Preparing for retirement just got a little more financial wiggle room. The Internal Revenue Service (IRS) announced new contribution limits for 2022.

401(k) & 403(b)

For workplace retirement accounts (i.e. 401(k), 403(b), amongst others), the contribution limit rises $1,000 to $20,500. Catch-up contributions remain at $6,500. (1)

Traditional IRA

Staying put for 2022 are traditional Individual Retirement Accounts (IRAs), with the limit remaining at $6,000. The catch-up contribution for traditional IRAs remains $1,000 as well. (1)

Roth IRA

Eligibility for Roth IRA contributions has increased, as well. These have bumped up to $129,000 to $144,000 for single filers and heads of households, and $204,000 to $214,000 for those filing jointly as married couples. (1)

SIMPLE IRA

Another increase was for SIMPLE IRA Plans (SIMPLE is an acronym for Savings Incentive Match Plan for Employees), which increases from $13,500 to $14,000. (1)

If these increases apply to your retirement strategy, a financial professional may be able to help make some adjustments to your contributions.

Contribution Limits (3,4)

2022

2021

Change

401(k) & 403(b) maximum employee elective deferral

$20,500

$19,500

+$1,000

401(k)s 403(b), etc. employee catch-up contribution (if age 50 or older by year-end)*

$6,500

$6,500

None

Traditional IRA & Roth IRA

$6,000

$6,000

None

Traditional IRA & Roth IRA catch-up contributions (if age 50 or older by year-end)*

$1.000

$1,000

None

SIMPLE IRA

$14,000

$13,500

+$500

RMDs Explained

Once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA) or Savings Incentive Match Plan for Employees IRA in most circumstances. Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Once you reach age 72, you must begin taking required minimum distributions from your 401(k), 403(b), or other defined-contribution plans in most circumstances. Withdrawals from your 401(k) or other defined-contribution plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

5-Year Holding Period for Roth IRAs

To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Most people worry about not having enough money for retirement. But did you also know that there is such a thing as having too much money? Too much money may not necessarily be a bad thing, but you do need to worry about required minimum distributions (RMDs). Here’s what you need to know about RMDs.

RMDs Depend on Your Age

The main point of RMDs is to keep money from staying tax-free forever. The government gave a temporary tax break to encourage you to save for retirement, but it still wants that tax money. A required minimum distribution is a required withdrawal from your retirement account. It counts in your taxable income just like any other withdrawal in retirement.

Currently, RMDs start when you hit age 72 (or 70½ if you turned 70½ prior to January 1, 2020) and they are calculated to empty your retirement account within your expected life expectancy. (1) Each year, you need to withdraw a certain percentage of your account with the percentage going up as you age. However, it’s important to realize that you do not have to spend all of this money. You can also reinvest it into a taxable account.

Not Taking the RMD Can Mean Big Penalties

Thinking about skipping RMDs to avoid taxes? Think again. Not only do you still have to pay the taxes on the RMD amount, but you’ll also owe a 50 percent penalty.

For example, if you were supposed to withdraw $10,000 but didn’t, the IRS will charge you an extra $5,000. The penalty repeats every year until you catch up on your RMDs from previous years.

RMDs Can Throw a Wrench in Your Tax Planning

There are many reasons why you might want to reduce your taxable income in retirement. These can include qualifying for things like Medicaid subsidies, avoiding taxes on your Social Security benefits, trying to stay in a lower capital gains tax bracket, or just wanting to pay fewer taxes.

Required minimum distributions can throw a major wrench in your tax planning because not only are they not avoidable, they can suddenly increase if the market surges. If you’re using a tax strategy that requires reducing your income to a certain level, it’s important to build in flexibility for your RMDs.

RMDs Can Be Avoided

There are still ways to reduce or even avoid RMDs altogether. The main idea is to get the money out of your retirement account when you want to not when the IRS wants you to.

One method is to make extra withdrawals at the end of the year. In December, you can estimate your taxes for the year. If you still have room in a lower tax bracket or below the income you need to stay under, you can withdraw additional money. When next year’s RMDs are calculated, it will be on a lower account balance.

You can also convert to a Roth IRA instead of taxing the money out of a tax-advantaged account. Roth IRAs don’t have RMDs because the money has already been taxed. When you make the conversion, you pay ordinary income tax rates on the amount you converted. There are no penalties even if you do the conversion before you turn 59 1/2.

This content is developed from sources believed to be providing accurate information, and provided by Twenty Over Ten. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

On October 13, 2021, the Social Security Administration (SSA) officially announced that Social Security recipients will receive a 5.9 percent cost-of-living adjustment (COLA) for 2022, the largest increase in four decades. This adjustment will begin with benefits payable to more than 64 million Social Security beneficiaries in January 2022. Additionally, increased payments to more than 8 million Supplemental Security Income (SSI) beneficiaries will begin on December 31, 2021. (1)

Biggest COLA Increase in Decades?

While many predicted a bump of as much as 6.1% given recent movement in the Consumer Price Index (CPI), the announced 5.9% increase is still substantial. Some fear that rising consumer prices may dilute the impact of the increase with inflation currently running at more than 5 percent. While this remains to be seen, Social Security beneficiaries will no doubt welcome the largest adjustment in many years.1

How You Will Be Notified

According to the Social Security Administration, Social Security and SSI beneficiaries are usually notified about their new benefit amount by mail starting in early December. However, if you’ve set up your SSA online account, you will also be able to view your COLA notice online through your “My Social Security” account. (1)

Next Steps?

If this increase surprises or concerns you, it’s always a good idea to seek guidance from your financial professional about changes to any of your sources of retirement income. I welcome a chance to talk with you about this.

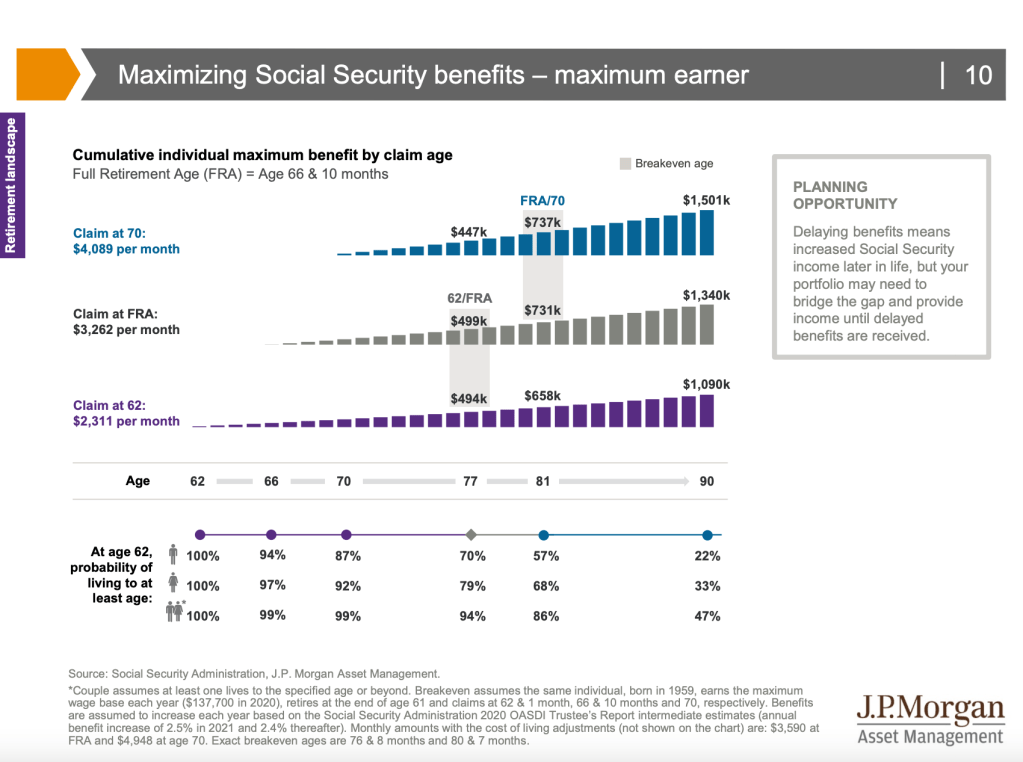

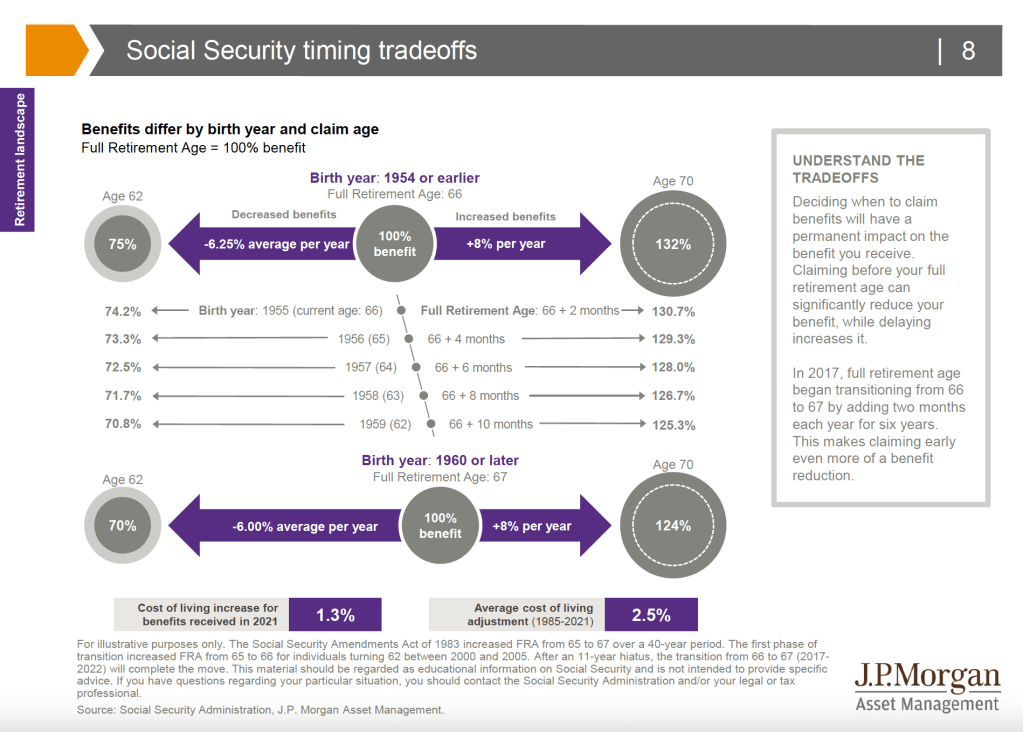

Surprisingly few Americans understand the benefits and trade-offs related to claiming Social Security at various ages. The top graphic illustrates these tradeoffs for people whose Full Retirement Age (FRA) is 66. Delaying benefits results in a much higher benefit amount: Waiting to age 70 results in 32% more in a benefit check than taking benefits at FRA. Likewise, taking benefits early will lower the benefit amount. At age 62, beneficiaries would have received only 75% of what they would get if they waited until age 66. FRA for individuals turning 62 in 2021 is 66 and 10 months, and FRA will continue to move 2 more months in 2022, when it will reach and remain at age 67. The Social Security Amendments Act of 1983 increased FRA from 65 to 67 over a 40-year period. The first phase of transition increased FRA from 65 to 66 for individuals turning 62 between 2000 and 2005. After an 11-year hiatus, the transition from 66 to 67 will complete the move.

The bottom graphic shows the tradeoffs for younger individuals, who will be penalized for early claiming to a greater degree. The percentages shown are “real” amounts – cost-of-living adjustments (COLA) will be added on top, providing an even greater difference between the actual dollar benefits one would receive. The average annual COLA for the past 36 years has been 2.5%.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

The news keeps getting better for Social Security recipients.

It’s now projected that benefits will increase 6.1% in 2022, up from the 4.7% forecast just two months ago. That would be the most significant increase since 1983. (1,2)

It’s all about inflation. Social Security cost of living adjustments (COLA) are based on the consumer price index, which rose 5.4% in June — its largest 12-month increase since 2008. The official announcement is expected in October and, once it’s confirmed, the revised payment will go into effect in January 2022. (3)

More than 65 million Americans receive Social Security, and the annual cost of living adjustments are designed to help recipients manage higher costs. At the start of 2021, recipients saw a 1.3% increase. (4)

The average monthly benefit is $1,544 for retired workers. So a 6.1% increase amounts to $94 more a month. That might not be quite enough for a car payment, but it’s double the 3% raise being given to U.S. workers in 2021. (4,5)

Social Security can be confusing. One survey found only 6% of Americans know all the factors that determine the maximum benefits someone can receive. If you have any questions, please reach out. We have a number of resources at our fingertips that you may find helpful. (6)

This decision tree is designed to help individuals think through some of the factors related to when to take Social Security benefits. Working, having other sources of income, expected longevity, preserving a portfolio and trying to maximize benefits are important considerations. The possibility of benefits for family is not included; individuals should contact the Social Security Administration if they have questions about their personal situation.

The forecasts for Social Security benefits are based on assumptions, subject to revision without notice, and may not materialize.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

If you are like many contemplating retirement, your view is likely pragmatic compared to that of your parents. That doesn’t mean you must have a “plain vanilla” tomorrow. Even if your retirement savings are not as great as you would prefer, you still have great potential to design the life you want.

With that in mind, here are some things to think about.

What do you absolutely need to accomplish?

If you could only get four or five things done in retirement, what would they be? Answering this question might lead you to compile a “short list” of life goals, and while they may have nothing to do with money, the financial decisions you make may be integral to achieving them.

What would revitalize you?

Some people retire with no particular goals at all, and others retire burnt out. After weeks or months of respite, ambition inevitably returns. They start to think about what pursuits or adventures they could embark on to make these years special. Others have known for decades what dreams they will follow … and yet, when the time to follow them arrives, those dreams may unfold differently than anticipated and may even be supplanted by new ones.

In retirement, time is really your most valuable asset. With more free time and opportunity for reflection, you might find your old dreams giving way to new ones. You may find yourself called to volunteer as never before or motivated to work again in a new context.

Who should you share your time with?

Here is another profound choice you get to make in retirement. The quick answer to this question for many retirees would be “family.” Today, we have nuclear families, blended families, extended families; some people think of their friends or their employees as family. You may define it as you wish and allocate more or less of your time to your family as you wish (some people do want less family time when they retire).

Regardless of how you define “family” or whether or not you want more “family time” in retirement, you probably don’t want to spend your time around “dream stealers.” They do exist. If you have a grand dream in mind for retirement, you may meet people who try to thwart it and urge you not to pursue it. (Hopefully, they are not in close proximity to you.) Reducing their psychological impact on your retirement may increase your happiness.

How much will you spend?

We can’t control all retirement expenses, but we can control some of them. The thought of downsizing may have crossed your mind. While only about 10% of people older than 60 sell homes and move following retirement, it can potentially lead to more manageable mortgage payments. You could also lose one or more cars (and the insurance that goes with them) and live in a neighborhood with extensive, efficient public transit. Ditching landlines and premium cable TV (or maybe all cable TV) can bring more savings. Garage sales and donations can have financial benefits as well as helping you get rid of clutter, with either cash or a federal tax deduction.1

This article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and accounting professionals before modifying your overall tax strategy.

Could you leave a legacy?

Many of us would like to give our kids or grandkids a good start in life, but given some of the economic realities of today, leaving an inheritance can be trickier than many realize.

Consider a couple with, for example, $285,000 in retirement savings. If that couple follows the 4% rule, the old maxim that you should withdraw about 4% of your retirement savings per year, subsequently adjusted for inflation – then you are talking about $11,400 withdrawn to start. When you combine that $11,400 with Social Security and other potential investment income, that couple isn’t exactly rich. Sustaining and enhancing income becomes the priority, and legacy preparations may have to take a backseat. On the other hand, a recent survey showed that 92% of all respondents believe it is important to leave money and other assets to their children.2

How are you preparing for retirement?

This is the most important question of all. If you feel you need to prepare more for the future or reexamine your existing strategy in light of recent changes in your life, conferring with a financial professional experienced in retirement approaches may be a smart move.

As households transition into retirement, time that had been spent working now is available for other pursuits. Individuals often enter retirement having spent too little time determining how they plan to spend this time – and run the risk of spending valuable time and money pursuing activities that may not prove to be as fulfilling as they had anticipated. For those who continue to work, they work fewer hours per day. Watching more television is a concerning trend. While a slightly higher percentage of people volunteer at older ages, it is important to note that the time spent volunteering remains about the same.

This material was prepared by MarketingLibrary.Net Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Your degree of happiness in your “second act” may depend on some factors that don’t come with an obvious price tag. Here are some non-monetary factors to consider as you plan your retirement.

What Will You Do With Your Time?

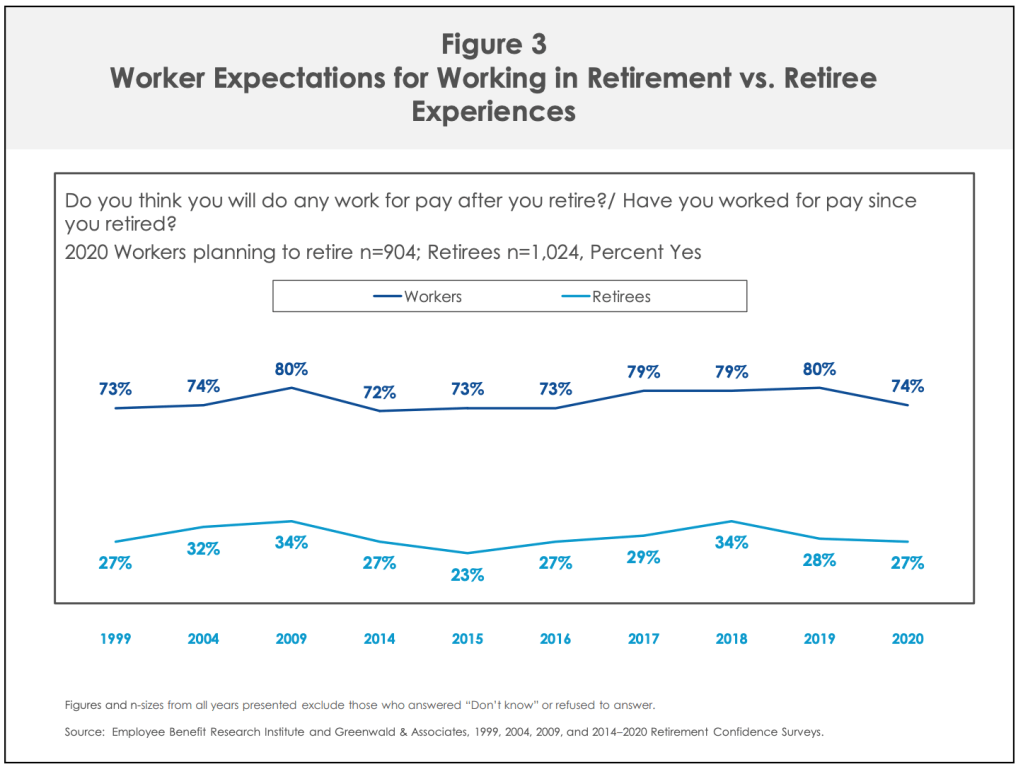

Too many people retire without any idea of what their retirement will look like. They leave work, and they cannot figure out what to do with themselves, so they grow restless. It’s important to identify what you want your retirement to look like and what you see yourself doing. Maybe you love your career, and can’t imagine not working during your retirement. There’s no hard and fast rule to your dream retirement, so it’s important to be honest with yourself. An EBRI retirement confidence survey shows that almost 74% of retirees plan to work for pay, whereas just 27% of retirees report that they’ve actually worked for pay. (1)

While this concept doesn’t have a monetary value, having a clear vision for your retirement may help you align your financial goals. It’s important to remember that your vision for retirement may change—like deciding you don’t want to continue working after all.

Where Will You Live?

This is another factor in retirement happiness. If you can surround yourself with family members and friends whose company you enjoy, in a community where you can maintain old friendships and meet new people with similar interests or life experience, that is a definite plus. If all this can occur in a walkable community with good mass transit and senior services, all the better. Moving away from the life you know to a spread-out, car-dependent suburb where anonymity seems more prevalent than community may not be the best decision for you.

How Are You Preparing to Get Around in Your Eighties and Nineties?

The actuaries at Social Security project that the average life expectancy for men is 84 years old, and the life expectancy for women is 86.5 years. Some will live longer. Say you find yourself in that group. What kind of car would you want to drive at 85 or 90? At what age would you cease driving? Lastly, if you do stop driving, who would you count on to help you go where you want to go and get out in the world? (2)

How Will You Keep Up Your Home?

At 45, you can tackle that bathroom remodel or backyard upgrade yourself. At 75, you will probably outsource projects of that sort, whether or not you stay in your current home. You may want to move out of a single-family home and into a townhome or condo for retirement. Regardless of the size of your retirement residence, you will probably need to fund minor or major repairs, and you may need to find reliable and affordable sources for gardening or landscaping.

These are the non-financial retirement questions that no pre-retiree should dismiss. Think about them as you prepare and invest for the future.

“Nearly 3 in 4 workers (74 percent) plan to work for pay in retirement, compared with just 27 percent of retirees who report they have actually worked for pay in retirement. In fact, the RCS has consistently found that workers are far more likely to plan to work for pay in retirement than retirees are to have actually worked (Figure 3). In the 2019 RCS, among retirees who worked for pay in retirement reported why they worked for pay in retirement and almost all gave a positive reason for doing so, saying they continued to work because they wanted to stay active and involved (91 percent), they enjoyed working (89 percent), or a job opportunity came along (58 percent). a Retirees could have retired for more than one reason. However, they reported that financial reasons also played a role in that decision, such as wanting money to buy extras (75 percent), needing money to make ends meet (37 percent), a decrease in the value of their savings or investments (28 percent), or keeping health insurance or other benefits (16 percent). *Retirees could have worked for pay in retirement for more than one reason.” (1)

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

On October 26, the Treasury Department released the 2021 adjusted figures for retirement account savings. Although these adjustments won’t bring any major changes, there are some minor elements to note.

401(k)s

The salary deferral amount for 401(k)s remains the same at $19,500, while the catch-up amount of $6,500 also remains unchanged. However, the overall limit for these plans will increase from $57,000 to $58,000 in 2021. (1)

Individual Retirement Accounts (IRA)

The limit on annual contributions remains at $6,000 for 2021, and the catch-up contribution limit is also unchanged at $1,000. (2)

Roth IRAs

Roth IRA account holders will experience some slightly beneficial changes. In 2021, the Adjusted Gross Income (AGI) phase-out range will be $198,000 to $208,000 for couples filing jointly. This will be an increase from the 2020 range of $196,000 to $206,000. For those who file as single or as head of household, the income phase-out range has also increased. The new range for 2021 will be $125,000 to $140,000, up from the current range of $124,000 to $139,000. (3)

Although these modest increases won’t impact many, it’s natural to have questions anytime the financial landscape changes. If you’re curious about any of the above, speak to your financial or tax professional for more information.

RETIREMENT PLANS (Annual Contribution Limits)

2021

2020

2019

401(k), 403(b), most 457 plans • 50+ Catch-up Contribution

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

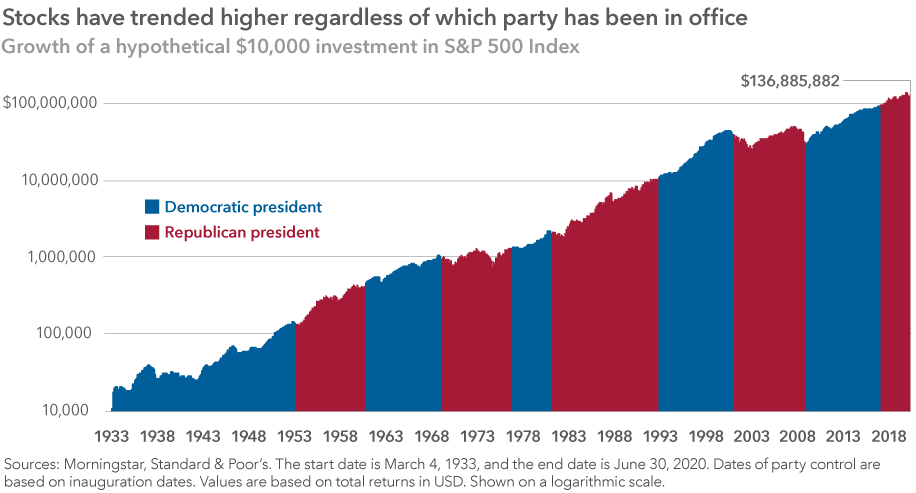

The impact of a potential new President on stock market returns is always a key question in the weeks prior to a general election. It’s important to keep in mind that, despite frequent worries around this time of year, and that financial markets may react in the shorter-term term to poll results and election outcomes (especially surprises), the longer-term effects of any administration’s policies appear to be disconnected from financial market results. Instead, stocks especially tend to follow earnings, which follow economic growth trends. Nevertheless, there are always policy distinctions that could affect various industries to some extent.

In contrast to election season norms in prior decades, polarization between the two parties has become more pronounced, with more extreme positions on both sides forcing candidates away from traditional ‘centrist’ policy often adopted during general election campaigns. A Biden victory has the potential of moving policy toward a more progressive stance, although this is not as simple of a story as in past years, with the current administration having taken a variety of unconventional stances in its own right.

The potential retaking of the Senate by Democrats, in addition to their already holding power in the House, would heighten the risk of more progressive policies being voted in—with minimal opposition. On the other hand, Republicans successfully retaining the Senate would continue to act as an effective counterbalance against legislation from the House, potentially resulting in a policy log jam for the next four years. (Some see this as a best-case scenario, although doing little to alleviate the high current levels of political disagreement.)

The following represent a few areas that could be most impacted by a new Democratic administration, through either new legislation, reversals of prior policies, or no change:

Taxes

It is assumed that the corporate and personal tax cuts put into place in the current regime could be reversed—partially or fully—towards prior levels. Personal income tax policy rhetoric during the campaign has been aimed at the ultra-wealthy, but with high budget deficits and an unprecedented level of fiscal debt, higher tax rates for even middle-income Americans have been feared. This includes higher capital gains tax rates, seen as benefitting the wealthy the most, as they own the majority of financial assets. ‘Wealth taxes’ based on assets are out there as a wildcard as well (although targeted at billionaires). Even if corporate rates do not return to prior max levels of 35%, they are likely not to remain at 21%, either. Most directly, higher tax rates for companies directly erode multi-year earnings projections, which could result in lower stock valuation assessments.

Environment

This multi-faceted policy area includes not only ‘green’ legislation (likely to be promoted by a Biden administration), but also important carryover effects related to the energy industry broadly. It would likely be unfavorable for traditional petroleum- and coal-based energy production (and emissions), including limitations for drilling, and increased regulation of impacts. Conversely, alternative energy sources would likely be promoted—including wind and solar—as well as the potential taxation of carbon emissions.

U.S.-China Relations and Trade

This is a more challenging policy point, as both parties have adopted a hard line on China—for a variety of different reasons. The current administration has taken a more confrontational approach. This has been unique relative to prior regimes, which, at least at the surface, had attempted to avoid outright hostile language and direct economic sanctions. While the two parties agree in principle for a tougher stance, Republicans have focused this effort on corporate intellectual property, while Democrats have also included human rights concerns; specifically, based on the treatment of several ethnic and religious minority groups within the country. This remains a wildcard to some degree, but the majority of Americans and politicians now favor a tougher stance toward China—a rare point of policy agreement.

Antitrust Legislation

This wouldn’t normally surface as a key policy platform, but the rise of several technology behemoths has raised questions over the competitive environment and growing economic power of these firms. In prior decades, pro-business conservative politicians have been more reluctant to attack oligopolistic entities, while populist/progressive movements had been responsible for breaking up dominant ‘Robber Baron’ firms—such as Rockefeller’s Standard Oil in the early 1900’s. In recent years, though, the more progressively-minded tech giants have been supportive of the Democratic agenda and drawing the ire of Republicans—creating a role reversal. The pressure on these firms may continue to some degree, depending on who’s in charge. Some of this oligopolistic power is due to the structures of the industries. They’ve remained among the most fundamentally solid from a financial standpoint during the pandemic, which has rewarded investors. Of course, many small businesses have not fared nearly as well, fanning the flames of resentment.

Workers

Republican policies over the years have generally been focused on letting ‘laissez faire’ (free market) forces determine market competition and pricing dynamics—favored by many mainstream economists. Biden policies would likely offer more worker-friendly populist concessions, such as a higher minimum wage, better health coverage, paid leave, student loan relief, etc. On one hand, additional benefits and pay cut into company profit margins. On the other hand, more money in the pockets of consumers could be a catalyst for broader personal spending and consumption growth broadly, which benefits the broader economy in its own way.

Healthcare

The formation of the Affordable Care Act (‘Obamacare’) was followed by an immediate battle for repeal by Republicans and expansion by Democrats. This fight is likely to continue, with any enhancements in coverage (like ‘Medicare For All’) or other changes aimed at high prescription drug prices (also favored by the current administration, despite potential impact on corporate profits). Some pharmaceutical firms have acted to pre-emptively curb pricing for some drugs in efforts to stem the criticism and potentially unfavorable legislation. These firms counter that such high prices act as the funding mechanism for continued research and development on new therapeutics, which many politicians have accepted. The convoluted health care system, though, continues to overwhelm attempts at reform, which has led to a lower financial market probability for radical change in the near-term.

Defense

In prior years, a strong defense budget and global projection of power has been a Republican party tenet. Lately, this has taken a bit of an opposite turn with conservatives moving more towards a stance of isolation, and progressives seeking to maintain greater globalism. This may be an area with little net change, absent geopolitical surprises (which can be counted on).

Immigration

This doesn’t seem like a market-related topic at first glance, but movement of people across borders affects demographics, which, in turn, affects the size of the labor force and productivity—and ultimately economic growth. This has been a divisive issue throughout America’s history, and each side currently has a mixed relationship with it. Generally, economists argue that a more lenient immigration policy provides a larger pool of workers, which results in not only higher production but also higher consumption. Companies have often silently been in favor of these less restrictive policies, which brings in a higher supply of workers, which lowers wages and boosts profits. On the other side, and often in conflict with other elements of the party, Democratic politicians have tended to have strong support from unionized U.S. workers, which often oppose globalism and foreign worker competition—in efforts to retain jobs and sustain higher wages domestically. Realistically, on net, there could be few extreme changes due to these continual conflicts.

Fiscal Policy

In decades of old, Republicans were seen as the fiscally spendthrift party, while Democrats were cast in debates as ‘tax-and-spend.’ But even prior to the Covid recession, these traditional labels were less applicable, with higher spending proposed on all sides. Due to economic woes from the pandemic likely carrying over into 2021, and perhaps 2022, as well as increasing acceptance of policies such as Modern Monetary Theory (MMT), it appears the accepted spending may continue regardless of the party in office. However, at the fringes, Democrats have proposed more direct relief to workers, and Republicans to small businesses, in keeping with other distinct policy preferences.

Monetary Policy

This should be unaffected by politics, and largely has been over the years. Of course, there have been notable and theatrical exceptions, such as the Fed Chair being physically bullied at LBJ’s Texas ranch in the 1960’s, and the current President’s urging of low rates via social media. A Biden presidency could likely feature more restraint, and a conventional ‘hands off’ approach. However, the Fed could be increasingly impacted by the large Federal deficit and rising debt load, which affects both interest payment obligations as well as credit rating—which affect rates outside of the Fed’s control.

In short, by looking at individual industries, the outlook may not appear to change that much, aside from policy preferences one way or another. The key differences relate to tax policy, the broader regulatory environment, and fiscal spending policies.

It’s important to remember that an elected President has very little effect on market results, historically. In fact, some of the stronger periods of market performance have been under Democratic administrations, contrary to popular assumption. (1)

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

How much does eldercare cost, and how do you arrange it when it is needed? The average person might have difficulty answering those two questions, for the answers are not widely known. For clarification, here are some facts to dispel some myths.

True or False: Medicare will pay for your mom or dad’s nursing home care.

FALSE. Medicare is not extended care insurance. (1)

Medicare Part A will pay the bill for up to 20 days of skilled nursing facility (SNF) care, but after that, you or your parents may have to cover some costs out-of-pocket. After 100 days in a SNF, you will have to cover all costs out of pocket. The only way to “reset the clock” for Medicare coverage of these services is if the patient can somehow go without skilled nursing care for 30 or 60 days or if they require a hospital stay of three full days or longer.

True or False: A semi-private room in a skilled nursing facility costs about $35,000 a year.

FALSE. The median cost of a semi-private room is now $89,297. A private room in an assisted living facility has a median annual cost of $100,375 annually. A home health aide could run you up to $4,385 per month for full-time care. Even if you just need someone to help mom or dad with activities of daily living (ADLs), such as eating, bathing, or getting dressed, the median hourly expense is not cheap: non-medical home aides run about $23 per hour, which at 10 hours a week, means nearly $12,000 a year. (2,3)

True or False: Only around 40% of Americans aged 65 and older are expected to need extended care.

FALSE. Someone turning 65 today has a 70% chance of needing extended care. That means that by 2030, it’s estimated that around 24 million Americans will need extended care. This is double the current number already receiving care. (4,5)

True or False: The earlier you buy extended care insurance, the more manageable the premiums.

TRUE. Younger policyholders may pay lower premiums.

The best time to consider extended care insurance is when you are healthy. While you may be paying a premium for a longer amount of time, the expense may pale in comparison to paying for unexpected medical costs out of pocket. (6)

True or False: Medicaid can pay nursing home costs.

TRUE. The question is, do you really want that to happen? While Medicaid rules vary by state, in most instances, a person may only qualify for Medicaid if they have no more than $2,000 in “countable” assets ($3,000 for a couple). A homeowner can even be disqualified from Medicaid for having too much home equity. A primary residence, a primary motor vehicle, personal property, and household items, burial funds of less than $1,500, and tiny life insurance policies (with face values of less than $1,500) are not countable. So, yes, under these economic circumstances, Medicaid may end up paying extended care expenses. (7)

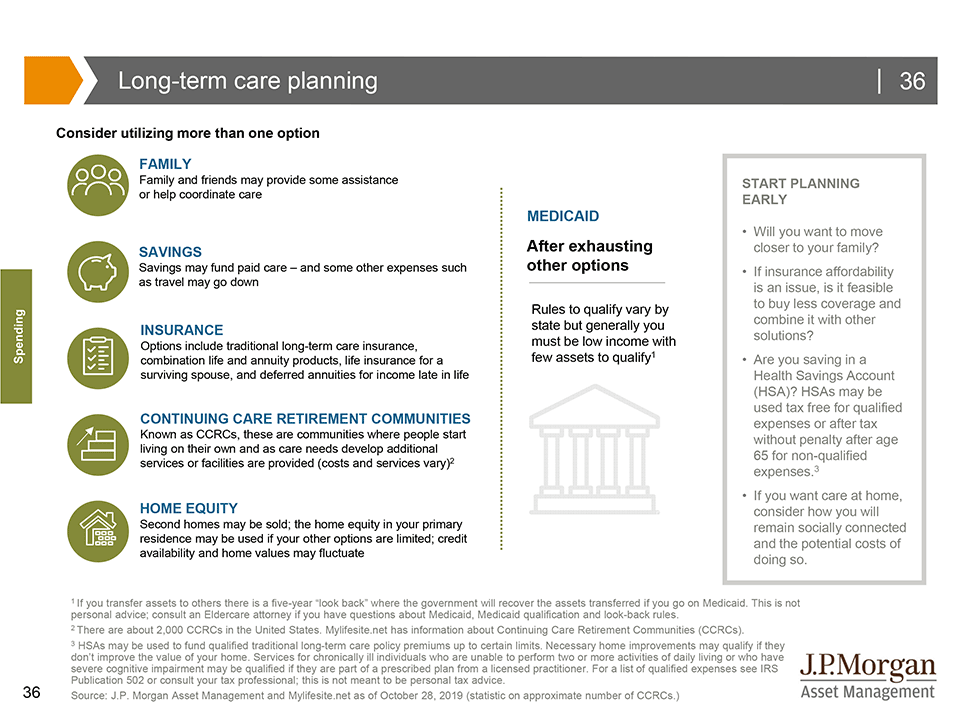

When planning for long-term care, consider multiple solutions that may be utilized including family assistance, income, savings, home equity, life insurance for a surviving spouse, and other insurance options that range from traditional long-term care insurance to combination products to annuities. Continuing Care Retirement Communities (CCRCs) are also a possibility for those who can afford them. Types of CCRCs vary – see MyLifeSite.net for more information. Medicaid may be a last resort; and if Medicaid is utilized, you may have less control of type of care and care setting. For specifics regarding Medicaid qualification in your area, consult with an eldercare attorney.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

In many ways,policies to expect would likely be similar to what’s in place today, and largely opposite of those proposed under a Biden administration.At the same time, Trump’s policies have not followed ‘traditional’ Republican ideologies from decades past in a variety of areas. The Senate Republicans have been far more predictable from a policy standpoint, as have the Congressional Democrats.

The practical factor for the election continues to be whether or not the Democrats are able to take the Senate from the Republicans, which, in addition to holding the House, would allow for the ability to push through a greater volume of progressive legislation. A split-party legislative and/or administrative branch could result in four years of gridlock, with little net change in policy. (That might be perceived as the ‘worst case’ or ‘best case’ depending on the observer.)

Little may change from a higher-level view if the first Trump term morphs into a second. But, it’s important to rememberfrom a financial markets perspective that the President in power has been relatively unimportant in driving longer-term sentiment and returns. Attempting to time election results or moving out of markets to avoid volatility can result in sub-optimal results, even though the weeks prior to an election can become more volatile. Interestingly, in the cases where an incumbent is seeking re-election, one of the few consistent tendencies over the past century is based on U.S. stock market results in the three months prior to Election Day. Based on the S&P 500, a positive return for that stretch has proven favorable for an incumbent’s chances, while a negative return has favored the challenger. (For perspective’s sake, from the window starting Aug. 3, the market is up 0.75% through Fri., Sept. 18—with several more weeks to go until Nov. 3.)

That said, while politics can coincide with day-to-day financial market movements at times, the two rarely correlate meaningfully over the long haul. The chart below bears this out fairly dramatically:

The following policy items assume that a Trump reelection is accompanied by Republicans retaining the Senate, which creates a ‘status quo’ situation. A newly Democratic senate majority would create more of a wildcard:

Taxes

It is probably safe to assume the tax cuts from 2017 would remain in place. These have served to benefit corporations, which receive an immediate boost to the bottom line, resulting in higher reported earnings. Consequently, this models out to higher multi-year growth and justifies higher equity valuations. Personal income tax rates would likely also remain low, along with capital gains rates. Traditional supply-side economists argue that stronger corporate performance and fewer hurdles (such as regulation and taxes) result in a larger ‘pot’ for everyone. However, this assumes that wealth trickles down proportionately to all workers, which has been debated in recent years as income equality between different groups has widened.

Environment

This would also be assumed to be status quo, which includes minimal promotion of green technologies. It would likely be coupled with a pushback on more stringent standards, such as those adopted by California (whose standards predate the EPA and are often stricter). While the energy sector has been struggling with low petroleum prices, due to weaker demand due to the pandemic, current policies would keep additional regulatory headwinds at bay. However, energy firms have been hurt far more by weaker demand from the pandemic than by other factors. U.S.-China relations and trade. The geopolitical tension with China has been steadily growing, and a status quo result would assume more of the same. It’s been claimed by some China experts that the country is currently just playing a ‘waiting game’—for the Trump administration to eventually end, and to instead deal with the successor. As part of their 50- and 100-year national plans, such a delay is seen as just a temporary roadblock. The important component is that a tough U.S. stance on China has support across the aisle—it’s one of the few policy items both parties agree on. So, a longer-term decoupling is likely, although the public stances and negotiation styles could differ between administrations.

Antitrust Legislation

In years past, some Democratic platforms have been seen as anti-corporate (and conversely, pro-worker). This would have translated to a crackdown on large ‘oligopolies’ and a reining in of corporate power in the economy and society. In the current case, argued by some due to the more progressive political leanings of large tech companies, Democrats have appeared less interested in breaking up these firms. Republicans have certainly appeared more interested. Since it’s not quite clear where any ‘abuses’ lie and how consumers are adversely affected (many argue they’ve benefited greatly through both product variety and cost), this issue remains complex and path unclear.

Workers

In line with trends seen globally, not just in the U.S., both parties have taken on a more populist tone in recent years, largely in keeping with the larger societal income gaps. The polarization has taken place far more on the political side than the socioeconomic side, as all parties want to be seen as ‘pro-working class.’ This creates a conundrum, although no clear evolution in policy. Continued trade restrictions may help U.S. firms in the near term, although it’s not clear that benefits trickle down to workers longer-term and could hurt consumers through higher prices. Contrary to the Biden agenda, a second Trump administration would make more progressive items, such as a higher minimum wage and other benefits less likely—although these also depend on the Congressional makeup.

Healthcare

A Trump administration would likely continue to fight ‘Obamacare,’ and continue support for the current private insurance-based healthcare model. Despite the battles over universal coverage/single-payer format, there remains no constructed alternative to the current system for legislators to gravitate to. However, there is bi-partisan populist support for better regulation of high pharmaceutical prices and plugging some gaps to help reduce medical care costs for seniors. The industry has fought back on pharma prices, arguing that profits feed back into research and development for important new therapies, so this has largely resulted in a stalemate in recent years.

Defense

A traditional Republican policy platform has been a strong defense base. This is thought likely to persist, although the Trump administration has focused on far less global interventionism. This hasn’t manifested completely, but could continue to play a role in broader policy thinking. At the same time, China has been viewed as an increasing global military threat, which would necessitate further spending. The trend has been moving from conventional military spending towards new technologies, such as cyberwarfare, satellites, drones, etc.—all of which are technologically complex and expensive.

Immigration

The border ‘wall’ has largely been symbolic, as the Trump administration has clamped down on immigration mostly through policy, which would seem likely to continue in a second term. This has provided a seeming veil of protection for U.S. workers (championed by both candidates in different ways), but economists, who view labor in a global context, see increased restrictions of any kind as a hurdle to stronger economic performance. This is a complex issue, with outcomes the result of multi-decade trends, so the policy action of a single President may only provide a short-term impact on GDP growth. Demographics and business/worker competitiveness play a far more important role, with job training and education enhancements acting as a behind-the-scenes policy championed by many but not discussed as much by candidates in terms of specific plans.

Less stringent regulatory environment.

The President promised to rollback regulations imposed over the past administration, including the expanded use of executive orders, and that has certainly occurred. It’s likely another four years would continue regulation downsizing, in a generally pro-business way, including financial markets and their oversight.

Fiscal policy

The old stereotypes have been cast aside, as parties on both sides are in a spending mode. Republicans are a bit less in favor of direct stimulus to workers (at least in the same large amounts Democrats have been), and more in favor of corporate injections. During the pandemic, airlines and the travel industry have been lobbying especially hard for more aid. This pandemic will end up being expensive regardless of who ends up in the White House, with debt ramifications far beyond the next four years. Monetary policy. As noted earlier, a central bank should be agnostic to political pressures, but that has been easier said than done. Pressure to lower rates or keep policy as ‘easy’ as possible is preferred, since it coincides with keeping the economy growing—which most administrations prefer under their watch. The U.S. Fed has sidestepped such pressure far better than in some countries, of course, but a continuation of the current administration and ‘tweeting’ about central bank decisions runs the risk of negatively influencing public opinion about the Fed and its functions. Politics can also appear in the nomination of certain new board members, such as the controversial Judy Shelton (who has favored revisiting the gold standard—a position rejected by many mainstream economists). Regardless, the Fed has continued to stay out of the political fray over the decades, despite a variety of administrations holding opposing views.

Judicial branch

The Supreme Court is typically not a top concern of financial markets, but with the passing of Justice Ruth Bader Ginsburg, a position on the bench has opened. Any new appointee’s political leanings can tilt the balance of key decisions toward either the conservative or progressive end of the spectrum. So, this can have ramifications for decisions involving business, regulations, or any other economically-relevant area.

Avoid Market Timing Around Politics

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

3 Tips for Successful Investing in an Election Year

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years. (3)

Book a FREE 15 minute, no commitment, phone call with me to discuss your financial situation and see if I can help. Pick a date & time that works for you!

visit weiss-financial.com to learn about our retirement planning & investment services.

Blog Topics:

What I’m Reading

Disclosure

Weiss Financial Group is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities product, service, or investment strategy. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser, tax professional, or attorney before implementing any strategy or recommendation discussed herein. Insurance products and services are offered through individually licensed and appointed agents in all applicable jurisdictions. The advisers at Weiss Financial Group are not attorneys of a law firm but can provide guidance to the client’s other professionals.