It depends on your goals, time horizon, and risk tolerance.

“Will I Outlive My Retirement Money?”

That’s one of the top fears for people who are starting to prepare for their retirement years.

So I have to chuckle a bit when I see headlines that say, “Here’s how much money Americans think they need to retire comfortably.” (1)

$1.9 million is the number, according to a nationwide survey of 1,000 employed 401(k) participants by a well-known financial services company. In 2019, the same survey reported the number was $1.7 million. But this year’s pandemic increased the total by $200,000.2

Is $1.9 million a realistic figure for retirement? It’s hard to say. The survey didn’t ask participants how they arrived at that figure or what information they used to draw that conclusion.

Determining How Much Money You Need in Retirement is a Process.

It shouldn’t be a number that you pull out of thin air.

The process should include looking at your current financial situation and developing an approach based on your goals, time horizon, and risk tolerance. The process should take into consideration all your potential sources of retirement income, and also may project what your income would look like each year in retirement.

A significant figure like $1.9 million does little good if you’re uncertain what it means for your retirement years. It’s a good idea to develop a retirement strategy combined with investment ideas designed to help you pursue the retirement you envision.

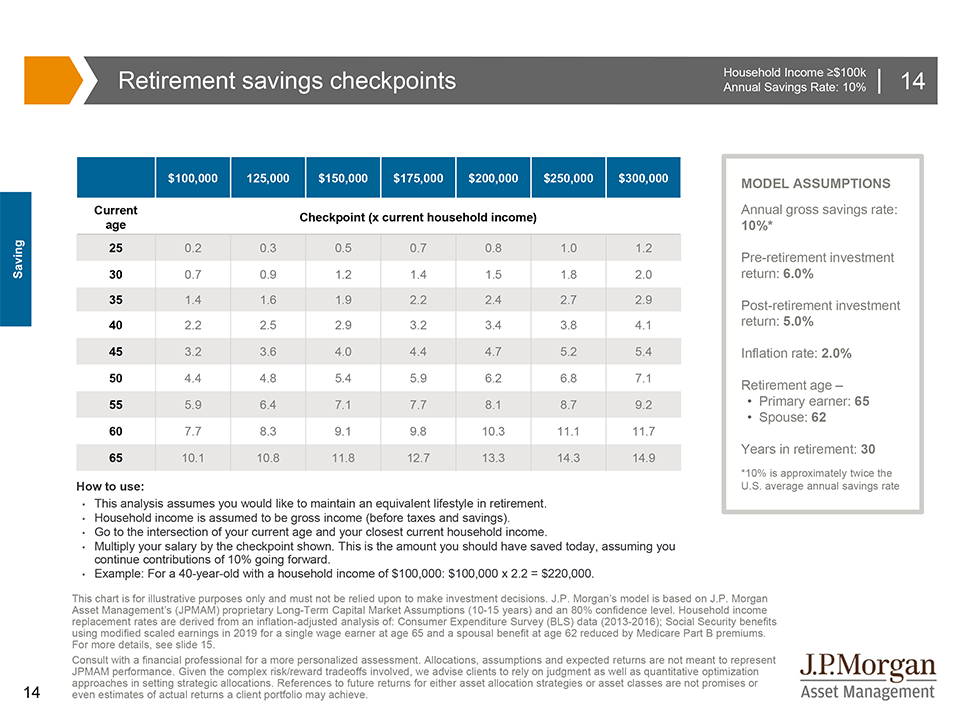

▲Retirement Saving Checkpoints

Achieving a financially successful retirement requires consistent savings, disciplined investing and a plan, yet too few Americans have calculated what it will take to be able to retire at their current lifestyle. This chart (for household incomes of $100,000 or more) helps investors to quickly gauge whether they are “on track” to afford their current lifestyle for 30 years in retirement based on their current age and annual household income. This analysis uses an appropriate income replacement rate (detailed on slide 15), an estimate of how much Social Security is likely to cover and the rate of return and inflation rate assumptions detailed on the right to determine the amount of investable wealth needed today, assuming a 10% gross annual savings rate until retirement. It is important to note that this analysis assumes a household with a primary earner who plans to retire at age 65 when the spouse is assumed to be 62. If an investor’s current retirement savings falls short of the amount for their age and income, developing a written retirement plan tailored to their unique situation with the help of an experienced financial advisor is a recommended next step.

Sources

- FoxBusiness.com, August 4, 2020

- Pressroom.aboutshwab.com, August 4, 2020

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/insights/guide-to-retirement

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.