Photo by Stanley Morales on Pexels.com

You can plan to meet the costs through a variety of methods.

How can you cover your child’s future college costs?

Saving early (and often) may be the key for most families. Here are some college savings vehicles to consider.

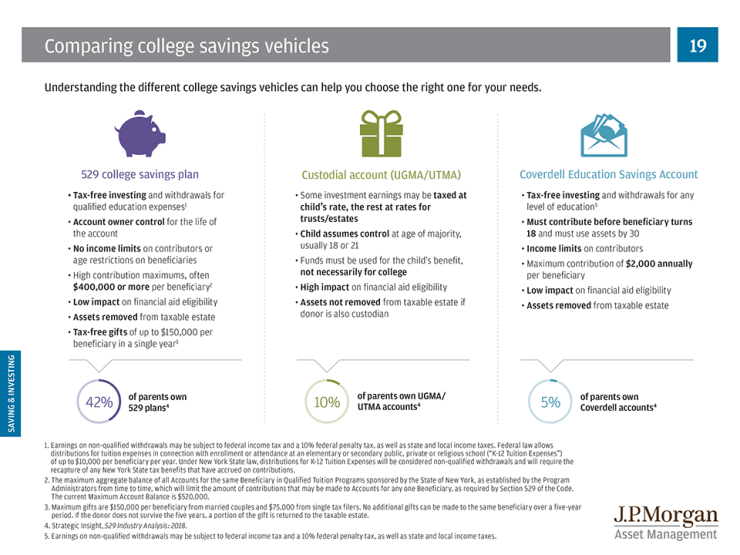

529 plans

Offered by states and some educational institutions, these plans let you save up to $14,000 per year for your child’s college costs without having to file an IRS gift tax return. A married couple can contribute up to $28,000 per year. (An individual or couple’s annual contribution to the plan cannot exceed the IRS yearly gift tax exclusion.) These plans commonly offer you options to try and grow your college savings through equity investments. You can even participate in 529 plans offered by other states, which may be advantageous if your student wants to go to college in another part of the country. (1,2)

While contributions to a 529 plan are not tax-deductible, 529 plan earnings are exempt from federal tax and generally exempt from state tax when withdrawn, as long as they are used to pay for qualified education expenses of the plan beneficiary. If your child doesn’t want to go to college, you can change the beneficiary to another child in your family. You can even roll over distributions from a 529 plan into another 529 plan established for the same beneficiary (or for another family member) without tax consequences. (1)

Grandparents can start a 529 plan, or other college savings vehicle, just as parents can; the earlier, the better. In fact, anyone can set up a 529 plan on behalf of anyone. You can even establish one for yourself. (1)

529 plans have been improved with two additional features. One, you can now use 529 plan dollars to pay for computer hardware, software, and computer-related technology, as long as such purchases are qualified higher education expenses. Two, you can now reinvest any 529 plan distribution refunded to you by an eligible educational institution, as long as it goes back into the same 529 plan account. You have a 60-day period to do this from when you receive the refund. (3)

Investors should consider the investment objective, risks, charges, and expenses associated with 529 plans before investing. More information about 529 plans is available in each issuer’s official statement, which should be read carefully before investing. A copy of the official statement can be obtained from a financial professional. Before investing, consider whether your state offers a 529 plan that provides residents with favorable state tax benefits.

Coverdell ESAs

Single filers with adjusted gross income (AGI) of $95,000 or less and joint filers with AGI of $190,000 or less can pour up to $2,000 annually into these tax-advantaged accounts. While the annual contribution ceiling is much lower than that of a 529 plan, Coverdell ESAs have perks that 529 plans lack. Money saved and invested in a Coverdell ESA can be used for college or K-12 education expenses. Coverdell ESAs offer a broader variety of investment options compared to many 529 plans, and plan fees are also commonly lower.(4)

Contributions to Coverdell ESAs aren’t tax-deductible, but the account enjoys tax-deferred growth and withdrawals are tax-free so long as they are used for qualified education expenses. Contributions may be made until the account beneficiary turns 18. The money must be withdrawn when the beneficiary turns 30 (there is a 30-day grace period), or taxes and penalties will be incurred. Money from a Coverdell ESA may even be rolled over tax-free into a 529 plan (but 529 plan money may not be rolled over into a Coverdell ESA). (2,4)

UGMA & UTMA accounts

These all-purpose savings and investment accounts are often used to save for college. When you put money in the account, you are making an irrevocable gift to your child. You manage the account assets. When your child reaches the “age of majority” (usually 18 or 21, as defined by state UGMA or UTMA law), he or she can use the money to pay for college. However, once that age is reached, that child can also use the money to pay for anything else.(5)

Imagine your child graduating from college debt-free. With the right kind of college planning, that may happen.

▲Comparing college savings vehicles

- 529 plan: Potential for tax-free investing for qualified education expenses;* high levels of flexibility, control and contribution maximums along with special gift and estate tax benefits.

- Custodial account: Less tax efficiency and control than other accounts; higher impact on financial aid eligibility.

- Coverdell account: Potential for tax-free investing for any qualified education expense; more restrictions and lower contributions than other accounts.

- Key takeaway: Not all college savings plans are the same. Differences among accounts can have a major impact on current taxes and future college funds.

* Earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, as well as state and local income taxes. Federal law allows distributions for tuition expenses in connection with enrollment or attendance at an elementary or secondary public, private or religious school (“K-12 Tuition Expenses”) of up to $10,000 per beneficiary per year. Under New York State law, distributions for K-12 Tuition Expenses will be considered non-qualified withdrawals and will require the recapture of any New York State tax benefits that have accrued on contributions.

Sources

- irs.gov/uac/529-Plans:-Questions-and-Answers

- time.com/money/3149426/college-savings-esa-529-differences-financial-aid/

- figuide.com/new-benefits-for-529-plans.html

- time.com/money/4102891/coverdell-529-education-college-savings-account/

- franklintempleton.com/investor/products/goals/education/ugma-utma-accounts?role=investor

- investopedia.com/articles/personal-finance/102915/life-insurance-vs-529.asp

- https://am.jpmorgan.com/us/en/asset-management/gim/protected/adv/products/college-savings-plan/college-planning-essentials

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.