Thinking about retirement? Not quite sure if you are ready? Here’s what you can do to get ready for a successful retirement:

REASON #1:

YOU DON’T HAVE A PLAN

Know Your Expenses And How You Will Pay For Them

This is a sure sign you are not ready. You need to know what your expenses are during retirement and how you are going to pay for them. Without a well thought out plan there is no way you are ready to retire. So, spend the time to build your plan or sit down with a CERTIFIED FINANCIAL PLANNER™ to help you.

REASON #2:

YOU HAVE TOO MUCH DEBT

Difficult to Pay Off When Living on a Fixed Income

Too much debt can really derail your retirement plan. Once you retire and are living on a fixed income it will become increasingly difficult to pay that debt off. In addition, too much debt can make dealing with financial emergencies nearly impossible.

REASON #3:

YOU HAVEN’T BUILT A RETIREMENT PORTFOLIO

You Need to Convert Your Savings Into Lifetime Income

During the accumulation phase of your retirement savings years, your goal is to save and grow your portfolio. As you enter retirement you need to refocus that goal and create a decumulation portfolio. Basically you need to convert your savings into lifetime income. In order to do this you’ll need to change your investment strategy. If you are still investing your portfolio with the sole purpose of growing it than you are probably not ready for retirement.

REASON #4:

YOU AND YOUR SPOUSE DON’T AGREE

The Change in Income Can Affect Your Lifestyle

So far I’ve just been talking about the financial aspects of retirement, but there is more to it than that. It’s important that you and your spouse are on the same page. Maybe you are ready but they are not. The change in income can affect your lifestyle so you want to make sure that you talk about this change and work through the issues this may cause before you decide to retire.

REASON #5:

YOU DON’T KNOW WHAT YOU’LL DO

This Can Lead to Overspending or Depression

Once you retire you will have a lot of time on your hands. Have you thought about what you will do with it? Not having a gameplan for your time can lead to overspending and even depression. Make sure you think through what you want to do, how you will pay for it and if it is really feasible. If you haven’t given this any thought, you are definitely not ready.

Sources:

1. This material was prepared, in part, by MarketingPro, Inc.

Thinking about borrowing money from your 401(k), 403(b), or 457 account? Think twice. Here are 6 reasons 401(k) loans are a bad idea.

REASON #1

Damages Retirement Prospects

A 401(k), 403(b), or 457 should never be viewed like a savings or checking account.

When you withdraw from a bank account, you pull out cash. When you take a loan from your workplace retirement plan, you sell shares of your investments to generate cash. You buy back investment shares as you repay the loan.

So in borrowing from a 401(k), 403(b), or 457, you siphon down your invested retirement assets, leaving a smaller account balance that experiences a smaller degree of compounding. In repaying the loan, you will likely repurchase investment shares at higher prices than in the past – in other words, you will be buying high. None of this makes financial sense.1

Most plans charge a $75 origination fee for a loan, and of course they charge interest – often around 5%. The interest paid will eventually return to your account, but that interest still represents money that could have remained in the account and remained invested.

REASON #2

Contributions Could Be Halted

May not be able to make additional contributions due to outstanding loans

Some workplace retirement plans suspend regular employee salary deferrals when a loan is taken. They can resume when you settle the loan.

REASON #3

Potential for Docked Pay

Your Take-Home Pay Could Be Docked

Most loans from 401(k), 403(b), and 457 plans are repaid incrementally – the plan subtracts X dollars from your paycheck, month after month, until the amount borrowed is fully restored.

REASON #4

A. May Have to Pay Back Immediately

30-60 Days: If You Quit, Get Laid Off Or Are Fired

This applies if you quit, get laid off or are fired. You will have 30-60 days (per the terms of the plan) to repay the loan in full, with interest.

If you are younger than age 59½ and fail to pay the full amount of the loan back, the IRS will characterize any amount not repaid as a premature distribution from a retirement plan – taxable income that is also subject to an early withdrawal penalty.1,2

Even if you have great job security, the loan will probably have to be repaid in full within five years. Most workplace retirement plans set such terms. If the terms are not met, then the unpaid balance becomes a taxable distribution with possible penalties (assuming you will not turn 59½ in the year in which repayment is due). If you default on the loan, the retirement plan may bar you from making future contributions.1

B. 5 Years To Repay

If Terms Are Not Met Unpaid Balance is Taxable

Even if you have great job security, the loan will probably have to be repaid in full within five years. Most workplace retirement plans set such terms. If the terms are not met, then the unpaid balance becomes a taxable distribution with possible penalties (assuming you will not turn 59½ in the year in which repayment is due). If you default on the loan, the retirement plan may bar you from making future contributions.1

REASON #5

You Get Taxed Twice!

Repay with after-tax dollars AND Taxed on withdrawals

When you borrow from an employee retirement plan, you invite that prospect. One, you will be repaying your loan with after-tax dollars. Two, those dollars will be taxed again when you withdraw them for retirement (unless your plan offers you a Roth option).

REASON #6

Why Go Into Debt to Pay Off Debt?

It’s Better to Go to a Reputable Lender for a Personal Loan

If you borrow from your retirement plan, you will be assuming one debt to pay off another. It is better to go to a reputable lender for a personal loan; borrowing cash has fewer potential drawbacks.

SMART TIP:

Your 401(k) Plan is NOT a Bank Account

Always remember, you should never confuse your retirement plan with a bank account.

If you’re considering retiring in the near future, you’ve probably heard or read that you need about 70% of your end salary to live comfortably in retirement. This estimate is frequently repeated … but that doesn’t mean it is true for everyone. It may not be true for you. Consider the following factors:

FACTOR #1

Your Health

Most of us will face a major health problem at some point in our lives. Think, for a moment, about the costs of prescription medicines, and recurring treatment for chronic ailments. These costs can really take a bite out of retirement income, even with a great health care plan.

FACTOR #2

Your Heredity

If you come from a family where people frequently live into their 80s and 90s, you may live as long or longer. Imagine retiring at 55 and living to 95 or 100. You would need 40-45 years of steady retirement income.

FACTOR #3

Your Portfolio

Many people retire with investment portfolios they haven’t reviewed in years, with asset allocations that may no longer be appropriate. New retirees sometimes carry too much risk in their portfolios, with the result being that the retirement income from their investments fluctuates wildly with the vagaries of the market. Other retirees are super-conservative investors: their portfolios are so risk-averse that they can’t earn enough to keep up with even moderate inflation, and over time, they find they have less and less purchasing power.

FACTOR #4

Your Spending Habits

Do you only spend 70% of your salary? Probably not. If you’re like many Americans, you probably spend 90% or 95% of it. Will your spending habits change drastically once you retire? Again, probably not.

Will You Have Enough?

When it comes to retirement income, a casual assumption may prove to be woefully inaccurate. However it doesn’t hurt to get a rough estimate. Using an online calculator link the one listed here can help you get started. You can use CNNMoney’s Will You Have Enough to Retire? calculator.

You won’t learn exactly how much retirement income you’ll need simply by watching this video and using the online calculator. But you will be on the right path. You may want to consider meeting with a fee-only, CERTIFIED FINANCIAL PLANNER™ who can help estimate your lifestyle needs and short-term and long-term expenses

Sources:

This material was prepared by MarketingLibrary.Net Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information should not be construed as investment, tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy.

Feeling like you need to start saving and planning for retirement? Here are 6 smart tips to get you going:

TIP #1

Make Savings A Top Priority

Pay Yourself First

Resolve to pay yourself first. That is, direct money toward your retirement before you do anything else, like pay the bills or spend it on needs or wants. Always remember, your future should come first.

TIP #2

Invest Some or Most of What You Save

Potential to Grow and Outpace Inflation

Investing in equities is vital, because it gives you the potential to grow and compound your money to outpace inflation. With interest rates so low right now, ultra-conservative fixed-income investments are generating very low returns, and most savings accounts are offering minimal interest rates. Thirty or forty years from now, you will probably not be able to retire solely on your savings. If you invest your retirement money in equities, you have the opportunity to retire on the earnings and compound interest accumulated through both saving and investing.

TIP #3

The Effect of Compounding Can Be Profoud

The Earlier You Start The Better

The effect of compounding can be profound. Suppose you want to retire with $1 million in savings. Let’s project that your investments will yield 6.5% a year between now and the year you turn 65 and, for the sake of simplicity, we will put any potential capital gains taxes and investment fees aside. Given all that, how early would you have to begin saving and investing to reach that $1 million goal, and how much would you have to save per month to reach it?

How early would you have to begin saving and investing to reach that $1M goal?

START AT 45 = $2,039

START AT 35 = $904

START AT 25 = $438

If you start saving at 45, the answer is $2,039. If you start saving at 35, the monthly number drops to $904. How about if you start saving at 25? Only $438 a month would be needed. So, as you see the earlier you start saving and investing, the more compounding power you can harness.

TIP #4

Strive to Get The Match

Some Companies Contribute 50 cents for Every Dollar

Some companies reward employees with matching retirement plan contributions; they will contribute 50 cents for every dollar the worker does or, perhaps, even match the contribution dollar-for-dollar. An employer match is too good to pass up.

TIP #5

Invest in A Way You Are Comfortable With

Avoid Investments That are Convoluted or Mysterious

In the mid-2000s, some Wall Street money managers directed assets into investments they did not fully understand, a gamble that contributed to the last bear market. Take a lesson from that example and avoid investing in what seems utterly convoluted or mysterious.

TIP #6

Realize That Friends And Family May Not Know It All

Your Main Concern Should Be Staying Invested

The people closest to you may or may not be familiar with investing. If they are not, take what they tell you with a few grains of salt.

Getting a double-digit annual return is great, but the main concern is staying invested. The market goes up and down, sometimes violently, but there has never been a 20-year period in which the market has lost value. As you save for the long run, that is worth remembering.

Sources:

This material was prepared, in part, by MarketingPro, Inc.

Getting ready to retire or have you just started your retirement? Here are 7 important ages you should to be ready for:

AGE 55

Can Make Withdrawals Without 10% Penalty if Retired

At age 55 you can withdraw from your 401(k) or 403(b) plan without the 10% penalty if you retire or get fired. Also, if your employer offers a pension you may be eligible for full retirement benefits, if you meet the plan requirements.

AGE 59 1/2

Can Make Withdrawals Without 10% Penalty

This is an important age to remember. Once you turn 59 ½ you can withdraw money from IRA’s and deferred annuities without paying the 10% penalty for early withdrawal.

AGE 62

Can Start Reduced Social Security Benefits

This is another big year. At age 62 you can start receiving Social Security benefits. However, keep in mind your benefits will be reduced since you will not have reached full retirement age. The other thing is that at age 62 you may be eligible for full pension benefits if applicable to your situation.

AGE 65

Qualify for Medicare Benefits

This is when you qualify for medicare benefits. Also, with most pension plans you become eligible for your full benefits.

AGES 66 & 67

Eligible for Full Social Security Benefits

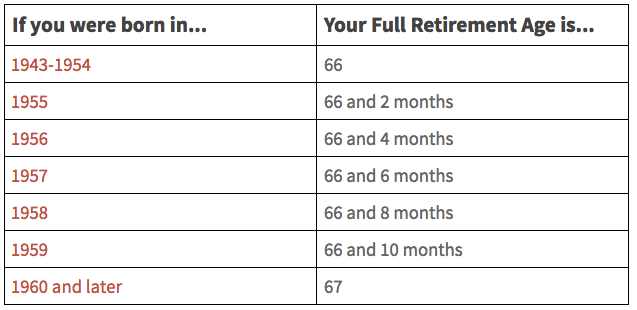

Ok, I have two ages here. But, they are pretty much for the same thing so I lumped them together. At age 66 you become eligible for full social security benefits, if you were born between 1943-1954. Everyone born after 1954 follows this table:

AGE 70

Your Social Security Benefits Max Out

Once you hit 70 you should start collecting your social security benefits if you haven’t already done so because your benefits will be maxed out. Waiting to collect benefits until age 70 can actually be a great strategy if you are trying to max out social security benefits or are concerned about longevity.

AGE 70 1/2

Must Start Your Required Minimum Distributions (RMD’s)

Finally, age 70 ½ . When you turn 70 ½ you will be required to start withdrawing specified amounts from your 401(k)’s and IRAs. This is called your Required Minimum Distribution or RMD for short. You must begin these withdrawals once your turn 70 ½ but you actually have until April 1st of the year following the year you actually turn age 70 1/2 . I know, confusing right? Let me give you an example. Let’s say you turn 70 ½ in January 2016, you will need to take your RMD by April 1st, of 2017. Now, you can take it in 2016 but you don’t have to. Going forward, every year after your first RMD you will be required to take the distribution buy December 31st.

If you haven’t retired already, at some point you’ll probably want to. Financial security in retirement doesn’t just happen. It takes planning, commitment and money. You’ll need enough money to potentially live on for at least 20 years, probably more. With the average life expectancy in the U.S. at nearly 80 and growing (1), you’ll want to be sure you can maintain the lifestyle you envision throughout your retirement years.

To help you focus on what you should be doing to succeed, here are 7 planning tips:

1. Make Saving a Habit

If you are already saving every month, awesome! Keep going! If you’re not, start now. The sooner you start the more time your money has to grow.

2. Know Your Retirement Expenses

This is much easier to do the closer you get to retirement. A twenty or thirty year old may have no idea what those numbers will eventually be. If that is you, concentrate more on the other tips. For those of you with retirement in your sightline, figure you will need AT LEAST 70% of your pre-retirement income to live comfortably. Knowing what you need is the key to getting what you need. The key to a secure retirement is to have a clearly defined goal.

3. Participate in your 401(k) or 403(b)

If your employer offers a 401(k) plan or 403(b) plan sign up and aim to contribute to the maximum. Over time, compound interest and tax deferrals can make a huge difference in the amount you accumulate for retirement.

4. Invest Wisely

Diversify your savings to reduce risk (i.e. don’t put it all on black!). In a nutshell, risk simply means how much money could you potentially lose with your investments. To check your current tolerance for risk use our free tool. It will give you something called your Risk Number™ which is a great starting place to see how much risk you can emotionally handle. You can then compare that to the Risk Number™ of your current portfolio and see if they match up or if you potentially need to make changes. Keep in mind, your investment mix may need to change over time due to age, goals, and circumstances, so it’s always a good idea to monitor your risk tolerance and portfolio allocation. Remember, financial knowledge and financial security go hand in hand.

5. Check Your Social Security Benefits

Social Security benefits provide supplemental income to you and your spouse during retirement. If you are counting on social security to bail you out, think again. Social Security provides enough for you to live around the poverty line. Check the Social Security website to see how much the government will pay you every month.

6. Ask Questions

The more you know, the better your chances of enjoying financial security in your retirement years. Talk with your accountant or financial advisor. Better yet, book a meeting with me right now! Ask questions and get good advice. Build a plan, and stick with it.

7. Make Planning for Your Retirement a Priority

Use our retirement check-up tool to find out if you are on the right track. It’s never too early or too late to start saving for your future. However, the longer you wait or leave things to chance, the less likely you will live a financially secure retirement.

“Planning is bringing the future into the present so that you can do something about it now.” -Alan Lakein

If you know anyone that could benefit from this advice, feel free to share this video with them. Good luck on your journey toward a financially secure retirement.

For more financial planning tips, download my free report: “8 Steps to Organize and Optimize Your Financial Life”. Thanks for reading!

You’re family, friends and co-workers have thrown more parties and functions than the Yankees did for Derek Jeter.

But are you ready?

Just as you proudly grew your financial nest egg, hopefully you’ve also invested in your health.

How do expect to insure a secure retirement without your health?

How do you expect to enjoy all of your hard work if you’re going to the doctor the majority of those golden years.

So, investing in your health is just as important for your bottom line as investing in your 401(k)

A major life change like transitioning into retirement can be stressful, even if retirement is a happy and welcome change from working.

So what’s the secret?

Start now! You’ve already planned for your fiscal future, why should your physical future be any different.

Here are 3 tips you can use to stay healthy as you move into retirement and beyond.

1. Get Moving and Stay Moving:

Regular physical activity also improves functional abilities we need for daily living.

These benefits are both physical and mental. Physical activity improves mood and can create more energy.

Regular physical activity can reduce your chances of diseases such as cancer and Heart disease. It will improve balance, agility and strength.

Older adults can even increase muscle and bone strength through using their major muscle groups at least twice per week.

Age means nothing! staying active will allow you to feel healthier and enjoy life more than ever!

In the years before you retire, I would suggest developing a routine of regular physical activity that will carry on into retirement.

When you retire, your daily routines will certainly change. This change can be a challenge; one of the best ways to adapt to retired life is to follow fun and fresh routines that include physical activity.

Here are some tips:

Do what you love to do. This could mean activities you have done for years, such as walking, swimming or tennis – or something new and different like Training For Warriors or yoga.

Lift weights.

Find a partner or a group of friends who enjoy similar activities. This can help motivate you!

Take advantage of available times while others are working and schedule your activities to avoid busy times on the golf course or ski trails, or at the swimming pool and gym.

Be active with your family, take your kids or grandchildren walking, hiking camping, fishing, cycling or even kayaking. Get involved with their lives and what they’re doing.

Aim for at least 3-5 days of physical activity each week, remember it doesn’t have to be super intense everyday. Mix your and match your activities, keep it fresh!

2. Healthy Eating:

Are you looking to spend all of you money fixing problems caused by a poor diet?

I ask because your diet greatly influences your long-term health. I’m not saying you can’t enjoy yourself and never have some of your favorite (but less healthy) foods. However, you should pay attention to what you eat.

Sugar and Ultra-Processed foods are making us fat and shortening our lives. Live happier and healthier by eliminating all processed foods such as grains, sugar and industrial oils.

Fruits and vegetables can help your health, as can nuts, fish, and other heart-healthy foods. Also, consider “brain foods” like salmon and blueberries. These can improve your mood and help your brain avoid deterioration.

I have profiled healthy food options off of the TFW Warrior 20 nutrition checklist and broken down the foods into Proteins, Carbohydrates & Fats.

Avoid spending your money on future medical bills and start incorporating these foods into your diet.

Proteins:

1. Lean Meats

Including meat in a well-balanced diet is a way to get a sufficient amount of high-quality protein. You don’t need to give up meat just because you’re trying to lose weight. The key is to stick with lean meats because they contain less total fat, as well as lower amounts of saturated fats.

Fatty fish is high in protein and provides heart-healthy omega-3 fatty acids. If it’s not wild caught don’t eat it!

Examples: Salmon, Sardines, Mackerel, Anchiovies

3. Eggs

Eggs are a nutritional powerhouse. The white packs a lot of high-quality protein and the yolks healthy fats & cholesterol as well as micronutrients like vitamin A, calcium, and phosphorous.

If you can afford it, look for local varieties of pasture raised eggs. Try the farmer’s market or gourmet grocery stores. If not, at least stick with organic, cage free, free range eggs. At the very least they weren’t packed into cages and pumped with drugs. These eggs tend to be pricey however your health is worth money.

Carbohydrates:

This just in….Carbs are not the ENEMY! If you are a person that likes to exercise (and you all should be that person) then a low-carb diet for a long period of time may hurt more than it helps. Reducing your intake of healthy carbs can lead to a slow metabolism, lower levels of muscle/strength-building hormones & higher levels of stress hormones. As a result your weight loss will probably slow down or stop.

1. Sweet Potatoes & Yams

Tubers like sweet potatoes are loaded with carbohydrate energy. They are loaded with Vitamin A, which is important in the synthesis of protein.

2. Quinoa

Known as the “mother of all grains” by the Incas. Quinoa is higher in protein than most grains and can be a great replacement for rice. It is also gluten-free making it an option for those of us with gluten intolerance.

3. Legumes

Beans such as Lentils and Kidney contain complex carbohydrates as well as fiber & protein. Beans are loaded with antioxidants and minerals such as magnesium, iron zinc & potassium.

* Beans are difficult to digest so if you are a person that likes to eat beans I would suggest soaking them prior to consuming.

Healthy Fats:

Our bodies need healthy fats. They help slow down the digestion process so our bodies have more time to absorb nutrients, and help provide a sustainable level of energy.

1. Coconut Oil

Coconut oil is one of the few foods that can be classified as a “superfood.”

It has a unique combination of fatty acids that have a positive effect on fat loss and better brain function. Other health benefits include skin care, stress relief, cholesterol level maintenance, boosted immune system, proper digestion and regulated metabolism.

2. Nuts

Many nuts are rich in mono-unsaturated & omega-3 fatty acids. Omega-3 fatty acids help with inflammation and brain function.

Examples: Almonds (almond butter), Cashews (cashew butter) Walnuts, Pecans, Macadamias, Pistachios. Avoid processed nuts as they lose a lot of nutrients instead opt for raw nuts. The same goes for nut butters, avoid nut butters that are high in hidden sugars and hydrogenated oils. Look for the most minimally processed options possible.

3. Seeds

Seeds, like nuts are a good source of fat. Seeds are rich in fiber and can help you feel fuller longer

How often do you say you wish you had more time to do amazing things like drive cross country or sky dive.

Well you will when you retire!

Retirement opens up doors and once in a lifetime opportunities for bucket list activities to become a reality. You can do anything and become anything that you want. If you’ve always wondered what would have happened if your life had taken a different turn, this is your opportunity to make that turn and see what happens.

Start fresh!

Today people that adopt a healthy lifestyle can live well into their 80’s and 90’s. So get out and hike the Appalachian Trail , go back to school, learn to play an instrument or open a business like Colonel Sanders who started Kentucky Fried Chicken at age 65!

With a healthy body, strong mind and solid planning you can look forward to a happy, active and fulfilling retirement.

Sorry to burst your bubble, but I don’t believe in the ‘magic number.’ Unfortunately, your wants and needs along with the unpredictability of life cause your ‘number’ to change over time. If you are not regularly assessing your financial situation, having a single number stuck in your head could be counter productive to your success.

So What Do I Do Now?

Instead of focusing on your ‘magic number’, I recommend building a solid retirement plan, setting a goal to save 10% -20% of what you make, invest your money, and regularly review and update that plan. In order to more accurately determine how much to set aside for retirement, you need to have a clear idea of how much you are spending annually to support your current lifestyle. Next, you will need to think through how those expenses may change in retirement. Will you move to a less expensive location? What about commuting expenses? How often will you need to purchase vehicles? Once you’ve thought through those possibilities, or any others, you will want to think about the lifestyle you hope to have in retirement. Do you want to travel or are you a homebody? Do you want to join a club or take up a new hobby? Think about how much each of these activities may cost and work that into your plan.

What Else Should I Look At?

The next piece of the puzzle is to take a look at any guaranteed income you may have from Social Security, pensions, or annuities. The more guarantees you have the less you’ll need in savings to replace your income during retirement. Also, it’s a good idea to think about whether you will continue to do some type of work to assist in meeting your income needs. My final recommendation is to factor in your health. Are you relatively healthy or do you need to plan for additional medical costs during retirement?

Run the Numbers

Truthfully, the closer you get to retirement the more accurate your projections will be. However, when you are younger you can still work with approximations and run monte-carlo simulations on your numbers. Just be sure to revisit those numbers on a regular basis to account for changes in your income, spending habits, and lifestyle. As a rule of thumb, you will typically need to replace 70%-90% of your pre-retirement income to maintain your pre-retirement lifestyle. But, keep in mind, this is merely a rule of thumb. Your personal needs can vary depending on the factors I just discussed.

How much you’ll need for retirement is directly dependent on the lifestyle you envision. If you are willing to make some sacrifices or have enough guaranteed income you may not need to save as much. On the other hand, for most people, if you want to maintain your current lifestyle you’ll need to save and invest regularly and monitor and adjust your retirement plan on an on-going basis in order to create the retirement lifestyle of your dreams.

Want a quick assessment of where you stand for your retirement? You can use my Retirement Check-Up tool to see how you are doing right now and if you might need to make any adjustments to your plan.

The days of staying at the same job your entire working life are pretty much over. Also gone are the days when your company would finance your retirement with a comfortable pension. That responsibility now falls squarely on you. Subsequently, your 401(k) is a great way to build your retirement war chest.

So, what is the smartest thing to do with the money in that 401(k) when you leave for the next big thing, get laid off, or retire? You basically have four options. The best one for you will depend on your situation and your objectives.

OPTION 1: Take a Lump Sum Distribution

With this option the company closes your account and sends you a check for whatever you’ve accumulated minus taxes. You will be taxed at ordinary income tax rates and could potentially be bumped into the next tax bracket if the distribution is large enough. Also, if you are under age 59 1/2, you may be subject to a 10% early distribution penalty.

Who could this option be good for?

Someone who got laid off and really needs the money. They understand the tax ramifications but there is really no other option to keep the lights on until they find a new job. As a side note, this is a good reason to build an emergency fund.

If you have accumulated very little money (i.e. a few hundred dollars or so) because you just started contributing to your 401(k) and feel the hassle of selecting another option is not worth it, then you could take the distribution. It’s not the best thing to do, but it won’t really hurt you.

OPTION 2: Leave the Money Where it is

This option is self explanatory. You just leave the money within the existing 401(k) plan at your previous employer. There is a comfort factor here; you know the plan, most likely know how to use the online access, are familiar with their customer service and know the investment options inside the plan. The downside is that you can no longer add money to this plan, get the company match, or possibly take loans if needed. You are also limited to the investment options offered by the plan which could be good or bad depending on the quality of the investments offered inside the plan. Also, keep an eye on expenses. They can vary significantly from plan to plan. In some cases you may be getting a better deal on the mutual funds inside the plan, but in other cases you may pay more for those same funds outside the plan. Be sure to review the plan documents. One final note about leaving your 401(k) with your old employer. Over the years, if you don’t stay on top of things, you can easily accumulate several retirement accounts spread among your previous employers. For many people, it can be confusing to keep track of everything which could, ultimately, be detrimental to your wealth.

Who could this option be good for?

If you are age 55 or older and need to begin taking distributions from your 401(k) for retirement, this might be a good option for you. In an IRA, you must wait until age 59 1/2 to take a distribution without incurring the extra 10% early distribution penalty. But, with a 401(k), if you leave your job the year you turn age 55 or later, the IRS will allow you to begin withdrawals without incurring the extra penalty. (Here are the IRS rules)

If you land another job, like your new employer’s 401(k) and want to roll your money into the new plan, then leave your money in your old 401(k) until you can make the transfer. There is no need to roll it over to an IRA for a short period of time and roll it over again several months later.

If you just really like your old employer’s 401(k) plan and are a do-it-yourself-er who will keep track of the money, perform the necessary re-balancing and periodically review the investments, leave it there.

OPTION 3: Roll your old 401(k) into your new 401(k)

If your new employer’s plan allows it, you can roll your old 401(k) over into your new 401(k). Doing this will help keep all your 401(k) assets together and make it simpler to manage your entire retirement portfolio. Keep in mind, your money will now be subject to the rules and regulations of the new plan and can only be invested in the options available inside the new plan. However, there is a lot to be said for keeping things simple. One other potential benefit is that your money will be available for plan loans if needed.

Who could this option be good for?

This is a good option for staying organized. Having all your money in one account is much easier to keep track of.

This is also a good option for the do-it-yourself-er who stays on top of their investments and regularly re-balances their portfolio

If you are in a situation where it maybe necessary to to take a loan from your 401(k), then rolling your money into the new plan is an option. Although I do not recommend 401(k) loans, sometimes they may be the only option. The important thing to be aware of when taking a 401(k) loan is that when you leave the company the loan needs to be paid back in full or the balance of the loan will be treated as a distribution and taxed accordingly.

If you have serious debt concerns, keeping your money in a 401(k) rather than rolling it over into an IRA may be the better option. Some states offer greater creditor protection for a 401(k) then they do for an IRA.

If you will be working into your 70’s and do not yet want to begin withdrawing money, then keeping your money in a 401(k) is better than an IRA rollover. With an IRA you must take Required Minimum Distributions (RMDs) at age 70 1/2. Not so with a 401(k), as long as you are still working at the company maintaining the plan.

OPTION 4: Roll your old 401(k) into an IRA

The final option is to roll your old 401(k) into an IRA. Typically what happens is you open an IRA account and instruct your old employer to transfer the money directly into your IRA. Sometimes, however, your company will send a check directly to you which must be deposited into your IRA within 60 days or be subject to taxes at ordinary rates and possibly the 10% early withdrawal penalty (Here are the IRS Rules). One big benefit of rolling your 401(k) over into an IRA is that you will have more investment options.

Who could this option be good for?

Great for someone who changes jobs a lot. You can have one account that you roll your old 401(k) accounts into as your situation changes.

If you plan to work with a fiduciary advisor to help you manage your investments, this may be the best option.

If you are heading into retirement and want assistance creating a retirement income plan, an IRA rollover could be a good option for you.

If you are a do-it-yourself-er, this might be a good option.

If you need to pay for college, you may be able to withdraw money from your IRA and not incur the 10% penalty. You don’t have the ability to do this with a 401(k). You will, however, need to pay ordinary income tax on the withdrawal. In most cases, I do not recommend using IRA money to pay for college, however, it is a potential benefit of an IRA.

If you are a first time home-buyer you can take $10,000 out of an IRA for a down payment without incurring the 10% early withdrawal penalty. Taxes at ordinary income tax rates will still apply.

So, those are your four options. What’s best for you will depend on your situation and the type of assistance you want managing your money. For me, I always rolled over my old 401(k) accounts into an IRA. I prefer keeping my retirement assets together, manage my own money, and do not like being restricted by the investment options inside a 401(k).

This guide walks through a simple framework to help you think clearly about retirement—from defining what matters most to understanding how your financial pieces fit together.

If you’re looking for help with retirement planning or investment management, you can learn more about how I work with clients at Weiss Financial Group.

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.

Scott Weiss, CFP®

RICP®, CRPC®, AAMS®, AWMA®, APMA®, CMFC®

ADDRESS:

704 Route 6

Mahopac, NY 10541

PHONE:

845-621-4700

Want more insights like this?

Get thoughtful, planning-focused insights delivered occasionally.

No noise. Just practical, planning-focused perspective. Unsubscribe anytime.

Thinking about retirement? Not quite sure if you are ready? Here’s what you can do to get ready for a successful retirement:

Thinking about retirement? Not quite sure if you are ready? Here’s what you can do to get ready for a successful retirement: Thinking about borrowing money from your 401(k), 403(b), or 457 account? Think twice. Here are 6 reasons 401(k) loans are a bad idea.

Thinking about borrowing money from your 401(k), 403(b), or 457 account? Think twice. Here are 6 reasons 401(k) loans are a bad idea. What is enough?

What is enough?  Feeling like you need to start saving and planning for retirement? Here are 6 smart tips to get you going:

Feeling like you need to start saving and planning for retirement? Here are 6 smart tips to get you going: