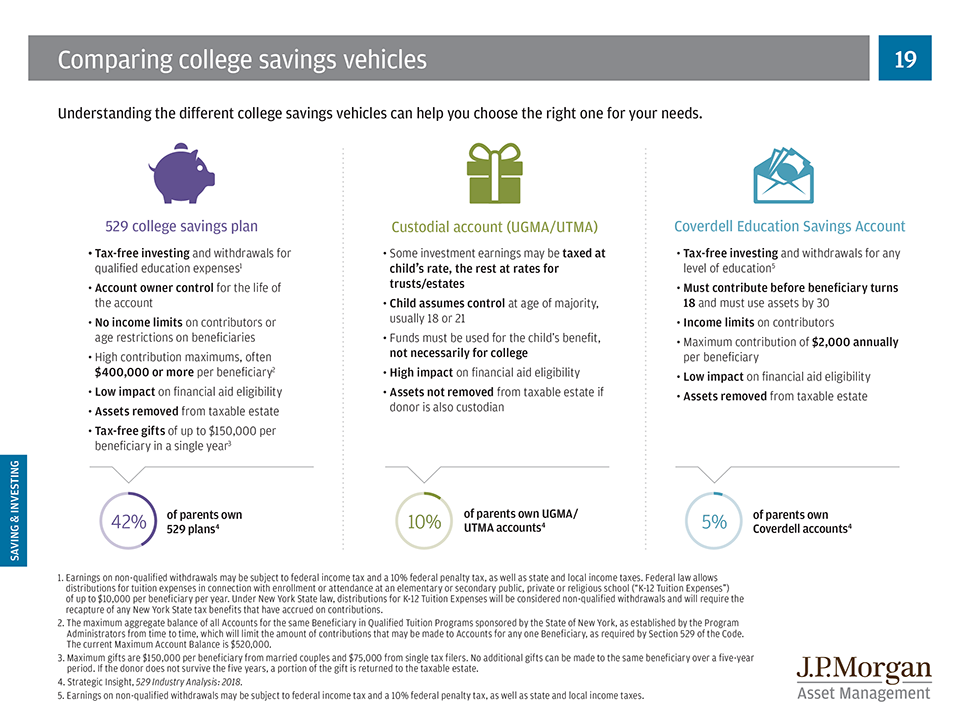

Preparing for retirement just got a little more financial wiggle room. The Internal Revenue Service (IRS) announced new contribution limits for 2022.

401(k) & 403(b)

For workplace retirement accounts (i.e. 401(k), 403(b), amongst others), the contribution limit rises $1,000 to $20,500. Catch-up contributions remain at $6,500. (1)

Traditional IRA

Staying put for 2022 are traditional Individual Retirement Accounts (IRAs), with the limit remaining at $6,000. The catch-up contribution for traditional IRAs remains $1,000 as well. (1)

Roth IRA

Eligibility for Roth IRA contributions has increased, as well. These have bumped up to $129,000 to $144,000 for single filers and heads of households, and $204,000 to $214,000 for those filing jointly as married couples. (1)

SIMPLE IRA

Another increase was for SIMPLE IRA Plans (SIMPLE is an acronym for Savings Incentive Match Plan for Employees), which increases from $13,500 to $14,000. (1)

If these increases apply to your retirement strategy, a financial professional may be able to help make some adjustments to your contributions.

| Contribution Limits (3,4) | 2022 | 2021 | Change |

|---|---|---|---|

| 401(k) & 403(b) maximum employee elective deferral | $20,500 | $19,500 | +$1,000 |

| 401(k)s 403(b), etc. employee catch-up contribution (if age 50 or older by year-end)* | $6,500 | $6,500 | None |

| Traditional IRA & Roth IRA | $6,000 | $6,000 | None |

| Traditional IRA & Roth IRA catch-up contributions (if age 50 or older by year-end)* | $1.000 | $1,000 | None |

| SIMPLE IRA | $14,000 | $13,500 | +$500 |

RMDs Explained

Once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA) or Savings Incentive Match Plan for Employees IRA in most circumstances. Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Once you reach age 72, you must begin taking required minimum distributions from your 401(k), 403(b), or other defined-contribution plans in most circumstances. Withdrawals from your 401(k) or other defined-contribution plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

5-Year Holding Period for Roth IRAs

To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

Sources

- CNBC.com, November 5, 2021

- https://www.investopedia.com/retirement/401k-contribution-limits/

- https://www.irs.gov/pub/irs-drop/n-21-61.pdf

- https://www.irs.gov/retirement-plans/401k-plans-deferrals-and-matching-when-compensation-exceeds-the-annual-limit

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.