Not long ago, I sat down with someone who hadn’t looked at their retirement plan in years. Nothing was “wrong,” exactly—their accounts were fine, and markets had done what markets do. But life had changed. They had moved, one spouse had scaled back work, and a grandchild was now part of the picture. Their priorities were simply different.

That’s the part that often gets missed. A retirement plan isn’t just about numbers—it’s about your life. And life doesn’t stay still.

Over the years, I’ve found that most plan updates aren’t triggered by the market. They usually come from real-life moments, like:

A job change or decision to retire

A move (across the country or just across town)

Changes in family—marriage, grandchildren, or caregiving

Health changes

Receiving an inheritance or paying off a mortgage

Sometimes those changes are positive, sometimes they’re not—but either way, they’re worth revisiting your plan.

There are also quieter shifts that don’t show up on a statement, but still matter. People start asking:

Do I really want to wait this long to retire?

Should we be enjoying this money more now?

What do we want this to do for our family?

Those aren’t spreadsheet questions—they’re life questions. And a good plan should evolve with them.

In many cases, nothing dramatic needs to change. But reviewing your plan—after a life event or even just every year or two—can help keep everything aligned and intentional.

Because the goal isn’t just to have a plan. It’s to have one that still fits the life you’re actually living.

This is a personal blog about retirement planning, investing, and the financial decisions that come with life’s transitions.

I write for pre-retirees and retirees who want to make thoughtful decisions about their money and gain clarity about where they’re headed.

Most of what I share isn’t about predicting markets or chasing returns. It’s about thinking clearly, avoiding common mistakes, and and working toward long-term progress over time.

Look beyond this moment and stay focused on your long-term objectives.

Volatility will always be around on Wall Street, and as you invest for the long term, you must learn to tolerate it. Rocky moments, fortunately, are not the norm.

Since the end of World War II, there have been dozens of Wall Street shocks.

Wall Street has seen 56 pullbacks (retreats of 5-9.99%) in the past 73 years; the S&P index dipped 6.9% in this last one. On average, the benchmark fully rebounded from these pullbacks within two months. The S&P has also seen 22 corrections (descents of 10-19.99%) and 12 bear markets (falls of 20% or more) in the post-WWII era. (1)

Even with all those setbacks, the S&P has grown exponentially larger. During the month World War II ended (September 1945), its closing price hovered around 16. At this writing, it is above 2,750. Those two numbers communicate the value of staying invested for the long run. (2)

This current bull market has witnessed five corrections, and nearly a sixth (a 9.8% pullback in 2011, a year that also saw a 19.4% correction). It has risen roughly 335% since its beginning even with those stumbles. Investors who stayed in equities through those downturns watched the major indices soar to all-time highs. (1)

As all this history shows, waiting out the shocks may be highly worthwhile.

The alternative is trying to time the market. That can be a fool’s errand. To succeed at market timing, investors have to be right twice, which is a tall order. Instead of selling in response to paper losses, perhaps they should respond to the fear of missing out on great gains during a recovery and hang on through the choppiness.

After all, volatility creates buying opportunities. Shares of quality companies are suddenly available at a discount. Investors effectively pay a lower average cost per share to obtain them.

Bad market days shock us because they are uncommon.

If pullbacks or corrections occurred regularly, they would discourage many of us from investing in equities; we would look elsewhere to try and build wealth. A decade ago, in the middle of the terrible 2007-09 bear market, some investors convinced themselves that bad days were becoming the new normal. History proved them wrong.

As you ride out this current outbreak of volatility, keep two things in mind.

One, your time horizon. You are investing for goals that may be five, ten, twenty, or thirty years in the future. One bad market week, month, or year is but a blip on that timeline and is unlikely to have a severe impact on your long-run asset accumulation strategy. Two, remember that there have been more good days on Wall Street than bad ones. The S&P 500 rose in 53.7% of its trading sessions during the years 1950-2017, and it advanced in 68 of the 92 years ending in 2017. (3,4)

Sudden volatility should not lead you to exit the market.

If you react anxiously and move out of equities in response to short-term downturns, you may impede your progress toward your long-term goals.

▲ Time, diversification and the volatility of returns

This chart shows historical returns by holding period for stocks, bonds and a 50/50 portfolio, rebalanced annually, over different time horizons. The bars show the highest and lowest return that you could have gotten during each of the time periods (1-year, 5-year rolling, 10-year rolling and 20-year rolling). This page advocates for simple balanced portfolio, as well as for having an appropriate time horizon.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Preparing for retirement just got a little more financial wiggle room. The Internal Revenue Service (IRS) announced new contribution limits for 2022.

401(k) & 403(b)

For workplace retirement accounts (i.e. 401(k), 403(b), amongst others), the contribution limit rises $1,000 to $20,500. Catch-up contributions remain at $6,500. (1)

Traditional IRA

Staying put for 2022 are traditional Individual Retirement Accounts (IRAs), with the limit remaining at $6,000. The catch-up contribution for traditional IRAs remains $1,000 as well. (1)

Roth IRA

Eligibility for Roth IRA contributions has increased, as well. These have bumped up to $129,000 to $144,000 for single filers and heads of households, and $204,000 to $214,000 for those filing jointly as married couples. (1)

SIMPLE IRA

Another increase was for SIMPLE IRA Plans (SIMPLE is an acronym for Savings Incentive Match Plan for Employees), which increases from $13,500 to $14,000. (1)

If these increases apply to your retirement strategy, a financial professional may be able to help make some adjustments to your contributions.

Contribution Limits (3,4)

2022

2021

Change

401(k) & 403(b) maximum employee elective deferral

$20,500

$19,500

+$1,000

401(k)s 403(b), etc. employee catch-up contribution (if age 50 or older by year-end)*

$6,500

$6,500

None

Traditional IRA & Roth IRA

$6,000

$6,000

None

Traditional IRA & Roth IRA catch-up contributions (if age 50 or older by year-end)*

$1.000

$1,000

None

SIMPLE IRA

$14,000

$13,500

+$500

RMDs Explained

Once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA) or Savings Incentive Match Plan for Employees IRA in most circumstances. Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Once you reach age 72, you must begin taking required minimum distributions from your 401(k), 403(b), or other defined-contribution plans in most circumstances. Withdrawals from your 401(k) or other defined-contribution plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

5-Year Holding Period for Roth IRAs

To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Most people worry about not having enough money for retirement. But did you also know that there is such a thing as having too much money? Too much money may not necessarily be a bad thing, but you do need to worry about required minimum distributions (RMDs). Here’s what you need to know about RMDs.

RMDs Depend on Your Age

The main point of RMDs is to keep money from staying tax-free forever. The government gave a temporary tax break to encourage you to save for retirement, but it still wants that tax money. A required minimum distribution is a required withdrawal from your retirement account. It counts in your taxable income just like any other withdrawal in retirement.

Currently, RMDs start when you hit age 72 (or 70½ if you turned 70½ prior to January 1, 2020) and they are calculated to empty your retirement account within your expected life expectancy. (1) Each year, you need to withdraw a certain percentage of your account with the percentage going up as you age. However, it’s important to realize that you do not have to spend all of this money. You can also reinvest it into a taxable account.

Not Taking the RMD Can Mean Big Penalties

Thinking about skipping RMDs to avoid taxes? Think again. Not only do you still have to pay the taxes on the RMD amount, but you’ll also owe a 50 percent penalty.

For example, if you were supposed to withdraw $10,000 but didn’t, the IRS will charge you an extra $5,000. The penalty repeats every year until you catch up on your RMDs from previous years.

RMDs Can Throw a Wrench in Your Tax Planning

There are many reasons why you might want to reduce your taxable income in retirement. These can include qualifying for things like Medicaid subsidies, avoiding taxes on your Social Security benefits, trying to stay in a lower capital gains tax bracket, or just wanting to pay fewer taxes.

Required minimum distributions can throw a major wrench in your tax planning because not only are they not avoidable, they can suddenly increase if the market surges. If you’re using a tax strategy that requires reducing your income to a certain level, it’s important to build in flexibility for your RMDs.

RMDs Can Be Avoided

There are still ways to reduce or even avoid RMDs altogether. The main idea is to get the money out of your retirement account when you want to not when the IRS wants you to.

One method is to make extra withdrawals at the end of the year. In December, you can estimate your taxes for the year. If you still have room in a lower tax bracket or below the income you need to stay under, you can withdraw additional money. When next year’s RMDs are calculated, it will be on a lower account balance.

You can also convert to a Roth IRA instead of taxing the money out of a tax-advantaged account. Roth IRAs don’t have RMDs because the money has already been taxed. When you make the conversion, you pay ordinary income tax rates on the amount you converted. There are no penalties even if you do the conversion before you turn 59 1/2.

This content is developed from sources believed to be providing accurate information, and provided by Twenty Over Ten. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

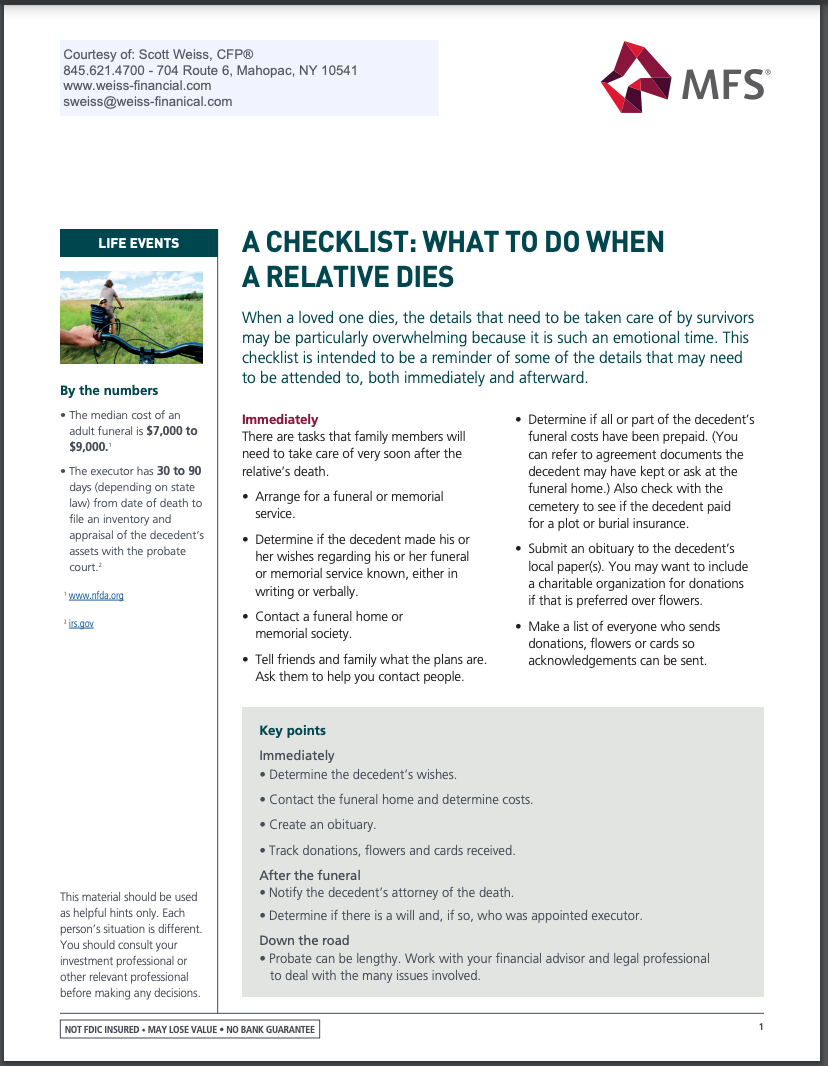

The passing of a loved one irrevocably alters family life. After a death, there is so much to attend to; it is better to do it sooner rather than later. Here, then, is a list of what commonly needs to be looked after.

Request copies of the death certificate.

Depending on where you live, you have two or three places to turn to for this document. You can phone, email, or personally visit the office of the county recorder (or county clerk, as the term may be). Alternately, you can contact your state’s vital records department (sometimes called the state registrar or department of health); it may take a little longer to get the document this way. In addition, some large and mid-sized cities maintain their own registrars of births and deaths.

Call advisors, executors, & business partners as applicable.

The deceased’s lawyer and CPA should be quickly notified along with any business partners and the executor of his or her estate. You must have a say in the decision-making. The tasks of protecting family assets, carrying out your loved one’s bequests, and determining the next steps for a business will follow.

Call your loved one’s current or former employer(s).

Notify them, even if your loved one left the workforce years ago, as retirement savings or pension payments may be involved. As the conversation develops, it is perfectly appropriate to ask about pertinent financial matters – say, 401(k) or 403(b) savings that will be inherited by a beneficiary or what will happen to unused vacation time and/or unpaid bonuses.

Funds amassed in a qualified retirement plan sponsored by an employer (or an IRA, for that matter) commonly go to the primary beneficiary who has been named on the most recent beneficiary form filled out by the account owner. That sounds simple enough – but certain rules and regulations can make things complicated. (1)

As a general rule, if the late 401(k) or 403(b) account owner was your spouse, then you are the presumed beneficiary of the 401(k) or 403(b) assets. Under the Employee Retirement Income Security Act (ERISA), workplace retirement plans are directed to abide by this guideline. If someone else has been named as the primary beneficiary of the account, with your consent, then the assets will go to that person. (2)

If the late 401(k) or 403(b) account owner was single, the assets in the account will go to whomever is designated as the primary beneficiary. The beneficiary designation will override other estate planning documents. (3)

To arrange and confirm the transfer or distribution of such assets, the beneficiary form must be found. If you can’t locate it, the employer and/or the financial firm overseeing the retirement plan should provide access to a copy. The financial firm should ask you to supply:

A certified copy of the account owner’s death certificate

A notarized affidavit of domicile (a document certifying his or her place of residence at the time of death)

If you have been widowed, call Social Security.

If you already receive benefits, you may now be eligible for greater benefits. (4)

If your spouse received Social Security and you did not, you may now qualify for survivor benefits – and you should let Social Security know as soon as possible, as these benefits may be paid out relative to your application date rather than the date of your loved one’s death. (4)

If this is the case, you may apply for survivor benefits by phone or by visiting a Social Security office. You will need to have some extensive paperwork on hand, specifically:

Proof of the death (death certificate, funeral home documentation)

Your late spouse’s Social Security number

His/her most recent W-2 forms or federal self-employment tax return

Your own Social Security number & birth certificate

Social Security numbers & birth certificates of any dependent children

Your marriage certificate, if you have been widowed

The name of your bank & the number of your bank account, for direct deposit purposes

If you have reached full retirement age, you will likely get 100% of the basic benefit amount that your late spouse was receiving. If you are in your sixties, but haven’t yet reached full retirement age, you may receive anywhere from 71% to 99% of that amount. If you have a child younger than 16, you will get 75% of your late spouse’s basic benefit amount and so will your child. (4,5)

Contact the insurance company.

Assuming your loved one had some form of life insurance, contact the policyholder services department of that insurer and confirm the steps for claiming the death benefit. A claim form will have to be filled out, signed, and presented to the insurance company (one for each named adult beneficiary of the policy), and a certified copy of the death certificate must also be sent. If the primary beneficiary of a policy is deceased, the contingent beneficiary can usually claim the death benefit with a claim form, plus the death certificates of the policy owner and the primary beneficiary. Some insurers simply have you submit a form reporting the death of the policyholder first, and then follow up by mailing you forms and instructions for the next steps. (6)

Death benefits are generally paid out within 30 to 60 days of a claim. Presumably, they will be paid out in a lump sum. Some insurers will let a beneficiary receive a payout as a stream of monthly income or in installments. (7)

It isn’t unusual for people to own multiple life insurance policies. The AARP, AAA, and myriad banks and non-profits market group life coverage to members/customers, and mortgage lenders and credit issuers offer forms of life insurance for borrowers. Tracking all this coverage down is the problem, and canceled checks and bank records don’t always provide ready clues. Not surprisingly, websites have appeared that will help you search for life insurance policies, and you may be able to locate policies with the help of your state insurance commissioner’s office. (8)

If the family member was a veteran, call the VA.

Your family may be entitled to funeral and burial benefits. In addition, the Veterans Administration offers Death Pensions and Aid & Attendance and Housebound Pensions to lower-income widows of deceased wartime veterans and their unmarried children. (9)

These pensions are needs based. To be eligible for the Death Pension, a widow or child’s “countable” income must fall below a certain yearly limit set by Congress. (A “child” as old as 22 may be eligible for the Death Pension.) The deceased veteran must not have received a dishonorable discharge, and they must have served 90 or more days of active duty, at least 1 day of it during wartime. If they entered active duty after September 7, 1980, then in most cases, 24 months or more of active duty service are necessary for a Death Pension to eventually be paid. The Aid & Attendance and Housebound Pensions provide some recurring income to pay for licensed home health aide or homemaker services. (9)

It is wise to contact a Veterans Services Officer before you file such a pension claim, as they can be a big help during the process. You can find a VSO through your state veterans’ affairs department or through the VFW, the Order of the Purple Heart, the American Legion, or the non-profit National Veterans Foundation. (9)

A final individual income tax return may be required for the deceased.

You or your tax professional should consult I.R.S. Publication 17 for more detail. Also, search for “Topic 356 – Decedents” on the I.R.S. website. Deductible expenses paid by the deceased before death can generally be claimed as deductions on such a return. (10)

If you have been widowed, consider the future.

In the coming days or weeks, you should arrange a meeting to review your retirement planning strategy, and your will, beneficiary designations, and estate plan may also need to be updated. The passing of your spouse may necessitate a new executor for your own estate. Any durable powers of attorney may also need to be revised.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

On October 13, 2021, the Social Security Administration (SSA) officially announced that Social Security recipients will receive a 5.9 percent cost-of-living adjustment (COLA) for 2022, the largest increase in four decades. This adjustment will begin with benefits payable to more than 64 million Social Security beneficiaries in January 2022. Additionally, increased payments to more than 8 million Supplemental Security Income (SSI) beneficiaries will begin on December 31, 2021. (1)

Biggest COLA Increase in Decades?

While many predicted a bump of as much as 6.1% given recent movement in the Consumer Price Index (CPI), the announced 5.9% increase is still substantial. Some fear that rising consumer prices may dilute the impact of the increase with inflation currently running at more than 5 percent. While this remains to be seen, Social Security beneficiaries will no doubt welcome the largest adjustment in many years.1

How You Will Be Notified

According to the Social Security Administration, Social Security and SSI beneficiaries are usually notified about their new benefit amount by mail starting in early December. However, if you’ve set up your SSA online account, you will also be able to view your COLA notice online through your “My Social Security” account. (1)

Next Steps?

If this increase surprises or concerns you, it’s always a good idea to seek guidance from your financial professional about changes to any of your sources of retirement income. I welcome a chance to talk with you about this.

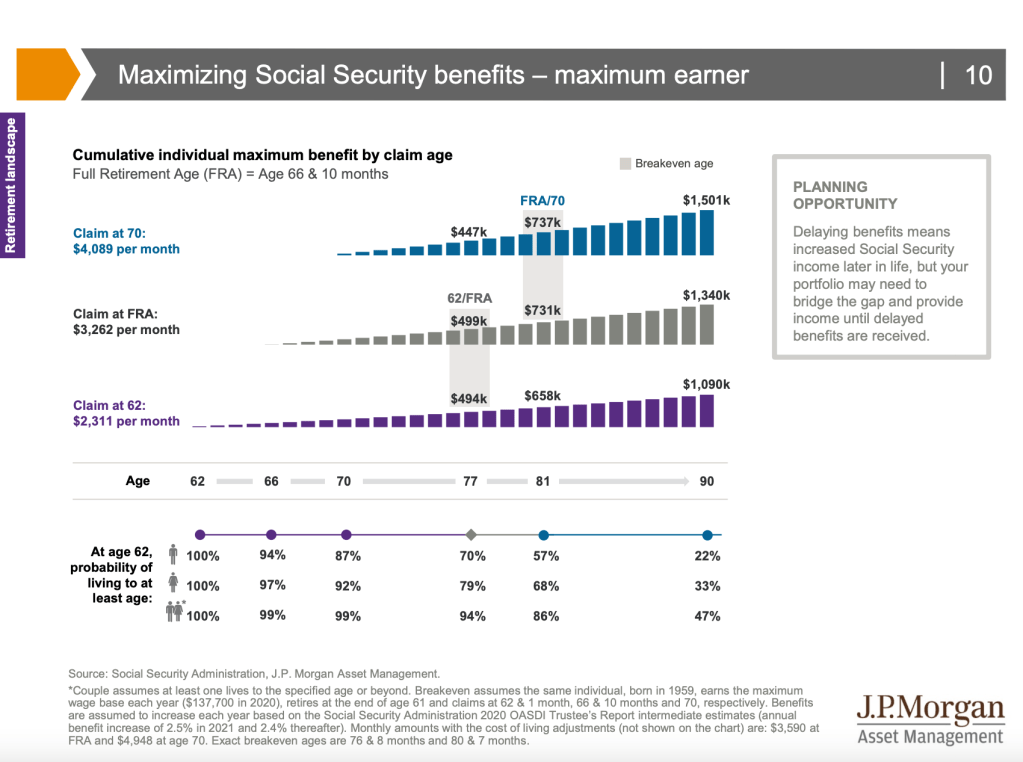

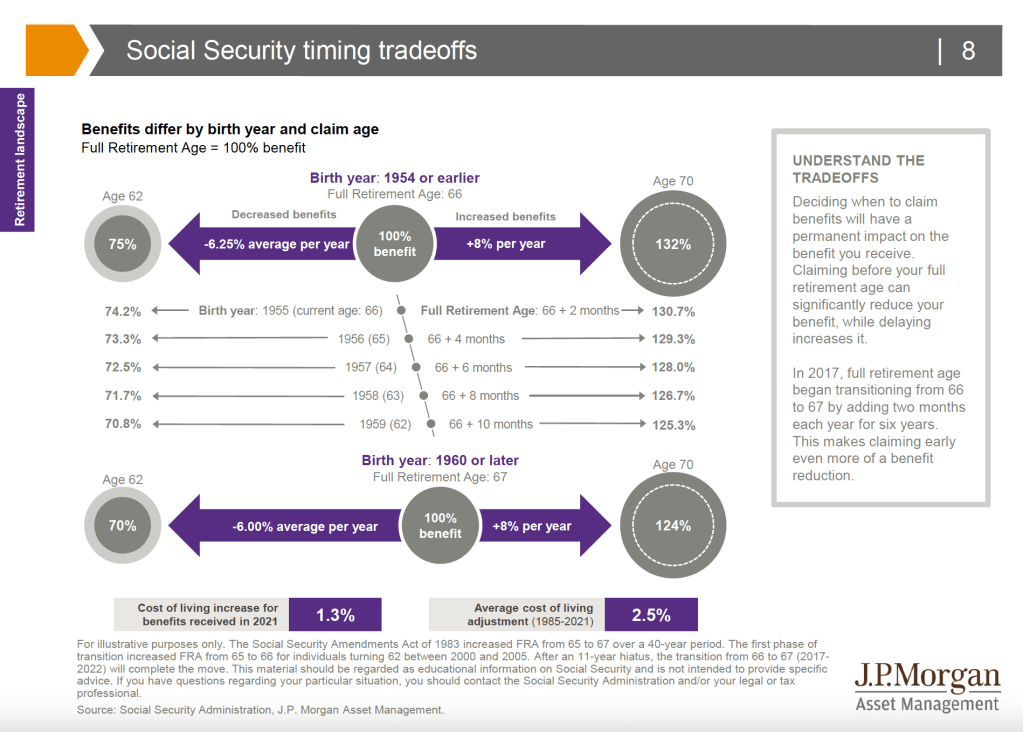

Surprisingly few Americans understand the benefits and trade-offs related to claiming Social Security at various ages. The top graphic illustrates these tradeoffs for people whose Full Retirement Age (FRA) is 66. Delaying benefits results in a much higher benefit amount: Waiting to age 70 results in 32% more in a benefit check than taking benefits at FRA. Likewise, taking benefits early will lower the benefit amount. At age 62, beneficiaries would have received only 75% of what they would get if they waited until age 66. FRA for individuals turning 62 in 2021 is 66 and 10 months, and FRA will continue to move 2 more months in 2022, when it will reach and remain at age 67. The Social Security Amendments Act of 1983 increased FRA from 65 to 67 over a 40-year period. The first phase of transition increased FRA from 65 to 66 for individuals turning 62 between 2000 and 2005. After an 11-year hiatus, the transition from 66 to 67 will complete the move.

The bottom graphic shows the tradeoffs for younger individuals, who will be penalized for early claiming to a greater degree. The percentages shown are “real” amounts – cost-of-living adjustments (COLA) will be added on top, providing an even greater difference between the actual dollar benefits one would receive. The average annual COLA for the past 36 years has been 2.5%.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Most likely, you’ve heard what’s brewing in Washington, D.C., called by one of these names.

The Build Back Better Act.

Or the $3.5 trillion budget reconciliation bill. Or the Jobs and Economic Recovery Plan for Working Families. (1)

Regardless of what name you’ve heard, one fact is clear: It is likely to be months before any action is taken.

When bills are being worked on—especially one that’s this size—it’s a good time to take a quick Civics refresher. Right now, the bill is “in committee” with both the House of Representatives and the Senate. The committees are filling in the policy details and the exact financial figures, which can be a long process. (2)

It will then be up to the House and Senate to vote on an identical version of a final bill—if both can agree to a final version. (2)

Right now, it would be hasty to make any portfolio changes based on what’s being discussed and debated. An ambitious investor would have to guess at what policies will be in the final bill, estimate the financial impact, and determine what portfolio changes should be made. That’s a tall order.

So as difficult as it may be, the best approach is to wait-and-see.

This article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and financial professionals before modifying your tax strategy.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

A power of attorney (POA) is a legal instrument that delegates an individual’s legal authority to another person. If an individual is incapacitated, the POA assigns a trusted party to make decisions on his or her behalf.

There are nondurable, springing, and durable powers of attorney. A nondurable power of attorney often comes into play in real estate transactions, or when someone elects to delegate their financial affairs to an assignee during an extended absence. A springing power of attorney “springs” into effect when a specific event occurs (usually an illness or disability affecting an individual). A “durable” power of attorney allows an assignee, or agent, to act on behalf of a second party, or principal, even after the principal is not mentally competent or physically able to make decisions. Once a principal signs, or executes, a durable power of attorney, it may be used immediately, until it is either revoked by the principal or the principal dies. (1)

Keep in mind this article is for informational purposes only. It’s not a replacement for real-life advice. Make sure to consult your legal professional so you can better understand what type of powers of attorney is a best fit for your situation.

What the POA allows in financial terms. Financially, a Power of Attorney is a tremendously useful instrument. An agent can pay bills, write checks, make investment decisions, buy or sell real estate or other hard assets, sign contracts, file taxes, and even arrange the distribution of retirement benefits.

Advanced Healthcare Directives and Living Wills

Some illnesses can eventually rob people of the ability to articulate their wishes, and this is a major reason why people opt for a Health Care Power of Attorney (HCPOA) or a living will. There are differences between the two.

A Health Care Power of Attorney (also called a “healthcare proxy”) allows an agent to make medical decisions for a principal, should they become physically or mentally incapacitated. A living will gives an assignee similar powers of decision, but this advanced directive only applies when someone faces certain death. The assignee has the authority to carry out the wishes of the incapacitated party.

Would you like to learn more?

It may be time to meet with an attorney who specializes in these issues. You can find one with the help of an insurance or financial professional who has assisted families with legacy planning.

This checklist will help you determine what issues to consider when reviewing your estate plan.

Sources

AgingCare.com, August 23, 2021

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The news keeps getting better for Social Security recipients.

It’s now projected that benefits will increase 6.1% in 2022, up from the 4.7% forecast just two months ago. That would be the most significant increase since 1983. (1,2)

It’s all about inflation. Social Security cost of living adjustments (COLA) are based on the consumer price index, which rose 5.4% in June — its largest 12-month increase since 2008. The official announcement is expected in October and, once it’s confirmed, the revised payment will go into effect in January 2022. (3)

More than 65 million Americans receive Social Security, and the annual cost of living adjustments are designed to help recipients manage higher costs. At the start of 2021, recipients saw a 1.3% increase. (4)

The average monthly benefit is $1,544 for retired workers. So a 6.1% increase amounts to $94 more a month. That might not be quite enough for a car payment, but it’s double the 3% raise being given to U.S. workers in 2021. (4,5)

Social Security can be confusing. One survey found only 6% of Americans know all the factors that determine the maximum benefits someone can receive. If you have any questions, please reach out. We have a number of resources at our fingertips that you may find helpful. (6)

This decision tree is designed to help individuals think through some of the factors related to when to take Social Security benefits. Working, having other sources of income, expected longevity, preserving a portfolio and trying to maximize benefits are important considerations. The possibility of benefits for family is not included; individuals should contact the Social Security Administration if they have questions about their personal situation.

The forecasts for Social Security benefits are based on assumptions, subject to revision without notice, and may not materialize.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

This guide walks through a simple framework to help you think clearly about retirement—from defining what matters most to understanding how your financial pieces fit together.

If you’re looking for help with retirement planning or investment management, you can learn more about how I work with clients at Weiss Financial Group.

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.

Scott Weiss, CFP®

RICP®, CRPC®, AAMS®, AWMA®, APMA®, CMFC®

ADDRESS:

704 Route 6

Mahopac, NY 10541

PHONE:

845-621-4700

Want more insights like this?

Get thoughtful, planning-focused insights delivered occasionally.

No noise. Just practical, planning-focused perspective. Unsubscribe anytime.