Preparing for retirement just got a little more financial wiggle room. The Internal Revenue Service (IRS) announced new contribution limits for 2022.

401(k) & 403(b)

For workplace retirement accounts (i.e. 401(k), 403(b), amongst others), the contribution limit rises $1,000 to $20,500. Catch-up contributions remain at $6,500. (1)

Traditional IRA

Staying put for 2022 are traditional Individual Retirement Accounts (IRAs), with the limit remaining at $6,000. The catch-up contribution for traditional IRAs remains $1,000 as well. (1)

Roth IRA

Eligibility for Roth IRA contributions has increased, as well. These have bumped up to $129,000 to $144,000 for single filers and heads of households, and $204,000 to $214,000 for those filing jointly as married couples. (1)

SIMPLE IRA

Another increase was for SIMPLE IRA Plans (SIMPLE is an acronym for Savings Incentive Match Plan for Employees), which increases from $13,500 to $14,000. (1)

If these increases apply to your retirement strategy, a financial professional may be able to help make some adjustments to your contributions.

Contribution Limits (3,4)

2022

2021

Change

401(k) & 403(b) maximum employee elective deferral

$20,500

$19,500

+$1,000

401(k)s 403(b), etc. employee catch-up contribution (if age 50 or older by year-end)*

$6,500

$6,500

None

Traditional IRA & Roth IRA

$6,000

$6,000

None

Traditional IRA & Roth IRA catch-up contributions (if age 50 or older by year-end)*

$1.000

$1,000

None

SIMPLE IRA

$14,000

$13,500

+$500

RMDs Explained

Once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA) or Savings Incentive Match Plan for Employees IRA in most circumstances. Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Once you reach age 72, you must begin taking required minimum distributions from your 401(k), 403(b), or other defined-contribution plans in most circumstances. Withdrawals from your 401(k) or other defined-contribution plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

5-Year Holding Period for Roth IRAs

To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Most people worry about not having enough money for retirement. But did you also know that there is such a thing as having too much money? Too much money may not necessarily be a bad thing, but you do need to worry about required minimum distributions (RMDs). Here’s what you need to know about RMDs.

RMDs Depend on Your Age

The main point of RMDs is to keep money from staying tax-free forever. The government gave a temporary tax break to encourage you to save for retirement, but it still wants that tax money. A required minimum distribution is a required withdrawal from your retirement account. It counts in your taxable income just like any other withdrawal in retirement.

Currently, RMDs start when you hit age 72 (or 70½ if you turned 70½ prior to January 1, 2020) and they are calculated to empty your retirement account within your expected life expectancy. (1) Each year, you need to withdraw a certain percentage of your account with the percentage going up as you age. However, it’s important to realize that you do not have to spend all of this money. You can also reinvest it into a taxable account.

Not Taking the RMD Can Mean Big Penalties

Thinking about skipping RMDs to avoid taxes? Think again. Not only do you still have to pay the taxes on the RMD amount, but you’ll also owe a 50 percent penalty.

For example, if you were supposed to withdraw $10,000 but didn’t, the IRS will charge you an extra $5,000. The penalty repeats every year until you catch up on your RMDs from previous years.

RMDs Can Throw a Wrench in Your Tax Planning

There are many reasons why you might want to reduce your taxable income in retirement. These can include qualifying for things like Medicaid subsidies, avoiding taxes on your Social Security benefits, trying to stay in a lower capital gains tax bracket, or just wanting to pay fewer taxes.

Required minimum distributions can throw a major wrench in your tax planning because not only are they not avoidable, they can suddenly increase if the market surges. If you’re using a tax strategy that requires reducing your income to a certain level, it’s important to build in flexibility for your RMDs.

RMDs Can Be Avoided

There are still ways to reduce or even avoid RMDs altogether. The main idea is to get the money out of your retirement account when you want to not when the IRS wants you to.

One method is to make extra withdrawals at the end of the year. In December, you can estimate your taxes for the year. If you still have room in a lower tax bracket or below the income you need to stay under, you can withdraw additional money. When next year’s RMDs are calculated, it will be on a lower account balance.

You can also convert to a Roth IRA instead of taxing the money out of a tax-advantaged account. Roth IRAs don’t have RMDs because the money has already been taxed. When you make the conversion, you pay ordinary income tax rates on the amount you converted. There are no penalties even if you do the conversion before you turn 59 1/2.

This content is developed from sources believed to be providing accurate information, and provided by Twenty Over Ten. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Most likely, you’ve heard what’s brewing in Washington, D.C., called by one of these names.

The Build Back Better Act.

Or the $3.5 trillion budget reconciliation bill. Or the Jobs and Economic Recovery Plan for Working Families. (1)

Regardless of what name you’ve heard, one fact is clear: It is likely to be months before any action is taken.

When bills are being worked on—especially one that’s this size—it’s a good time to take a quick Civics refresher. Right now, the bill is “in committee” with both the House of Representatives and the Senate. The committees are filling in the policy details and the exact financial figures, which can be a long process. (2)

It will then be up to the House and Senate to vote on an identical version of a final bill—if both can agree to a final version. (2)

Right now, it would be hasty to make any portfolio changes based on what’s being discussed and debated. An ambitious investor would have to guess at what policies will be in the final bill, estimate the financial impact, and determine what portfolio changes should be made. That’s a tall order.

So as difficult as it may be, the best approach is to wait-and-see.

This article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and financial professionals before modifying your tax strategy.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Year after year, certain taxpayers resort to schemes in an effort to put one over on the Internal Revenue Service (I.R.S.). These cons occur year-round, not just during tax season. In response to their frequency, the I.R.S. has listed the 12 biggest offenses – scams that you should recognize, schemes that warrant penalties and/or punishment.

1. Phishing

If you get an unsolicited email claiming to be from the I.R.S., it is a scam. The I.R.S. never reaches out via email, regardless of the situation. If such an email lands in your inbox, forward it to phishing@irs.gov. You should also be careful with sending personal information, including payroll or other financial information, via an email or website. (1,2)

2. Phone scams

Each year, criminals call taxpayers and allege that said taxpayers owe money to the I.R.S. The Treasury Inspector General for Tax Administration says that over the last five years, 12,000 victims have been identified, resulting in a cumulative loss of more than $63 million. Visual tricks can lend authenticity to the ruse: the caller ID may show a toll-free number. The caller may mention a phony I.R.S. employee badge number. New spins are constantly emerging, including threats of arrest, and even deportation. (1,2)

3. Identity theft

The I.R.S. warns that identity theft is a constant concern, but not just online. Thieves can steal your mail or rifle through your trash. While the I.R.S. has made headway in terms of identifying such scams when related to tax returns, and plays an active role in identifying lawbreakers, the best defense that remains is caution when your identity and information are concerned. (1,2)

4. Return preparer fraud

Almost 60% of American taxpayers use a professional tax preparer. Unfortunately, among the many honest professionals, there are also some con artists out there who aim to rip off personal information and grab phantom refunds, so be careful when making a selection. (1,2)

5. Fake charities

Some taxpayers claim that they are gathering funds for hurricane victims, an overseas relief effort, an outreach ministry, and so on. Be on the lookout for organizations that are using phony names to appear as legitimate charities. A specious charity may ask you for cash donations and/or your Social Security Number and banking information before offering a receipt. (1,2)

6. Inflated refund claims

In this scenario, the scammers do prepare and file 1040s, but they charge big fees up front or claim an exorbitant portion of your refund. The I.R.S. specifically warns against signing a blank return as well as preparers who charge based on the amount of your tax refund. (1,2)

7. Excessive claims for business credits

In their findings, the I.R.S. specifically notes abuses of the fuel tax credit and research credit. If you or your tax preparer claim these credits without meeting the correct requirements, you could be in for a nasty penalty. (1,2)

8. Falsely padding deductions on returns

Some taxpayers exaggerate or falsify deductions and expenses in pursuit of the Earned Income Tax Credit, the Child Tax Credit, and other federal tax perks. Resist the temptation to pad the numbers and avoid working with scammers who pressure you to do the same. (1,2)

9. Falsifying income to claim credits

Some credits, like the Earned Income Tax Credit, are reported by scammers claiming false income. You are responsible for what appears on your return, so a boosted income can lead to big penalties, interest, and back taxes. (1,2)

10. Frivolous tax arguments

There are seminar speakers and books claiming that federal taxes are illegal and unconstitutional and that Americans only have an implied obligation to pay them. These and other arguments crop up occasionally when people owe back taxes, and at present, they carry little weight in the courts and before the I.R.S. There’s also a $5,000 penalty for filing a frivolous tax return, so these fantasies are best ignored. (1,2)

11. Abusive tax shelters

If it sounds too good to be true, it usually is, and that’s especially true of complicated tax avoidance schemes, which attempt to hide assets through a web of pass-through companies. The I.R.S. suggests that a second opinion from another financial professional might help you avoid making a big mistake. (1,2)

12. Offshore tax avoidance

Not all taxpayers adequately report offshore income, and if you don’t, you are a lawbreaker, according to the I.R.S. You could be prosecuted or contend with fines and penalties. (1,2)

Watch out for these ploys – ultimately, you are the first defense against a scam that could cause you to run afoul of tax law.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The impact of a potential new President on stock market returns is always a key question in the weeks prior to a general election. It’s important to keep in mind that, despite frequent worries around this time of year, and that financial markets may react in the shorter-term term to poll results and election outcomes (especially surprises), the longer-term effects of any administration’s policies appear to be disconnected from financial market results. Instead, stocks especially tend to follow earnings, which follow economic growth trends. Nevertheless, there are always policy distinctions that could affect various industries to some extent.

In contrast to election season norms in prior decades, polarization between the two parties has become more pronounced, with more extreme positions on both sides forcing candidates away from traditional ‘centrist’ policy often adopted during general election campaigns. A Biden victory has the potential of moving policy toward a more progressive stance, although this is not as simple of a story as in past years, with the current administration having taken a variety of unconventional stances in its own right.

The potential retaking of the Senate by Democrats, in addition to their already holding power in the House, would heighten the risk of more progressive policies being voted in—with minimal opposition. On the other hand, Republicans successfully retaining the Senate would continue to act as an effective counterbalance against legislation from the House, potentially resulting in a policy log jam for the next four years. (Some see this as a best-case scenario, although doing little to alleviate the high current levels of political disagreement.)

The following represent a few areas that could be most impacted by a new Democratic administration, through either new legislation, reversals of prior policies, or no change:

Taxes

It is assumed that the corporate and personal tax cuts put into place in the current regime could be reversed—partially or fully—towards prior levels. Personal income tax policy rhetoric during the campaign has been aimed at the ultra-wealthy, but with high budget deficits and an unprecedented level of fiscal debt, higher tax rates for even middle-income Americans have been feared. This includes higher capital gains tax rates, seen as benefitting the wealthy the most, as they own the majority of financial assets. ‘Wealth taxes’ based on assets are out there as a wildcard as well (although targeted at billionaires). Even if corporate rates do not return to prior max levels of 35%, they are likely not to remain at 21%, either. Most directly, higher tax rates for companies directly erode multi-year earnings projections, which could result in lower stock valuation assessments.

Environment

This multi-faceted policy area includes not only ‘green’ legislation (likely to be promoted by a Biden administration), but also important carryover effects related to the energy industry broadly. It would likely be unfavorable for traditional petroleum- and coal-based energy production (and emissions), including limitations for drilling, and increased regulation of impacts. Conversely, alternative energy sources would likely be promoted—including wind and solar—as well as the potential taxation of carbon emissions.

U.S.-China Relations and Trade

This is a more challenging policy point, as both parties have adopted a hard line on China—for a variety of different reasons. The current administration has taken a more confrontational approach. This has been unique relative to prior regimes, which, at least at the surface, had attempted to avoid outright hostile language and direct economic sanctions. While the two parties agree in principle for a tougher stance, Republicans have focused this effort on corporate intellectual property, while Democrats have also included human rights concerns; specifically, based on the treatment of several ethnic and religious minority groups within the country. This remains a wildcard to some degree, but the majority of Americans and politicians now favor a tougher stance toward China—a rare point of policy agreement.

Antitrust Legislation

This wouldn’t normally surface as a key policy platform, but the rise of several technology behemoths has raised questions over the competitive environment and growing economic power of these firms. In prior decades, pro-business conservative politicians have been more reluctant to attack oligopolistic entities, while populist/progressive movements had been responsible for breaking up dominant ‘Robber Baron’ firms—such as Rockefeller’s Standard Oil in the early 1900’s. In recent years, though, the more progressively-minded tech giants have been supportive of the Democratic agenda and drawing the ire of Republicans—creating a role reversal. The pressure on these firms may continue to some degree, depending on who’s in charge. Some of this oligopolistic power is due to the structures of the industries. They’ve remained among the most fundamentally solid from a financial standpoint during the pandemic, which has rewarded investors. Of course, many small businesses have not fared nearly as well, fanning the flames of resentment.

Workers

Republican policies over the years have generally been focused on letting ‘laissez faire’ (free market) forces determine market competition and pricing dynamics—favored by many mainstream economists. Biden policies would likely offer more worker-friendly populist concessions, such as a higher minimum wage, better health coverage, paid leave, student loan relief, etc. On one hand, additional benefits and pay cut into company profit margins. On the other hand, more money in the pockets of consumers could be a catalyst for broader personal spending and consumption growth broadly, which benefits the broader economy in its own way.

Healthcare

The formation of the Affordable Care Act (‘Obamacare’) was followed by an immediate battle for repeal by Republicans and expansion by Democrats. This fight is likely to continue, with any enhancements in coverage (like ‘Medicare For All’) or other changes aimed at high prescription drug prices (also favored by the current administration, despite potential impact on corporate profits). Some pharmaceutical firms have acted to pre-emptively curb pricing for some drugs in efforts to stem the criticism and potentially unfavorable legislation. These firms counter that such high prices act as the funding mechanism for continued research and development on new therapeutics, which many politicians have accepted. The convoluted health care system, though, continues to overwhelm attempts at reform, which has led to a lower financial market probability for radical change in the near-term.

Defense

In prior years, a strong defense budget and global projection of power has been a Republican party tenet. Lately, this has taken a bit of an opposite turn with conservatives moving more towards a stance of isolation, and progressives seeking to maintain greater globalism. This may be an area with little net change, absent geopolitical surprises (which can be counted on).

Immigration

This doesn’t seem like a market-related topic at first glance, but movement of people across borders affects demographics, which, in turn, affects the size of the labor force and productivity—and ultimately economic growth. This has been a divisive issue throughout America’s history, and each side currently has a mixed relationship with it. Generally, economists argue that a more lenient immigration policy provides a larger pool of workers, which results in not only higher production but also higher consumption. Companies have often silently been in favor of these less restrictive policies, which brings in a higher supply of workers, which lowers wages and boosts profits. On the other side, and often in conflict with other elements of the party, Democratic politicians have tended to have strong support from unionized U.S. workers, which often oppose globalism and foreign worker competition—in efforts to retain jobs and sustain higher wages domestically. Realistically, on net, there could be few extreme changes due to these continual conflicts.

Fiscal Policy

In decades of old, Republicans were seen as the fiscally spendthrift party, while Democrats were cast in debates as ‘tax-and-spend.’ But even prior to the Covid recession, these traditional labels were less applicable, with higher spending proposed on all sides. Due to economic woes from the pandemic likely carrying over into 2021, and perhaps 2022, as well as increasing acceptance of policies such as Modern Monetary Theory (MMT), it appears the accepted spending may continue regardless of the party in office. However, at the fringes, Democrats have proposed more direct relief to workers, and Republicans to small businesses, in keeping with other distinct policy preferences.

Monetary Policy

This should be unaffected by politics, and largely has been over the years. Of course, there have been notable and theatrical exceptions, such as the Fed Chair being physically bullied at LBJ’s Texas ranch in the 1960’s, and the current President’s urging of low rates via social media. A Biden presidency could likely feature more restraint, and a conventional ‘hands off’ approach. However, the Fed could be increasingly impacted by the large Federal deficit and rising debt load, which affects both interest payment obligations as well as credit rating—which affect rates outside of the Fed’s control.

In short, by looking at individual industries, the outlook may not appear to change that much, aside from policy preferences one way or another. The key differences relate to tax policy, the broader regulatory environment, and fiscal spending policies.

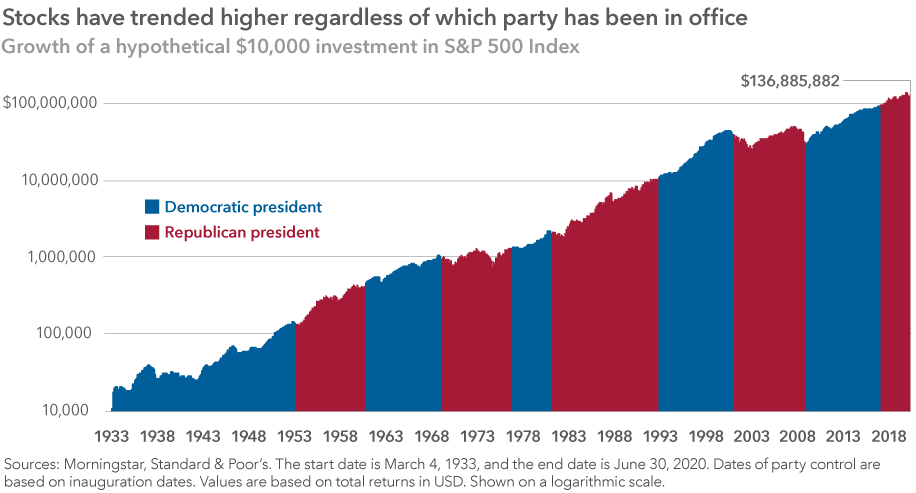

It’s important to remember that an elected President has very little effect on market results, historically. In fact, some of the stronger periods of market performance have been under Democratic administrations, contrary to popular assumption. (1)

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

In many ways,policies to expect would likely be similar to what’s in place today, and largely opposite of those proposed under a Biden administration.At the same time, Trump’s policies have not followed ‘traditional’ Republican ideologies from decades past in a variety of areas. The Senate Republicans have been far more predictable from a policy standpoint, as have the Congressional Democrats.

The practical factor for the election continues to be whether or not the Democrats are able to take the Senate from the Republicans, which, in addition to holding the House, would allow for the ability to push through a greater volume of progressive legislation. A split-party legislative and/or administrative branch could result in four years of gridlock, with little net change in policy. (That might be perceived as the ‘worst case’ or ‘best case’ depending on the observer.)

Little may change from a higher-level view if the first Trump term morphs into a second. But, it’s important to rememberfrom a financial markets perspective that the President in power has been relatively unimportant in driving longer-term sentiment and returns. Attempting to time election results or moving out of markets to avoid volatility can result in sub-optimal results, even though the weeks prior to an election can become more volatile. Interestingly, in the cases where an incumbent is seeking re-election, one of the few consistent tendencies over the past century is based on U.S. stock market results in the three months prior to Election Day. Based on the S&P 500, a positive return for that stretch has proven favorable for an incumbent’s chances, while a negative return has favored the challenger. (For perspective’s sake, from the window starting Aug. 3, the market is up 0.75% through Fri., Sept. 18—with several more weeks to go until Nov. 3.)

That said, while politics can coincide with day-to-day financial market movements at times, the two rarely correlate meaningfully over the long haul. The chart below bears this out fairly dramatically:

The following policy items assume that a Trump reelection is accompanied by Republicans retaining the Senate, which creates a ‘status quo’ situation. A newly Democratic senate majority would create more of a wildcard:

Taxes

It is probably safe to assume the tax cuts from 2017 would remain in place. These have served to benefit corporations, which receive an immediate boost to the bottom line, resulting in higher reported earnings. Consequently, this models out to higher multi-year growth and justifies higher equity valuations. Personal income tax rates would likely also remain low, along with capital gains rates. Traditional supply-side economists argue that stronger corporate performance and fewer hurdles (such as regulation and taxes) result in a larger ‘pot’ for everyone. However, this assumes that wealth trickles down proportionately to all workers, which has been debated in recent years as income equality between different groups has widened.

Environment

This would also be assumed to be status quo, which includes minimal promotion of green technologies. It would likely be coupled with a pushback on more stringent standards, such as those adopted by California (whose standards predate the EPA and are often stricter). While the energy sector has been struggling with low petroleum prices, due to weaker demand due to the pandemic, current policies would keep additional regulatory headwinds at bay. However, energy firms have been hurt far more by weaker demand from the pandemic than by other factors. U.S.-China relations and trade. The geopolitical tension with China has been steadily growing, and a status quo result would assume more of the same. It’s been claimed by some China experts that the country is currently just playing a ‘waiting game’—for the Trump administration to eventually end, and to instead deal with the successor. As part of their 50- and 100-year national plans, such a delay is seen as just a temporary roadblock. The important component is that a tough U.S. stance on China has support across the aisle—it’s one of the few policy items both parties agree on. So, a longer-term decoupling is likely, although the public stances and negotiation styles could differ between administrations.

Antitrust Legislation

In years past, some Democratic platforms have been seen as anti-corporate (and conversely, pro-worker). This would have translated to a crackdown on large ‘oligopolies’ and a reining in of corporate power in the economy and society. In the current case, argued by some due to the more progressive political leanings of large tech companies, Democrats have appeared less interested in breaking up these firms. Republicans have certainly appeared more interested. Since it’s not quite clear where any ‘abuses’ lie and how consumers are adversely affected (many argue they’ve benefited greatly through both product variety and cost), this issue remains complex and path unclear.

Workers

In line with trends seen globally, not just in the U.S., both parties have taken on a more populist tone in recent years, largely in keeping with the larger societal income gaps. The polarization has taken place far more on the political side than the socioeconomic side, as all parties want to be seen as ‘pro-working class.’ This creates a conundrum, although no clear evolution in policy. Continued trade restrictions may help U.S. firms in the near term, although it’s not clear that benefits trickle down to workers longer-term and could hurt consumers through higher prices. Contrary to the Biden agenda, a second Trump administration would make more progressive items, such as a higher minimum wage and other benefits less likely—although these also depend on the Congressional makeup.

Healthcare

A Trump administration would likely continue to fight ‘Obamacare,’ and continue support for the current private insurance-based healthcare model. Despite the battles over universal coverage/single-payer format, there remains no constructed alternative to the current system for legislators to gravitate to. However, there is bi-partisan populist support for better regulation of high pharmaceutical prices and plugging some gaps to help reduce medical care costs for seniors. The industry has fought back on pharma prices, arguing that profits feed back into research and development for important new therapies, so this has largely resulted in a stalemate in recent years.

Defense

A traditional Republican policy platform has been a strong defense base. This is thought likely to persist, although the Trump administration has focused on far less global interventionism. This hasn’t manifested completely, but could continue to play a role in broader policy thinking. At the same time, China has been viewed as an increasing global military threat, which would necessitate further spending. The trend has been moving from conventional military spending towards new technologies, such as cyberwarfare, satellites, drones, etc.—all of which are technologically complex and expensive.

Immigration

The border ‘wall’ has largely been symbolic, as the Trump administration has clamped down on immigration mostly through policy, which would seem likely to continue in a second term. This has provided a seeming veil of protection for U.S. workers (championed by both candidates in different ways), but economists, who view labor in a global context, see increased restrictions of any kind as a hurdle to stronger economic performance. This is a complex issue, with outcomes the result of multi-decade trends, so the policy action of a single President may only provide a short-term impact on GDP growth. Demographics and business/worker competitiveness play a far more important role, with job training and education enhancements acting as a behind-the-scenes policy championed by many but not discussed as much by candidates in terms of specific plans.

Less stringent regulatory environment.

The President promised to rollback regulations imposed over the past administration, including the expanded use of executive orders, and that has certainly occurred. It’s likely another four years would continue regulation downsizing, in a generally pro-business way, including financial markets and their oversight.

Fiscal policy

The old stereotypes have been cast aside, as parties on both sides are in a spending mode. Republicans are a bit less in favor of direct stimulus to workers (at least in the same large amounts Democrats have been), and more in favor of corporate injections. During the pandemic, airlines and the travel industry have been lobbying especially hard for more aid. This pandemic will end up being expensive regardless of who ends up in the White House, with debt ramifications far beyond the next four years. Monetary policy. As noted earlier, a central bank should be agnostic to political pressures, but that has been easier said than done. Pressure to lower rates or keep policy as ‘easy’ as possible is preferred, since it coincides with keeping the economy growing—which most administrations prefer under their watch. The U.S. Fed has sidestepped such pressure far better than in some countries, of course, but a continuation of the current administration and ‘tweeting’ about central bank decisions runs the risk of negatively influencing public opinion about the Fed and its functions. Politics can also appear in the nomination of certain new board members, such as the controversial Judy Shelton (who has favored revisiting the gold standard—a position rejected by many mainstream economists). Regardless, the Fed has continued to stay out of the political fray over the decades, despite a variety of administrations holding opposing views.

Judicial branch

The Supreme Court is typically not a top concern of financial markets, but with the passing of Justice Ruth Bader Ginsburg, a position on the bench has opened. Any new appointee’s political leanings can tilt the balance of key decisions toward either the conservative or progressive end of the spectrum. So, this can have ramifications for decisions involving business, regulations, or any other economically-relevant area.

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

Recently, the $2 trillion “Coronavirus Aid, Relief, and Economic Security” (“CARES”) Act was signed into law. The CARES Act is designed to help those most impacted by the COVID-19 pandemic, while also providing key provisions that may benefit retirees. (1)

To put this monumental legislation in perspective, Congress earmarked $800 billion for the Economic Stimulus Act of 2008 during the financial crisis. (1)

The CARES Act has far-reaching implications for many. Here are the most important provisions to keep in mind:

Stimulus Check Details

Americans can expect a one-time direct payment of up to $1,200 for individuals (or $2,400 for married couples) with an additional $500 per child under age 17. These payments are based on the 2019 tax returns for those who have filed them and 2018 information if they have not. The amount is reduced if an individual makes more than $75,000 or a couple makes more than $150,000. Those who make more than $99,000 as an individual (or $198,000 as a couple) will not receive a payment. (1)

Business Owner Relief

The act also allocates $500 billion for loans, loan guarantees, or investments to businesses, states, and municipalities. (1)

Your Inherited 401(k)s

People who have inherited 401(k)s or Individual Retirement Accounts can suspend distributions in 2020. Required distributions don’t apply to people with Roth IRAs; although, they do apply to investors who inherit Roth accounts. (2)

RMDs Suspended

The CARES Act suspends the minimum required distributions most people must take from 401(k)s and IRAs in 2020. In 2009, Congress passed a similar rule, which gave retirees some flexibility when considering distributions. (2,3)

Withdrawal Penalties

Account owners can take a distribution of up to $100,000 from their retirement plan or IRA in 2020, without the 10-percent early withdrawal penalty that normally applies to money taken out before age 59½. But remember, you still owe the tax. (4)

Many businesses and individuals are struggling with the realities that COVID-19 has brought to our communities. The CARES Act, however, may provide some much-needed relief. Contact your financial professional today to see if these special 2020 distribution rules are appropriate for your situation.

Sources

CNBC.com, March 25, 2020.

The Wall Street Journal, March 25, 2020.

The Wall Street Journal, March 25, 2020.

The Wall Street Journal, March 25, 2020.

This material was prepared by MarketingPro, Inc., and does notnecessarilyrepresent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Under the CARES act, an accountholder who already took a 2020 distribution has up to 60 days to return the distribution without owing taxes on it. This material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Under the SECURE Act, your required minimum distribution (RMD) must be distributed by the end of the 10th calendar year following the year of the Individual Retirement Account (IRA) owner’s death. Penalties may occur for missed RMDs. Any RMDs due for the original owner must be taken by their deadlines to avoid penalties. A surviving spouse of the IRA owner, disabled or chronically ill individuals, individuals who are not more than 10 years younger than the IRA owner, and children of the IRA owner who have not reached the age of majority may have other minimum distribution requirements.

Under the CARES act, an accountholder who already took a 2020 distribution has up to 60 days to return the distribution without owing taxes on it. This material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Under the SECURE Act, in most circumstances, once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA). Withdrawals from Traditional IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. You may continue to contribute to a Traditional IRA past age 70½ under the SECURE Act, as long as you meet the earned-income requirement.

Account holders can always withdraw more. But if they take less than the minimum required, they could be subject to a 50% penalty on the amount they should have withdrawn – except for 2020.

Financially, many of us associate April with taxes – but we should also associate April with important IRA deadlines.

April 1, 2020

The deadlineto take your Required Minimum Distribution (RMD) from certain individual retirement accounts.

A New Federal Law

The Setting Every Community Up for Retirement Enhancement (SECURE) ACT, passed late in 2019, changed the age for the initial RMD for traditional IRAs and traditional workplace retirement plans. It lifted this age from 70½ to 72, effective as of 2020.1

So, if you were not 70½ or older when 2019 ended, you can wait to take your first RMD until age 72. If you were 70½ at the end of 2019, the old rules still apply, and your initial RMD deadline is April 1, 2020. Your second RMD will be due on December 31, 2020.1,2

Keep in mind that withdrawals from traditional, SIMPLE, and SEP-IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty.

To qualify for the tax-free and penalty-free withdrawal of earnings from a Roth IRA, your Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances, such as a result of the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

April 15, 2020

The deadline for making annual contributions to a traditional IRA, Roth IRA, and certain other retirement accounts. (3)

The earlier you make your annual IRA contribution, the better. You can make a yearly IRA contribution any time between January 1 of the current year and April 15 of the next year. So, the contribution window for 2019 started on January 1, 2019 and ends on April 15, 2020. Accordingly, you can make your IRA contribution for 2020 any time from January 1, 2020 to April 15, 2021. (4)

You may help manage your income tax bill if you are eligible to contribute to a traditional IRA. To get the full tax deduction for your 2019 traditional IRA contribution, you have to meet one or more of these financial conditions:

You aren’t eligible to participate in a workplace retirement plan.

You are eligible to participate in a workplace retirement plan, but you are a single filer or head of household with Modified Adjusted Gross Income (MAGI) of $64,000 or less. (Or if you file jointly with your spouse, your combined MAGI is $103,000 or less.) (5)

You aren’t eligible to participate in a workplace retirement plan, but your spouse is eligible and your combined 2019 gross income is $193,000 or less. (6)

Thanks to the SECURE Act, both traditional and Roth IRA owners now have the chance to contribute to their IRAs as long as they have taxable compensation (and in the case of Roth IRAs, MAGI below a certain level; see below). (1,4)

If you are making a 2019 IRA contribution in early 2020, you must tell the investment company hosting the IRA account which year the contribution is for. If you fail to indicate the tax year that the contribution applies to, the custodian firm may make a default assumption that the contribution is for the current year (and note exactly that to the I.R.S.).

So, write “2020 IRA contribution” or “2019 IRA contribution,” as applicable, in the memo area of your check, plainly and simply. Be sure to write your account number on the check. If you make your contribution electronically, double-check that these details are communicated.

How Much Can You Put Into an IRA This Year?

You can contribute up to $6,000 to a Roth or traditional IRA for the 2020 tax year; $7,000, if you will be 50 or older this year. (The same applies for the 2019 tax year). Should you make an IRA contribution exceeding these limits, you have until the following April 15 to correct the contribution with the help of an I.R.S. form. If you don’t, the amount of the excess contribution will be taxed at 6% each year the correction is avoided.3,4

The maximum contribution to a Roth IRA may be reduced because of Modified Adjusted Gross Income (MAGI) phaseouts, which kick in as follows.

2019 Tax Year

Single/head of household: $122,000 – $137,000

Married filing jointly: $193,000 – $203,000 (7)

2020 Tax Year

Single/head of household: $124,000 – $139,000

Married filing jointly: $196,000 – $206,000 (8)

The I.R.S. has other rules for other income brackets. If your MAGI falls within the applicable phase-out range, you may be eligible to make a partial contribution. (7,8)

A last reminder for those who turned 70½ in 2019: you need to take your first traditional IRA RMD by April 1, 2020 at the latest. The investment company that serves as custodian (host) of your IRA should have alerted you to this deadline; in fact, they have probably calculated the RMD amount for you. Your subsequent RMD deadlines will all fall on December 31. (2)

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Here are some things you might consider before saying goodbye to 2019.

What has changed for you in 2019?

Did you start a new job or leave a job behind?Did you retire? Did you start a family? If notable changes occurred in your personal or professional life, then you will want to review your finances before this year ends and 2020 begins.

Even if your 2019 has been relatively uneventful, the end of the year is still a good time to get cracking and see where you can manage your take bill and/or build a little more wealth.

Keep in mind this article is for informational purposes only and is not a replacement for real-life advice. Please consult your tax, legal, and accounting professionals before modifying your tax strategy.

Do you practice tax-loss harvesting?

That is the art of taking capital losses (selling securities worth less than what you first paid for them) to offset your short-term capital gains. You might want to consider this move, which may lower your taxable income. It should be made with the guidance of a financial professional you trust. (1)

In fact, you could even take it a step further. Consider that up to $3,000 of capital losses in excess of capital gains can be deducted from ordinary income, and any remaining capital losses above that can be carried forward to offset capital gains in upcoming years. When you live in a high-tax state, this is one way to defer tax. (1)

Do you want to itemize deductions?

You may just want to take the standard deduction for 2019, which has ballooned to $12,000 for single filers and $24,000 for joint filers because of the Tax Cuts & Jobs Act. If you do think it might be better for you to itemize, now would be a good time to get receipts and assorted paperwork together. While many miscellaneous deductions have disappeared, some key deductions are still around: the state and local tax (SALT) deduction, now capped at $10,000; the mortgage interest deduction; the deduction for charitable contributions, which now has a higher limit of 60% of adjusted gross income; and the medical expense deduction. (2,3)

Could you ramp up 401(k) or 403(b) contributions?

Contribution to these retirement plans may lower your yearly gross income. If you lower your gross income enough, you might be able to qualify for other tax credits or breaks available to those under certain income limits. Note that contributions to Roth 401(k)s and Roth 403(b)s are made with after-tax rather than pretax dollars, so contributions to those accounts are not deductible and will not lower your taxable income for the year. (4,5)

Are you thinking of gifting?

How about donating to a qualified charity or nonprofit organization before 2019 ends? Your gift may qualify as a tax deduction. You must itemize deductions using Schedule A to claim a deduction for a charitable gift. (4,5)

While we’re on the topic of estate strategy, why not take a moment to review your beneficiary designations? If you haven’t reviewed them for a decade or more (which is all too common), double-check to see that these assets will go where you want them to go, should you pass away. Lastly, look at your will to see that it remains valid and up to date.

Can you take advantage of the American Opportunity Tax Credit?

The AOTC allows individuals whose modified adjusted gross income is $80,000 or less (and joint filers with MAGI of $160,000 or less) a chance to claim a credit of up to $2,500 for qualified college expenses. Phaseouts kick in above those MAGI levels. (6)

See that you have withheld the right amount.

If you discover that you have withheld too little on your W-4 form so far, you may need to adjust your withholding before the year ends.

What can you do before ringing in the New Year?

Talk with a financial or tax professional now rather than in February or March. Little year-end moves might help you improve your short-term and long-term financial situation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Here are some things you might want to do before saying goodbye to 2018.

What has changed for you in 2018?

Did you start a new job or leave a job behind? Did you retire? Did you start a family? If notable changes occurred in your personal or professional life, then you will want to review your finances before this year ends and 2019 begins.

Even if your 2018 has been relatively uneventful, the end of the year is still a good time to get cracking and see where you can plan to save some taxes and/or build a little more wealth.

Do you practice tax-loss harvesting?

That is the art of taking capital losses (selling securities worth less than what you first paid for them) to offset your short-term capital gains. If you fall into one of the upper tax brackets, you might want to consider this move, which directly lowers your taxable income. It should be made with the guidance of a financial professional you trust. (1)

In fact, you could even take it a step further. Consider that up to $3,000 of capital losses in excess of capital gains can be deducted from ordinary income, and any remaining capital losses above that can be carried forward to offset capital gains in upcoming years. When you live in a high-tax state, this is one way to defer tax. (1_

Do you want to itemize deductions?

You may just want to take the standard deduction for 2018, which has ballooned to $12,000 for single filers and $24,000 for joint filers because of the Tax Cuts & Jobs Act. If you do think it might be better for you to itemize, now would be a good time to get the receipts and assorted paperwork together. While many miscellaneous deductions have disappeared, some key deductions are still around: the state and local tax (SALT) deduction, now capped at $10,000; the mortgage interest deduction; the deduction for charitable contributions, which now has a higher limit of 60% of adjusted gross income; and the medical expense deduction. (2,3)

Could you ramp up 401(k) or 403(b) contributions?

Contribution to these retirement plans lower your yearly gross income. If you lower your gross income enough, you might be able to qualify for other tax credits or breaks available to those under certain income limits. Note that contributions to Roth 401(k)s and Roth 403(b)s are made with after-tax rather than pre-tax dollars, so contributions to those accounts are not deductible and will not lower your taxable income for the year. They will, however, help to strengthen your retirement savings. (4)

Are you thinking of gifting?

How about donating to a qualified charity or non-profit organization before 2018 ends? In most cases, these gifts are partly tax deductible. You must itemize deductions using Schedule A to claim a deduction for a charitable gift.5

If you donate publicly traded shares you have owned for at least a year, you can take a charitable deduction for their fair market value and forgo the capital gains tax hit that would result from their sale. If you pour some money into a 529 college savings plan on behalf of a child in 2018, you may be able to claim a full or partial state income tax deduction (depending on the state).2,6

Of course, you can also reduce the value of your taxable estate with a gift or two. The federal gift tax exclusion is $15,000 for 2018. So, as an individual, you can gift up to $15,000 to as many people as you wish this year. A married couple can gift up to $30,000 in 2018 to as many people as they desire.7

While we’re on the topic of estate planning, why not take a moment to review the beneficiary designations for your IRA, your life insurance policy, and workplace retirement plan? If you haven’t reviewed them for a decade or more (which is all too common), double-check to see that these assets will go where you want them to go, should you pass away. Lastly, look at your will to see that it remains valid and up-to-date.

Should you convert all or part of a traditional IRA into a Roth IRA?

You will be withdrawing money from that traditional IRA someday, and those withdrawals will equal taxable income. Withdrawals from a Roth IRA you own are not taxed during your lifetime, assuming you follow the rules. Translation: tax savings tomorrow. Before you go Roth, you do need to make sure you have the money to pay taxes on the conversion amount. A Roth IRA conversion can no longer be recharacterized (reversed). (8)

Can you take advantage of the American Opportunity Tax Credit?

The AOTC allows individuals whose modified adjusted gross income is $80,000 or less (and joint filers with MAGI of $160,000 or less) a chance to claim a credit of up to $2,500 for qualified college expenses. Phase-outs kick in above those MAGI levels.9

See that you have withheld the right amount. The Tax Cuts & Jobs Act lowered federal income tax rates and altered withholding tables. If you discover that you have withheld too little on your W-4 form so far in 2018, you may need to adjust your withholding before the year ends. The Government Accountability Office projects that 21% of taxpayers are withholding less than they should in 2018. Even an end-of-year adjustment has the potential to save you some tax.10

What can you do before ringing in the New Year? Talk with a financial or tax professional now rather than in February or March. Little year-end moves might help you improve your short-term and long-term financial situation.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Book a FREE 15 minute, no commitment, phone call with me to discuss your financial situation and see if I can help. Pick a date & time that works for you!

visit weiss-financial.com to learn about our retirement planning & investment services.

Blog Topics:

What I’m Reading

Disclosure

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.