘punish’ the segment of the economy that has proven most resilient and efficient during the pandemic? Anti-trust typically requires a ‘damaged’ party, via price gouging or anti-competitive behavior. Do these services take unfair advantage of consumers (since they’re often free)? Do they suppress competition (or merely offer a better product)? These aren’t easily rectified.

Foreign stocks. Covid has challenged populations and businesses on a global level. While U.S. markets were seen as a safe haven in 2020 due to demand for leading technology/communications firms residing in the U.S., foreign markets offer more cyclicality, so an embedded ‘value’ bet of sorts. They also offer more relatively attractive valuations, less positive sentiment, and have been on the losing end of the U.S. vs. World equity performance trade for several years (the typical historical length for such dominance prior to a reversal). Emerging markets, in particular, have suffered high costs during the pandemic, and offer strong potential for recovery growth, due to a more modest starting point and more favorable demographics.

Bonds. An important relationship in fixed income is that total returns one should expect for coming years are mathematically tied to starting yields. This doesn’t bode well for those hoping for results like the past few decades, where rates were in a steady decline (from a peak in the early 1980’s) to today’s low levels. Credit spreads are also tighter than they were in much of 2020, with corporate improvement priced in. At the same time, while one shouldn’t necessarily expect great things from fixed income, the diversification element remains important should risk markets experience volatility. As a case in point, while interest rates were already considered low a year ago, and caution for bonds was everywhere, long-term U.S. treasuries earned 15%+ returns in 2020. Foreign bonds are an even more challenged environment, with a substantial percentage of debt offering negative yields, with price returns largely driven by currency markets.

Real estate.Last year was best described as one split between the ‘haves’ and ‘have-nots’ in the real property realm. Winners included newer niches of real estate markets that benefit from technological immersion, such as data centers and cell phone towers, and distribution centers that catered to online shopping. Valuations have risen for these assets, although fundamentals remain strong as they take a greater place in REIT indexes. Losing groups include the obvious, such as shopping malls, other retail, and travel/lodging. These represent the industries most heavily affected by lockdowns, although valuations have fallen to depressed levels, and could offer attractive sensitivity to further recovery. Office properties look to remain mixed, with some faring better than expected in the near-term, while the long-term strategic trend toward less office space/working from home has accelerated. Real estate in general has been supported by record-low financing rates, which is of course Fed-dependent.

It’s easy for investors to forget that the real estate universe is the world’s largest asset class, by overall size, and is extremely diverse.Owners of real estate assets are similarly quite diverse. On one end are residential homes and small commercial properties, which experienced contrasting results during the pandemic—strong house price increases bookended by retail locations having trouble making lease payments. So, the knee-jerk response is to cast commercial property overall in the bucket of ‘doomed’ asset. In some cases, this may be true, and has been for some time (notably in weaker strip malls in less desirable locations, and the like). However, as an institutional investment asset class, REITs generally focus their efforts on the largest, highest quality properties, in the most desirable locations (such as New York, London, etc.). While these are still sensitive to the business cycle, they’re often far less so (by design), and are far more liquid, than stand-alone properties profiled in news stories or owned in private partnerships. While there is some overlap due to similar inputs, high-quality REITs and generic Main Street real estate can provide varying results.

Commodities.Index composition varies, but energy futures contracts remain the most famous member of the asset class. Petroleum demand is more predictable in normal times, but fell off a cliff in 2020 as the pandemic put a damper on both industrial production and consumer mobility. Manufacturing has bounced back first, in China and other Asian nations, with lockdowns eased earlier. As the global economy recovers, prices for crude oil and industrial metals may also rise, as they often do when economies ‘reflate.’ Precious metals earned strong returns in 2020 due to their ‘safe haven’ tendencies, although that faded later in the year when investors sought riskier assets. A continued weaker U.S. dollar and any signs of higher inflation readings could serve to be two of the more important catalysts for commodities movement in 2021. Their most important role, however, is their lack of correlation to other asset classes in a portfolio—which can be hard to find elsewhere and often goes unappreciated.

Currencies.The U.S. dollar weakened by -7% in 2020 relative to a basket of developed market currencies, but was little changed versus emerging market currencies. As always, currency movements represent a ‘two-way street.’ This was a slight erosion in confidence in the dollar’s safe haven status, due to unprecedented amounts of fiscal and monetary stimulus, but also expectations in improved growth abroad—particularly the euro and U.K. pound as markets look past Brexit. Will this trend continue? Currency markets are fickle to say the least, but a cyclical rebound could continue to favor foreign currencies, which could translate to tailwinds for international stocks and bonds, which have lagged those of the U.S. in recent years.

These represent only a few items to watch. No doubt 2021 will bring its share of more (and hopefully positive) surprises.

For many, this year has been as complicated as learning a new dance. Did you start a new job or leave a job behind? That’s one step. Did you retire? There’s another step. Did you start a family? That’s practically a pirouette. If notable changes occurred in your personal or professional life, then you may want to review your finances before this year ends and 2021 begins. Proving that you have all of the right moves in 2020 might put you in a better position to tango with 2021.

Even if your 2020 has been relatively uneventful, the end of the year is still a good time to get cracking and see where you can manage your overall personal finances.

Keep in mind this post is for informational purposes only and is not a replacement for real-life advice. Please consult your tax, legal, and accounting professionals before modifying your tax strategy.

Do You Engage in Tax-Loss Harvesting?

That’s the practice of taking capital losses (selling securities worth less than what you first paid for them) to manage capital gains. You might want to consider this move, but it should be made with the guidance of a financial professional you trust. (1)

In fact, you could even take it a step further. Consider that up to $3,000 of capital losses in excess of capital gains can be deducted from ordinary income, and any remaining capital losses above that amount can be carried forward to offset capital gains in upcoming years. (1)

Do you want to itemize deductions?

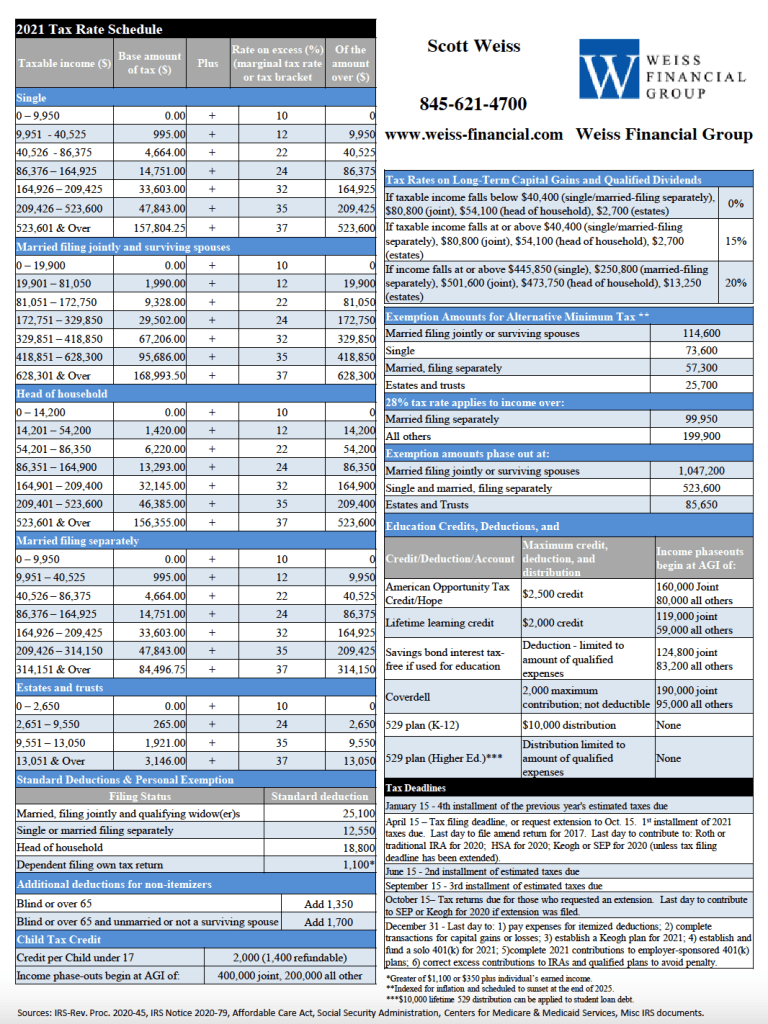

You may just want to take the standard deduction for the 2020 tax year, which has risen to $12,400 for single filers and $24,800 for joint. If you do think it might be better for you to itemize, now would be a good time to get the receipts and assorted paperwork together. (2,3)

Could You Ramp up Your Retirement Plan Contributions?

Contribution to these retirement plans may lower your yearly gross income. If you lower your gross income enough, you might be able to qualify for other tax credits or breaks available to those under certain income limits. (4)

Are You Thinking of Gifting?

How about donating to a qualified charity or non-profit organization before 2020 ends? Your gift may qualify as a tax deduction. For some gifts, you may be required to itemize deductions using Schedule A. (4)

Review a Portion of Your Estate Strategy

Specifically, take a look at your beneficiary designations. If you haven’t reviewed them for some time, double-check to see that these assets are structured to go where you want them to go, should you pass away. Lastly, look at your will to see that it remains valid and up-to-date.

Check on the Amount You Have Withheld

If you discover that you have withheld too little on your W-4 form so far, you may need to adjust your withholding before the year ends.

What Can You do Before Ringing in the New Year?

New Year’s Eve may put you in a dancing move, eager to say goodbye to the old year and welcome 2021. Before you put on your dancing shoes, consider speaking with a financial or tax professional. Do it now, rather than in February or March. Little year-end moves might help you improve your short-term and long-term financial situation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

On October 26, the Treasury Department released the 2021 adjusted figures for retirement account savings. Although these adjustments won’t bring any major changes, there are some minor elements to note.

401(k)s

The salary deferral amount for 401(k)s remains the same at $19,500, while the catch-up amount of $6,500 also remains unchanged. However, the overall limit for these plans will increase from $57,000 to $58,000 in 2021. (1)

Individual Retirement Accounts (IRA)

The limit on annual contributions remains at $6,000 for 2021, and the catch-up contribution limit is also unchanged at $1,000. (2)

Roth IRAs

Roth IRA account holders will experience some slightly beneficial changes. In 2021, the Adjusted Gross Income (AGI) phase-out range will be $198,000 to $208,000 for couples filing jointly. This will be an increase from the 2020 range of $196,000 to $206,000. For those who file as single or as head of household, the income phase-out range has also increased. The new range for 2021 will be $125,000 to $140,000, up from the current range of $124,000 to $139,000. (3)

Although these modest increases won’t impact many, it’s natural to have questions anytime the financial landscape changes. If you’re curious about any of the above, speak to your financial or tax professional for more information.

RETIREMENT PLANS (Annual Contribution Limits)

2021

2020

2019

401(k), 403(b), most 457 plans • 50+ Catch-up Contribution

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The impact of a potential new President on stock market returns is always a key question in the weeks prior to a general election. It’s important to keep in mind that, despite frequent worries around this time of year, and that financial markets may react in the shorter-term term to poll results and election outcomes (especially surprises), the longer-term effects of any administration’s policies appear to be disconnected from financial market results. Instead, stocks especially tend to follow earnings, which follow economic growth trends. Nevertheless, there are always policy distinctions that could affect various industries to some extent.

In contrast to election season norms in prior decades, polarization between the two parties has become more pronounced, with more extreme positions on both sides forcing candidates away from traditional ‘centrist’ policy often adopted during general election campaigns. A Biden victory has the potential of moving policy toward a more progressive stance, although this is not as simple of a story as in past years, with the current administration having taken a variety of unconventional stances in its own right.

The potential retaking of the Senate by Democrats, in addition to their already holding power in the House, would heighten the risk of more progressive policies being voted in—with minimal opposition. On the other hand, Republicans successfully retaining the Senate would continue to act as an effective counterbalance against legislation from the House, potentially resulting in a policy log jam for the next four years. (Some see this as a best-case scenario, although doing little to alleviate the high current levels of political disagreement.)

The following represent a few areas that could be most impacted by a new Democratic administration, through either new legislation, reversals of prior policies, or no change:

Taxes

It is assumed that the corporate and personal tax cuts put into place in the current regime could be reversed—partially or fully—towards prior levels. Personal income tax policy rhetoric during the campaign has been aimed at the ultra-wealthy, but with high budget deficits and an unprecedented level of fiscal debt, higher tax rates for even middle-income Americans have been feared. This includes higher capital gains tax rates, seen as benefitting the wealthy the most, as they own the majority of financial assets. ‘Wealth taxes’ based on assets are out there as a wildcard as well (although targeted at billionaires). Even if corporate rates do not return to prior max levels of 35%, they are likely not to remain at 21%, either. Most directly, higher tax rates for companies directly erode multi-year earnings projections, which could result in lower stock valuation assessments.

Environment

This multi-faceted policy area includes not only ‘green’ legislation (likely to be promoted by a Biden administration), but also important carryover effects related to the energy industry broadly. It would likely be unfavorable for traditional petroleum- and coal-based energy production (and emissions), including limitations for drilling, and increased regulation of impacts. Conversely, alternative energy sources would likely be promoted—including wind and solar—as well as the potential taxation of carbon emissions.

U.S.-China Relations and Trade

This is a more challenging policy point, as both parties have adopted a hard line on China—for a variety of different reasons. The current administration has taken a more confrontational approach. This has been unique relative to prior regimes, which, at least at the surface, had attempted to avoid outright hostile language and direct economic sanctions. While the two parties agree in principle for a tougher stance, Republicans have focused this effort on corporate intellectual property, while Democrats have also included human rights concerns; specifically, based on the treatment of several ethnic and religious minority groups within the country. This remains a wildcard to some degree, but the majority of Americans and politicians now favor a tougher stance toward China—a rare point of policy agreement.

Antitrust Legislation

This wouldn’t normally surface as a key policy platform, but the rise of several technology behemoths has raised questions over the competitive environment and growing economic power of these firms. In prior decades, pro-business conservative politicians have been more reluctant to attack oligopolistic entities, while populist/progressive movements had been responsible for breaking up dominant ‘Robber Baron’ firms—such as Rockefeller’s Standard Oil in the early 1900’s. In recent years, though, the more progressively-minded tech giants have been supportive of the Democratic agenda and drawing the ire of Republicans—creating a role reversal. The pressure on these firms may continue to some degree, depending on who’s in charge. Some of this oligopolistic power is due to the structures of the industries. They’ve remained among the most fundamentally solid from a financial standpoint during the pandemic, which has rewarded investors. Of course, many small businesses have not fared nearly as well, fanning the flames of resentment.

Workers

Republican policies over the years have generally been focused on letting ‘laissez faire’ (free market) forces determine market competition and pricing dynamics—favored by many mainstream economists. Biden policies would likely offer more worker-friendly populist concessions, such as a higher minimum wage, better health coverage, paid leave, student loan relief, etc. On one hand, additional benefits and pay cut into company profit margins. On the other hand, more money in the pockets of consumers could be a catalyst for broader personal spending and consumption growth broadly, which benefits the broader economy in its own way.

Healthcare

The formation of the Affordable Care Act (‘Obamacare’) was followed by an immediate battle for repeal by Republicans and expansion by Democrats. This fight is likely to continue, with any enhancements in coverage (like ‘Medicare For All’) or other changes aimed at high prescription drug prices (also favored by the current administration, despite potential impact on corporate profits). Some pharmaceutical firms have acted to pre-emptively curb pricing for some drugs in efforts to stem the criticism and potentially unfavorable legislation. These firms counter that such high prices act as the funding mechanism for continued research and development on new therapeutics, which many politicians have accepted. The convoluted health care system, though, continues to overwhelm attempts at reform, which has led to a lower financial market probability for radical change in the near-term.

Defense

In prior years, a strong defense budget and global projection of power has been a Republican party tenet. Lately, this has taken a bit of an opposite turn with conservatives moving more towards a stance of isolation, and progressives seeking to maintain greater globalism. This may be an area with little net change, absent geopolitical surprises (which can be counted on).

Immigration

This doesn’t seem like a market-related topic at first glance, but movement of people across borders affects demographics, which, in turn, affects the size of the labor force and productivity—and ultimately economic growth. This has been a divisive issue throughout America’s history, and each side currently has a mixed relationship with it. Generally, economists argue that a more lenient immigration policy provides a larger pool of workers, which results in not only higher production but also higher consumption. Companies have often silently been in favor of these less restrictive policies, which brings in a higher supply of workers, which lowers wages and boosts profits. On the other side, and often in conflict with other elements of the party, Democratic politicians have tended to have strong support from unionized U.S. workers, which often oppose globalism and foreign worker competition—in efforts to retain jobs and sustain higher wages domestically. Realistically, on net, there could be few extreme changes due to these continual conflicts.

Fiscal Policy

In decades of old, Republicans were seen as the fiscally spendthrift party, while Democrats were cast in debates as ‘tax-and-spend.’ But even prior to the Covid recession, these traditional labels were less applicable, with higher spending proposed on all sides. Due to economic woes from the pandemic likely carrying over into 2021, and perhaps 2022, as well as increasing acceptance of policies such as Modern Monetary Theory (MMT), it appears the accepted spending may continue regardless of the party in office. However, at the fringes, Democrats have proposed more direct relief to workers, and Republicans to small businesses, in keeping with other distinct policy preferences.

Monetary Policy

This should be unaffected by politics, and largely has been over the years. Of course, there have been notable and theatrical exceptions, such as the Fed Chair being physically bullied at LBJ’s Texas ranch in the 1960’s, and the current President’s urging of low rates via social media. A Biden presidency could likely feature more restraint, and a conventional ‘hands off’ approach. However, the Fed could be increasingly impacted by the large Federal deficit and rising debt load, which affects both interest payment obligations as well as credit rating—which affect rates outside of the Fed’s control.

In short, by looking at individual industries, the outlook may not appear to change that much, aside from policy preferences one way or another. The key differences relate to tax policy, the broader regulatory environment, and fiscal spending policies.

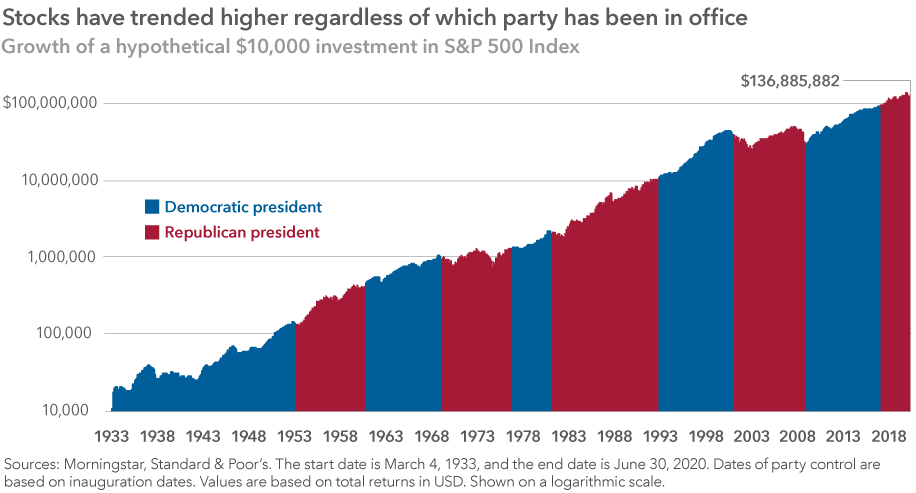

It’s important to remember that an elected President has very little effect on market results, historically. In fact, some of the stronger periods of market performance have been under Democratic administrations, contrary to popular assumption. (1)

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

This guide walks through a simple framework to help you think clearly about retirement—from defining what matters most to understanding how your financial pieces fit together.

If you’re looking for help with retirement planning or investment management, you can learn more about how I work with clients at Weiss Financial Group.

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.

Scott Weiss, CFP®

RICP®, CRPC®, AAMS®, AWMA®, APMA®, CMFC®

ADDRESS:

704 Route 6

Mahopac, NY 10541

PHONE:

845-621-4700

Want more insights like this?

Get thoughtful, planning-focused insights delivered occasionally.

No noise. Just practical, planning-focused perspective. Unsubscribe anytime.