A well-structured plan can provide clarity in a way predictions often cannot.

It helps you:

Understand what’s sustainable over time

See how different scenarios may affect your decisions

Make adjustments without starting over

Make more consistent decisions during uncertain markets

Most importantly, it shifts your focus away from trying to control the future…

And toward building something that works within it.

Bringing It Together

The future will always be uncertain.

What can change is how you approach it.

When decisions are built around predictions, it’s easy to feel like you’re waiting—for better markets, better timing, or more clarity that may never fully arrive. That uncertainty can quietly shape decisions in ways that don’t always serve you over time.

A good plan creates a different experience.

It can give your decisions a foundation. It connects your income, investments, and spending into something designed to work together—even as conditions shift.

You’re no longer trying to guess what comes next.

You’re making thoughtful decisions within a structure designed to adapt.

Over time, that shift can be meaningful.

Not because it removes uncertainty—but because it allows you to move forward without being controlled by it.

Final Thought

If you’re approaching retirement and want help thinking through this, you can schedule a brief, complimentary call.

No pressure. Just a chance to see if it makes sense to talk further.

At some point, many people wonder whether they should get a second opinion on their financial plan.

Not because something is obviously wrong.

But because retirement decisions become more complex over time—and it’s not always easy to know how well everything is aligned.

A second opinion isn’t about replacing what you have. It’s about gaining clarity.

When It’s Worth Taking a Closer Look

There are a few situations where getting another perspective can be especially helpful.

1. You’re approaching retirement

As you move closer to retirement, the focus shifts.

It’s no longer just about saving and investing. It becomes about how those savings are structured to support income, and how different decisions fit together.

If you haven’t revisited your plan recently, this is often a useful time to revisit it.

One of the things I’ve noticed over the years is that many people feel confident about their retirement savings, but less clear about their retirement plan.

Their accounts may be in good shape, and they’ve done a good job saving. But when you start talking through how everything fits together—income, spending, investments, and the decisions that come with retirement—it may be less clearly defined.

When people think about retirement planning, they often picture numbers—account balances, rates of return, withdrawal percentages.

Those things matter. But they’re only part of the picture.

A thoughtful retirement plan isn’t just a set of projections. It’s a way of organizing decisions so that decisions are aligned.

It Starts With Your Life, Not Your Portfolio

A plan doesn’t begin with investments.

It begins with how you want to live.

That includes questions like:

When do you want to retire?

What does a typical year look like?

How do you want to spend your time and money?

Without that context, the numbers don’t mean much.

If you’re thinking through the timing of retirement itself, you can read more here:When Should You Retire?

Income Is the Foundation

In retirement, your plan revolves around income.

Not just how much you have, but how that translates into supporting your spending needs.

A thoughtful plan helps address:

Where will your income come from?

How will that change over time?

How do different sources (Social Security, investments, etc.) fit together?

It’s less about maximizing returns and more about creating a structured approach to generating income over time.

The passing of a loved one irrevocably alters family life. After a death, there is so much to attend to; it is better to do it sooner rather than later. Here, then, is a list of what commonly needs to be looked after.

Request copies of the death certificate.

Depending on where you live, you have two or three places to turn to for this document. You can phone, email, or personally visit the office of the county recorder (or county clerk, as the term may be). Alternately, you can contact your state’s vital records department (sometimes called the state registrar or department of health); it may take a little longer to get the document this way. In addition, some large and mid-sized cities maintain their own registrars of births and deaths.

Call advisors, executors, & business partners as applicable.

The deceased’s lawyer and CPA should be quickly notified along with any business partners and the executor of his or her estate. You must have a say in the decision-making. The tasks of protecting family assets, carrying out your loved one’s bequests, and determining the next steps for a business will follow.

Call your loved one’s current or former employer(s).

Notify them, even if your loved one left the workforce years ago, as retirement savings or pension payments may be involved. As the conversation develops, it is perfectly appropriate to ask about pertinent financial matters – say, 401(k) or 403(b) savings that will be inherited by a beneficiary or what will happen to unused vacation time and/or unpaid bonuses.

Funds amassed in a qualified retirement plan sponsored by an employer (or an IRA, for that matter) commonly go to the primary beneficiary who has been named on the most recent beneficiary form filled out by the account owner. That sounds simple enough – but certain rules and regulations can make things complicated. (1)

As a general rule, if the late 401(k) or 403(b) account owner was your spouse, then you are the presumed beneficiary of the 401(k) or 403(b) assets. Under the Employee Retirement Income Security Act (ERISA), workplace retirement plans are directed to abide by this guideline. If someone else has been named as the primary beneficiary of the account, with your consent, then the assets will go to that person. (2)

If the late 401(k) or 403(b) account owner was single, the assets in the account will go to whomever is designated as the primary beneficiary. The beneficiary designation will override other estate planning documents. (3)

To arrange and confirm the transfer or distribution of such assets, the beneficiary form must be found. If you can’t locate it, the employer and/or the financial firm overseeing the retirement plan should provide access to a copy. The financial firm should ask you to supply:

A certified copy of the account owner’s death certificate

A notarized affidavit of domicile (a document certifying his or her place of residence at the time of death)

If you have been widowed, call Social Security.

If you already receive benefits, you may now be eligible for greater benefits. (4)

If your spouse received Social Security and you did not, you may now qualify for survivor benefits – and you should let Social Security know as soon as possible, as these benefits may be paid out relative to your application date rather than the date of your loved one’s death. (4)

If this is the case, you may apply for survivor benefits by phone or by visiting a Social Security office. You will need to have some extensive paperwork on hand, specifically:

Proof of the death (death certificate, funeral home documentation)

Your late spouse’s Social Security number

His/her most recent W-2 forms or federal self-employment tax return

Your own Social Security number & birth certificate

Social Security numbers & birth certificates of any dependent children

Your marriage certificate, if you have been widowed

The name of your bank & the number of your bank account, for direct deposit purposes

If you have reached full retirement age, you will likely get 100% of the basic benefit amount that your late spouse was receiving. If you are in your sixties, but haven’t yet reached full retirement age, you may receive anywhere from 71% to 99% of that amount. If you have a child younger than 16, you will get 75% of your late spouse’s basic benefit amount and so will your child. (4,5)

Contact the insurance company.

Assuming your loved one had some form of life insurance, contact the policyholder services department of that insurer and confirm the steps for claiming the death benefit. A claim form will have to be filled out, signed, and presented to the insurance company (one for each named adult beneficiary of the policy), and a certified copy of the death certificate must also be sent. If the primary beneficiary of a policy is deceased, the contingent beneficiary can usually claim the death benefit with a claim form, plus the death certificates of the policy owner and the primary beneficiary. Some insurers simply have you submit a form reporting the death of the policyholder first, and then follow up by mailing you forms and instructions for the next steps. (6)

Death benefits are generally paid out within 30 to 60 days of a claim. Presumably, they will be paid out in a lump sum. Some insurers will let a beneficiary receive a payout as a stream of monthly income or in installments. (7)

It isn’t unusual for people to own multiple life insurance policies. The AARP, AAA, and myriad banks and non-profits market group life coverage to members/customers, and mortgage lenders and credit issuers offer forms of life insurance for borrowers. Tracking all this coverage down is the problem, and canceled checks and bank records don’t always provide ready clues. Not surprisingly, websites have appeared that will help you search for life insurance policies, and you may be able to locate policies with the help of your state insurance commissioner’s office. (8)

If the family member was a veteran, call the VA.

Your family may be entitled to funeral and burial benefits. In addition, the Veterans Administration offers Death Pensions and Aid & Attendance and Housebound Pensions to lower-income widows of deceased wartime veterans and their unmarried children. (9)

These pensions are needs based. To be eligible for the Death Pension, a widow or child’s “countable” income must fall below a certain yearly limit set by Congress. (A “child” as old as 22 may be eligible for the Death Pension.) The deceased veteran must not have received a dishonorable discharge, and they must have served 90 or more days of active duty, at least 1 day of it during wartime. If they entered active duty after September 7, 1980, then in most cases, 24 months or more of active duty service are necessary for a Death Pension to eventually be paid. The Aid & Attendance and Housebound Pensions provide some recurring income to pay for licensed home health aide or homemaker services. (9)

It is wise to contact a Veterans Services Officer before you file such a pension claim, as they can be a big help during the process. You can find a VSO through your state veterans’ affairs department or through the VFW, the Order of the Purple Heart, the American Legion, or the non-profit National Veterans Foundation. (9)

A final individual income tax return may be required for the deceased.

You or your tax professional should consult I.R.S. Publication 17 for more detail. Also, search for “Topic 356 – Decedents” on the I.R.S. website. Deductible expenses paid by the deceased before death can generally be claimed as deductions on such a return. (10)

If you have been widowed, consider the future.

In the coming days or weeks, you should arrange a meeting to review your retirement planning strategy, and your will, beneficiary designations, and estate plan may also need to be updated. The passing of your spouse may necessitate a new executor for your own estate. Any durable powers of attorney may also need to be revised.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

A power of attorney (POA) is a legal instrument that delegates an individual’s legal authority to another person. If an individual is incapacitated, the POA assigns a trusted party to make decisions on his or her behalf.

There are nondurable, springing, and durable powers of attorney. A nondurable power of attorney often comes into play in real estate transactions, or when someone elects to delegate their financial affairs to an assignee during an extended absence. A springing power of attorney “springs” into effect when a specific event occurs (usually an illness or disability affecting an individual). A “durable” power of attorney allows an assignee, or agent, to act on behalf of a second party, or principal, even after the principal is not mentally competent or physically able to make decisions. Once a principal signs, or executes, a durable power of attorney, it may be used immediately, until it is either revoked by the principal or the principal dies. (1)

Keep in mind this article is for informational purposes only. It’s not a replacement for real-life advice. Make sure to consult your legal professional so you can better understand what type of powers of attorney is a best fit for your situation.

What the POA allows in financial terms. Financially, a Power of Attorney is a tremendously useful instrument. An agent can pay bills, write checks, make investment decisions, buy or sell real estate or other hard assets, sign contracts, file taxes, and even arrange the distribution of retirement benefits.

Advanced Healthcare Directives and Living Wills

Some illnesses can eventually rob people of the ability to articulate their wishes, and this is a major reason why people opt for a Health Care Power of Attorney (HCPOA) or a living will. There are differences between the two.

A Health Care Power of Attorney (also called a “healthcare proxy”) allows an agent to make medical decisions for a principal, should they become physically or mentally incapacitated. A living will gives an assignee similar powers of decision, but this advanced directive only applies when someone faces certain death. The assignee has the authority to carry out the wishes of the incapacitated party.

Would you like to learn more?

It may be time to meet with an attorney who specializes in these issues. You can find one with the help of an insurance or financial professional who has assisted families with legacy planning.

This checklist will help you determine what issues to consider when reviewing your estate plan.

Sources

AgingCare.com, August 23, 2021

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

One of the objectives of creating a household budget is that, as time moves on and the various household members advance in their careers, they are likely to make more money. Knowing where that money goes can help direct that money to not only meet your day-to-day needs but also to potentially realize your financial goals. Rent payments may become mortgage payments, and socking away a few bucks into your savings each payday could change into an effective financial strategy involving various investment tools. (1)

Remember that investing involves risk, and the return and principal value of investments will fluctuate as market conditions change. Investment opportunities should take into consideration your goals, time horizon, and risk tolerance. When sold, investments may be worth more or less than their original cost. Past performance does not guarantee future results.

The Back of an Envelope or a Spreadsheet App.

Traditionally, a household budget could be worked out “on the back of an envelope.” Of course, this is still true, though you may have access to more bells and whistles than previous generations. Whether you prefer to work it out with pencil and paper or by computer, the main rule is to create and stick to the budget.

Easy Come, Easy Go.

Start by taking note of your income. Some Americans have more than one income source, either through a second gig or even a hobby turned small business. You don’t have to be making money very long, though, to realize that it doesn’t always sit still in your checking account. Along with your income, tally up your expenditures: Housing costs (rent, utilities, etc.), groceries, student loan payments, transportation expenses, phone, and Internet, as well as entertainment. It adds up! (More like subtracts, actually.)

Make Adjustments

Ideally, the number at the bottom of this reckoning should be a positive number. This means that you’re living within your means and, while you may want to make that a larger number by adjusting your expenses, you’re at a good starting point.

Adjustments are probably overdue if you have a negative number; you’ll need to take a cold hard look at those expenses and think about can I live without (such as mountaineering lessons) and what isn’t going to give (the essentials: food and shelter).

Your other choice, of course, is to make more money. As you move on in your career, this will likely happen as you earn salary increases or build your business. Don’t forget, though, that life gets more expensive over time, as well. Rents and fees will rise as time goes on. Regular adjustments are a natural part of good budgetary maintenance.

Goals and Strategies

If you have money coming in that is not being gobbled up by line items on your budget, and you stick to it and keep it that way, you’re (literally) coming out ahead. Now’s the time to put that money to work toward goals and strategies. Goals can be small, like saving up for a vacation or upgrading an item in your home. Or they can be larger, like saving for a major expense.

Goals can work side-by-side with financial strategies, which tend to be “bigger picture” in scope. Financial strategies tend to be things like looking ahead to your retirement or investing in creating more income (so you can get back to mountain climbing). For these bigger strategies and the shorter-term goals, there is an advantage to seeking out a financial professional geared toward helping you get the most from your efforts.

There is No “One Way” to Budget.

There isn’t a single, one-size-fits-all solution for creating and maintaining a household budget. Financial professionals also know this and can help craft a strategy suited to your risk tolerance, goals, and financial situation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Many people plan their estates diligently, with input from legal, tax, and financial professionals. Others plan earnestly but make mistakes that can potentially affect both the transfer and destiny of family wealth. Here are some common and not-so-common errors to avoid.

1) Doing it All Yourself

While you could write your own will or create a will, it can be risky to do so. Sometimes simplicity has a price. Look at the example of Aretha Franklin. The “Queen of Soul’s” estate, valued at $80 million, may be divided under a handwritten or “holographic” will. Her wills were discovered among her personal effects. Provided that the will can be authenticated, it will be probated under Michigan law, but such unwitnessed documents are not necessarily legally binding. (1)

2) Failing to Update Your Will or Trust After a Life Event

Relatively few estate plans are reviewed over time. Any major life event should prompt you to review your will, trust, or other estate planning documents. So should a major life event that affects one of your beneficiaries.

3) Appointing a Co-Trustee

Trust administration is not for everyone. Some people lack the interest, the time, or the understanding it requires, and others balk at the responsibility and potential liability involved. A co-trustee also introduces the potential for conflict.

4) Being too Vague With Your Heirs About Your Estate Plan

While you may not want to explicitly reveal who will get what prior to your passing, your heirs should understand the purpose and intentions at the heart of your estate planning. If you want to distribute more of your wealth to one child than another, write a letter to be presented after your death that explains your reasoning. Make a list of which heirs will receive collectibles or heirlooms. If your family has some issues, this may go a long way toward reducing squabbles as well as the possibility of legal costs eating up some of this-or-that heir’s inheritance.

5) Leaving a Trust Unfunded (or Underfunded)

Through a simple, one-sentence title change, a married couple can fund a revocable trust with their primary residence. As an example, if a couple retitles their home from “Heather and Michael Smith, Joint Tenants with Rights of Survivorship” to “Heather and Michael Smith, Trustees of the Smith Revocable Trust dated (month)(day), (year).” They are free to retitle myriad other assets in the trust’s name. (1)

6) Ignoring a Caregiver With Ulterior Motives

Very few people consider this possibility when creating a will or trust, but it does happen. A caregiver harboring a hidden agenda may exploit a loved one to the point where they revise estate planning documents for the caregiver’s financial benefit.

The best estate plans are clear in their language, clear in their intentions, and updated as life events demand. They are overseen through the years with care and scrutiny, reflecting the magnitude of the transfer of significant wealth.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

When you reach age 70½, the Internal Revenue Service instructs you to start making withdrawals from your traditional IRA(s). These withdrawals are also called Required Minimum Distributions (RMDs). You will make them, annually, from now on. (1)

If you fail to take your annual RMD or take out less than the required amount, the I.R.S. will notice. You will not only owe income taxes on the amount not withdrawn, you will owe 50% more. (The 50% penalty can be waived if you can show the I.R.S. that the shortfall resulted from a “reasonable error” instead of negligence.) (1)

Many IRA owners have questions about the rules related to their initial RMDs, so let’s answer a few.

How does the I.R.S. define age 70½?

Its definition is pretty straightforward. If your 70th birthday occurs in the first half of a year, you turn 70½ within that calendar year. If your 70th birthday occurs in the second half of a year, you turn 70½ during the subsequent calendar year. (2)

Your initial RMD has to be taken by April 1 of the year after you turn 70½. All the RMDs you take in subsequent years must be taken by December 31 of each year. (1)

So, if you turned 70 during the first six months of 2020, then you will be 70½ by the end of 2020, and you must take your first RMD by April 1, 2021. If you turn 70 in the second half of 2020, then you will be 70½ in 2021, and you won’t need to take that initial RMD until April 1, 2022. (1)

Is waiting until April 1 of the following year to take my first RMD a bad idea?

The I.R.S. allows you three extra months to take your first RMD, but it isn’t necessarily doing you a favor. Your initial RMD is taxable in the year that it is taken. If you postpone it into the following year, then the taxable portions of both your first RMD and your second RMD must be reported as income on your federal tax return for that following year. (2)

An example: James and his wife Stephanie file jointly, and they earn $78,950 in 2019 (the upper limit of the 22% federal tax bracket). James turns 70½ in 2019, but he decides to put off his first RMD until April 1, 2020. Bad idea: this means that he will have to take two RMDs before 2020 ends. So, his taxable income jumps in 2020 as a result of the dual RMDs, and it pushes the pair into a higher tax bracket for 2020 as well. The lesson: if you will be 70½ by the time 2019 ends, take your initial RMD by the end of 2019 – it might save you thousands in taxes to do so. (3)

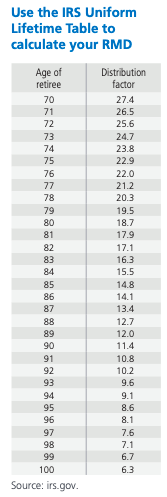

How do I calculate my first RMD?

I.R.S. Publication 590 is your resource. You calculate it using I.R.S. life expectancy tables and your IRA balance on December 31 of the previous year. For that matter, if you Google “how to calculate your RMD,” you will see links to RMD worksheets at irs.gov and a host of other free online RMD calculators. (1,4)

If your spouse is more than 10 years younger than you and happens to be designated as the sole beneficiary for one or more of the traditional IRAs that you own, you should use the I.R.S. IRA Minimum Distribution Worksheet (downloadable as a PDF online) to help calculate your RMD. (5)

If your IRA is held at one of the big investment firms, that firm may calculate your RMD for you and offer to route the amount into another account of your choice. It will give you and the I.R.S. a 1099-R form recording the income distribution and the amount of the distribution that is taxable. (6)

When I take my RMD, do I have to withdraw the whole amount?

No. You can also take it in smaller, successive withdrawals. Your IRA custodian may be able to schedule them for you. (7)

What if I have more than one traditional IRA?

You then figure out your total RMD by calculating the RMD for each traditional IRA you own, using the IRA balances on the prior December 31. This total is the basis for the RMD calculation. You can take your RMD from a single traditional IRA or multiple traditional IRAs. (1)

What if I have a Roth IRA?

If you are the original owner of that Roth IRA, you don’t have to take any RMDs. Only inherited Roth IRAs require RMDs. (7)

Be proactive when it comes to your first RMD

Putting off the initial RMD until the first quarter of next year could mean higher-than-normal income taxes for the year ahead. (2)

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Your approach to building wealth should be built around your goals & values.

Just what is comprehensive financial planning?

As you invest and save for retirement, you may hear or read about it – but what does that phrase really mean? Just what does comprehensive financial planning entail, and why do knowledgeable investors request this kind of approach?

While the phrase may seem ambiguous to some, it can be simply defined.

Comprehensive financial planning is about building wealth through a process, not a product.

Financial products are everywhere, and simply putting money into an investment is not a gateway to getting rich, nor a solution to your financial issues.

Comprehensive financial planning is holistic.

It is about more than “money.” A comprehensive financial plan is not only built around your goals, but also around your core values. What matters most to you in life? How does your wealth relate to that? What should your wealth help you accomplish? What could it accomplish for others?

Comprehensive financial planning considers the entirety of your financial life.

Your assets, your liabilities, your taxes, your income, your business – these aspects of your financial life are never isolated from each other. Occasionally or frequently, they interrelate. Comprehensive financial planning recognizes this interrelation and takes a systematic, integrated approach toward improving your financial situation.

Comprehensive financial planning is long range.

It presents a strategy for the accumulation, maintenance, and eventual distribution of your wealth, in a written plan to be implemented and fine-tuned over time.

What makes this kind of planning so necessary?

If you aim to build and preserve wealth, you must play “defense” as well as “offense.” Too many people see building wealth only in terms of investing – you invest, you “make money,” and that is how you become rich.

That is only a small part of the story. The rich carefully plan to minimize their taxes and debts as well as adjust their wealth accumulation and wealth preservation tactics in accordance with their personal risk tolerance and changing market climates.

Basing decisions on a plan prevents destructive behaviors when markets turn unstable.

Quick decision-making may lead investors to buy high and sell low – and overall, investors lose ground by buying and selling too actively. Openfolio, a website which lets tens of thousands of investors compare the performance of their portfolios against portfolios of other investors, found that its average investor earned 5% in 2016. In contrast, the total return of the S&P 500 was nearly 12%. Why the difference? As CNBC noted, most of it could be chalked up to poor market timing and faulty stock picking. A comprehensive financial plan – and its long-range vision – helps to discourage this sort of behavior. At the same time, the plan – and the financial professional(s) who helped create it – can encourage the investor to stay the course. (1)

A comprehensive financial plan is a collaboration & results in an ongoing relationship.

Since the plan is goal-based and values-rooted, both the investor and the financial professional involved have spent considerable time on its articulation. There are shared responsibilities between them. Trust strengthens as they live up to and follow through on those responsibilities. That continuing engagement promotes commitment and a view of success.

Think of a comprehensive financial plan as your compass.

Accordingly, the financial professional who works with you to craft and refine the plan can serve as your navigator on the journey toward your goals.

The plan provides not only direction, but also an integrated strategy to try and better your overall financial life over time. As the years go by, this approach may do more than “make money” for you – it may help you to build and retain lifelong wealth.

▲ Comprehensive Planning

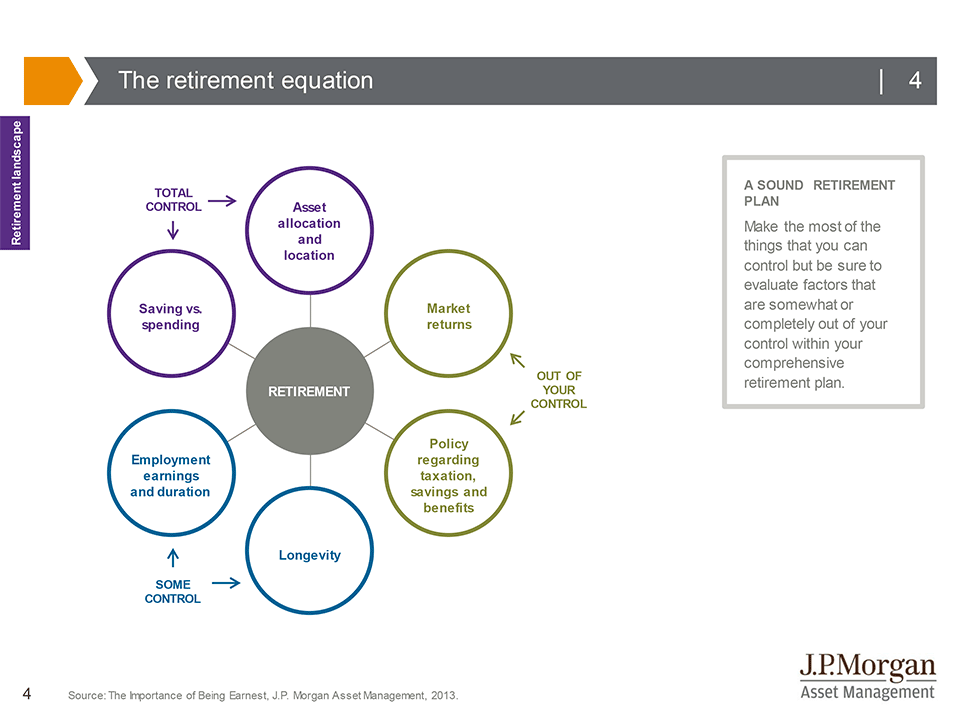

Planning for retirement can be overwhelming as individuals navigate various retirement factors over which we have varying levels of control. There are challenges in retirement planning over which we have no control, like the future of tax policy and market returns, and factors over which we have limited control, like longevity and how long we plan to work. The best way to achieve a secure retirement is to develop a comprehensive retirement plan and to focus on the factors we can control: maximize savings, understand and manage spending and adhere to a disciplined approach to investing.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

This guide walks through a simple framework to help you think clearly about retirement—from defining what matters most to understanding how your financial pieces fit together.

If you’re looking for help with retirement planning or investment management, you can learn more about how I work with clients at Weiss Financial Group.

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.

Scott Weiss, CFP®

RICP®, CRPC®, AAMS®, AWMA®, APMA®, CMFC®

ADDRESS:

704 Route 6

Mahopac, NY 10541

PHONE:

845-621-4700

Want more insights like this?

Get thoughtful, planning-focused insights delivered occasionally.

No noise. Just practical, planning-focused perspective. Unsubscribe anytime.